STEM Toys Market Size

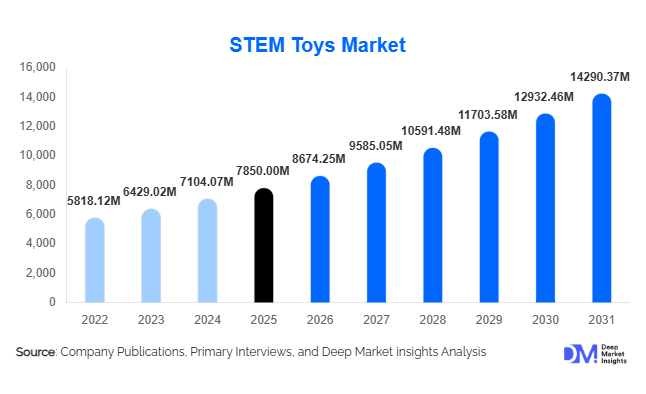

According to Deep Market Insights, the global STEM toys market size was valued at USD 7,850 million in 2025 and is projected to grow from USD 8,674.25 million in 2026 to reach USD 14,290.37 million by 2031, expanding at a CAGR of 10.5% during the forecast period (2026–2031). The STEM toys market growth is primarily driven by rising emphasis on early STEM education, integration of advanced technologies such as AI and AR/VR into educational toys, and increasing parental awareness regarding skill-based cognitive development for children.

Key Market Insights

- Integration of STEM toys with digital learning ecosystems is creating seamless connections between physical and online platforms, enhancing interactive learning and engagement for children.

- Engineering and construction toys dominate the product segment, offering versatile learning experiences in problem-solving, design thinking, and applied sciences, contributing to the largest market share globally.

- North America holds the largest regional share, supported by high disposable income, strong edtech adoption, and curriculum-aligned STEM initiatives in schools.

- Asia-Pacific is the fastest-growing region, with India and China showing surging demand driven by government initiatives and expanding middle-class consumption of educational products.

- The residential segment dominates end-use demand, though educational institutions are emerging as a high-growth segment for bulk procurement of STEM kits and robotics products.

- Technological integration in toys, including AR/VR, AI, and IoT-enabled kits, is reshaping consumer engagement, product differentiation, and long-term adoption trends.

What are the latest trends in the STEM toys market?

Tech-Enhanced Learning and Gamification

STEM toys are increasingly integrating technology, including AI-powered coding platforms, AR-based interactive experiments, and IoT-enabled robotics kits. These innovations allow children to visualize scientific concepts, practice programming skills, and engage in gamified learning, enhancing retention and motivation. Mobile apps now accompany physical kits to provide progress tracking, adaptive learning challenges, and curriculum alignment. Gamification encourages repeated engagement and fosters problem-solving skills in children, making STEM toys more appealing to both educational institutions and parents.

Customization and Curriculum Alignment

Manufacturers are designing STEM kits that align with local curricula, age-appropriate learning objectives, and skill development goals. Customizable kits allow educators and parents to select modules suited for specific learning levels, fostering hands-on learning. This trend is particularly strong in North America and Europe, where standardized learning outcomes are emphasized. Institutions increasingly adopt kits that complement classroom teaching, supporting STEM-focused learning objectives and improving adoption rates.

What are the key drivers in the STEM toys market?

Growing Emphasis on Early STEM Education

Governments and educational organizations worldwide are prioritizing STEM learning from early childhood, recognizing the importance of foundational skills in shaping future workforce capabilities. Initiatives include curriculum integration of coding, robotics, and mathematics-based learning, fueling demand for STEM toys at home and in educational institutions.

Technological Innovation in Toys

The proliferation of AI, robotics, and AR/VR in STEM toys enhances engagement and learning outcomes. Children are drawn to interactive and gamified products that teach programming, engineering, and scientific concepts, which increases market penetration. Companies offering tech-enabled products are seeing higher adoption in both premium and mid-range segments.

Rising Parental Awareness and Spending Power

Parents increasingly recognize the importance of cognitive development and future-ready skills, resulting in higher expenditure on educational toys. This trend is especially prevalent in urban centers and high-income households, where investment in mid-range and premium STEM toys is accelerating market growth.

What are the restraints for the global market?

High Cost of Advanced STEM Toys

Premium STEM toys that integrate robotics, AI, and AR/VR features remain expensive, limiting access in price-sensitive markets. While mid-range and low-cost alternatives exist, affordability challenges restrict penetration in emerging economies, slowing overall growth potential.

Lack of Standardization and Curriculum Alignment

Many STEM toys do not fully align with formal education standards or learning outcomes, particularly in institutional settings. This inconsistency limits adoption in schools and educational programs, creating challenges for manufacturers to demonstrate tangible learning value.

What are the key opportunities in the STEM toys industry?

Digital Learning Integration

The growth of hybrid and digital learning models presents a key opportunity for STEM toy manufacturers to integrate physical kits with online curricula. App-based kits, virtual lessons, and gamified learning experiences allow for continuous engagement and tracking, creating opportunities for subscription-based revenue models and long-term brand loyalty.

Emerging Market Expansion

Emerging regions, especially India, China, and Brazil, are experiencing increased disposable incomes, expanding middle-class populations, and growing awareness of STEM education. Tailoring products to local languages, curricula, and affordability levels can accelerate market penetration, creating high-growth opportunities for both new entrants and established players.

Institutional Partnerships

Educational institutions, including schools, STEM labs, and learning centers, are increasingly adopting STEM kits for bulk procurement. Partnering with government programs or curriculum-aligned initiatives allows manufacturers to secure stable, high-volume demand. Certifications and collaborations with educational boards enhance credibility and facilitate adoption in formal learning environments.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 7850 Million |

| Market Size in 2026 | USD 8674.25 Million |

| Market Size in 2031 | USD 14290.37 Million |

| CAGR | 10.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Engineering and construction toys dominate the product segment, accounting for approximately 28% of the 2025 market. The leadership of this segment is primarily driven by its strong alignment with core STEM learning outcomes such as problem-solving, spatial reasoning, and design thinking. These toys provide hands-on, modular experiences that allow children to experiment, build, and iterate, key factors supporting their widespread adoption across both residential and institutional settings. Additionally, their scalability across age groups and compatibility with curriculum-based learning make them a preferred choice among educators and parents alike.

Robotics and coding kits represent the fastest-evolving segment, gaining traction due to the growing global emphasis on programming literacy and digital skills. Increasing integration of AI, IoT, and app-based interfaces in these kits enhances interactivity and engagement, particularly among middle school and teenage users. Science kits, including chemistry, physics, and biology modules, continue to maintain steady demand by supporting experiential and experiment-driven learning. These kits are widely used in both classrooms and home environments, reinforcing theoretical knowledge through practical application and contributing to their sustained market relevance.

Application Insights

Residential applications remain the largest end-use segment, accounting for approximately 62% of the 2025 market. This dominance is driven by increasing parental awareness regarding early cognitive development and a growing willingness to invest in skill-based educational tools. The rise of home-schooling trends, hybrid learning models, and screen-free educational alternatives further strengthens demand within this segment.

Educational institutions are the fastest-growing segment, supported by the integration of STEM-based curricula in schools and government-backed initiatives promoting experiential learning. Schools, STEM labs, and after-school programs are increasingly adopting robotics kits, coding tools, and science experiment modules to enhance classroom engagement. Additionally, emerging applications such as STEM-based recreational centers, coding bootcamps, maker spaces, and technology-enabled learning zones are diversifying demand. These new-age applications are particularly popular in urban markets, where experiential and project-based learning is gaining prominence.

Distribution Channel Insights

Online retail dominates the distribution landscape, accounting for approximately 55% of the global market share. This leadership is driven by factors such as wider product availability, competitive pricing, convenience of home delivery, and access to detailed product comparisons and reviews. The shift toward direct-to-consumer (D2C) models has further strengthened online channels, enabling manufacturers to build brand loyalty and offer personalized experiences.

E-commerce platforms are increasingly incorporating advanced features such as augmented reality (AR) previews, subscription-based learning kits, and bundled educational packages, enhancing customer engagement. Offline channels, including specialty toy stores, educational supply outlets, and large-format retail stores, continue to play a critical role, particularly in emerging markets. These channels provide hands-on product demonstrations, localized customer support, and immediate product access, which remain key decision-making factors for first-time buyers and institutional purchasers.

Age Group Insights

Middle school children aged 9–12 years represent the largest age segment, capturing approximately 34% of the market in 2025. This segment leads due to increased exposure to structured STEM curricula and the ability of children in this age group to engage with more complex, logic-based, and application-oriented learning tools. Products such as robotics kits, coding platforms, and advanced construction sets are particularly popular within this demographic.

The early childhood segment (0–5 years) is witnessing steady growth, driven by demand for sensory-based and introductory STEM toys that focus on basic cognitive and motor skill development. Meanwhile, teenagers (13–18 years) are increasingly adopting advanced STEM kits, including AI-enabled robotics, programming tools, and engineering models, reflecting a shift toward career-oriented skill development. The growing emphasis on age-specific customization, adaptive learning levels, and curriculum alignment is a key driver supporting adoption across all age groups.

Explore more data points, trends and opportunities Download Free Sample Report

STEM Toys Market Segmentations

By Product Type

- Robotics Kits

- Coding & Programming Toys

- Science Kits

- Engineering & Construction Toys

- Mathematics Learning Toys

- Electronic & Circuit-Based Kits

- AR/VR-Based STEM Toys

By Application

- Residential

- Educational Institutions

- Commercial & Recreational

By Distribution Channel

- Online Retail

- Specialty Educational Stores

- Hypermarkets & Supermarkets

- Brand-Owned Stores

By Age Group

- Early Childhood

- Primary

- Middle School

- Teenagers

Regional Insights

North America

North America accounts for approximately 35% of the global STEM toys market in 2025, with the United States representing nearly 28% of global demand. The region’s dominance is driven by high disposable incomes, advanced educational infrastructure, and strong integration of STEM-focused curricula across schools. Government initiatives promoting digital literacy and coding education at early stages further support demand. Additionally, high penetration of edtech platforms and widespread adoption of technology-enabled toys, including robotics and AI-based kits, are key growth drivers. The presence of leading market players and strong retail and e-commerce ecosystems further accelerates regional expansion.

Europe

Europe holds approximately 22% of the global market share, led by countries such as Germany, the United Kingdom, and France. The region’s growth is supported by strong regulatory emphasis on STEM education, sustainability-focused product development, and high consumer awareness regarding educational toys. Government-backed initiatives promoting science and technology learning in schools, combined with funding for innovation labs and maker spaces, are key drivers. Additionally, increasing demand for eco-friendly and ethically produced toys aligns with Europe’s sustainability goals, further boosting adoption. The region is also witnessing rising demand for gamified and AR-enabled STEM products among younger consumers.

Asia-Pacific

Asia-Pacific accounts for approximately 30% of the global market and is the fastest-growing region, with a projected CAGR exceeding 13% in key countries such as India and China. Growth in this region is driven by expanding middle-class populations, rising disposable incomes, and increasing awareness of STEM education. Government initiatives such as digital education programs, coding in school curricula, and local manufacturing incentives significantly contribute to market expansion. China benefits from its strong manufacturing ecosystem and large domestic demand, while India is witnessing rapid growth due to edtech expansion and increasing private investment in education. Japan and Australia represent mature markets, with steady demand for high-end robotics and advanced learning kits.

Latin America

Latin America is an emerging market, with countries such as Brazil, Mexico, and Argentina driving demand. Growth in this region is supported by urbanization, expansion of the middle-class population, and increasing adoption of digital learning tools. Affordability remains a key factor, with mid-range STEM kits gaining the highest traction. Government efforts to improve educational infrastructure and private sector investments in edtech platforms are also contributing to market growth. Additionally, rising internet penetration and e-commerce adoption are improving product accessibility across the region.

Middle East & Africa

The Middle East & Africa region is witnessing gradual growth, with the UAE and Saudi Arabia leading demand due to high-income households and strong focus on modernizing education systems. Government initiatives aimed at diversifying economies through knowledge-based sectors and investments in smart education infrastructure are key drivers. In Africa, demand is concentrated in urban centers and private educational institutions, where STEM curricula are being increasingly adopted. International aid programs and NGO-led educational initiatives are also supporting market penetration. While the region currently holds a smaller share, improving access to education and digital infrastructure is expected to drive long-term growth.

Key Players in the STEM Toys Market

- LEGO Group

- Mattel Inc.

- Hasbro Inc.

- Spin Master Corp.

- VTech Holdings Ltd.

- Learning Resources Inc.

- Thames & Kosmos

- Melissa & Doug

- Sphero Inc.

- WowWee Group

- Kano Computing

- Makeblock Co., Ltd.

- Elenco Electronics

- SmartLab Toys

- Fischertechnik GmbH