STEM Education Market Size

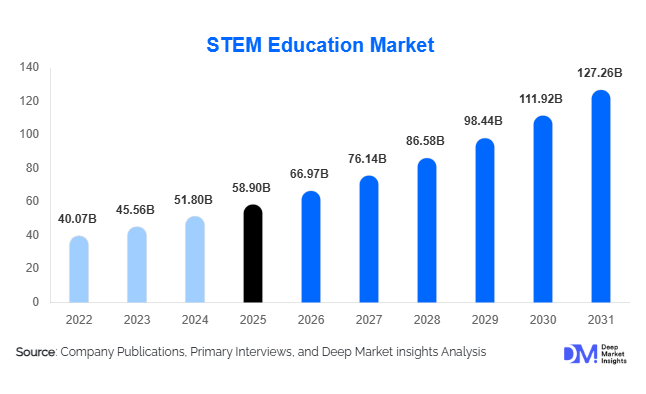

According to Deep Market Insights, the global STEM education market size was valued at USD 58.9 billion in 2025 and is projected to grow from USD 66.97 billion in 2026 to reach USD 127.26 billion by 2031, expanding at a CAGR of 13.7% during the forecast period (2026–2031). The STEM education market growth is primarily driven by accelerating digital transformation across education systems, rising demand for future-ready technical skills, increasing adoption of coding and AI curricula, and growing investments in workforce-oriented science and engineering education globally.

Key Market Insights

- AI-enabled personalized learning platforms are transforming STEM education delivery, enabling adaptive learning pathways, predictive assessments, and intelligent tutoring systems.

- K-12 institutions remain the largest demand segment, supported by government curriculum mandates integrating coding, robotics, engineering, and computational thinking.

- North America dominates the global STEM education market, driven by strong EdTech ecosystems, advanced digital infrastructure, and high institutional spending.

- Asia-Pacific is the fastest-growing regional market, fueled by educational digitization initiatives across China, India, South Korea, Singapore, and Southeast Asia.

- Corporate STEM reskilling programs are rapidly expanding, particularly in AI, cybersecurity, cloud computing, robotics, and data science training.

- Immersive technologies, including AR/VR, gamification, and virtual laboratories, are reshaping engagement models and improving accessibility to practical STEM learning.

STEM Education Market Trends

AI-Powered Personalized Learning Ecosystems Expanding Rapidly

Artificial intelligence is becoming a central component of modern STEM education platforms. Educational institutions and EdTech providers are increasingly deploying AI-powered adaptive learning systems capable of customizing lessons, assessments, and content delivery according to student performance and learning behavior. AI tutoring engines are improving student engagement and retention rates, particularly in mathematics, coding, engineering, and data science disciplines. Intelligent analytics tools are also helping institutions identify learning gaps, automate grading systems, and optimize curriculum pathways. The growing adoption of generative AI is further transforming STEM education by enabling conversational tutoring, automated coding assistance, and real-time problem-solving support. Institutions in the United States, China, South Korea, and Europe are heavily investing in AI-integrated digital learning infrastructure to strengthen educational outcomes and workforce readiness.

Virtual Labs and Gamified STEM Platforms Gaining Momentum

Immersive learning technologies are significantly changing STEM education delivery models worldwide. Virtual laboratories, simulation-based engineering environments, and gamified mathematics applications are improving accessibility to practical STEM training without requiring extensive physical infrastructure investments. AR/VR-enabled science experiments and engineering simulations are helping institutions provide hands-on learning experiences remotely. Gamification strategies including reward systems, competitive coding challenges, interactive robotics exercises, and project-based learning modules are attracting younger learners and improving long-term engagement. Cloud-based collaborative STEM environments are also enabling students from remote regions to access laboratory-grade simulations and participate in global technical learning ecosystems. These trends are particularly accelerating in K-12 education and workforce reskilling programs.

STEM Education Market Drivers

Global Shortage of Skilled STEM Professionals

The rising global shortage of skilled professionals across artificial intelligence, semiconductors, cybersecurity, renewable energy, robotics, aerospace, and advanced manufacturing industries is significantly driving demand for STEM education. Governments and enterprises are investing aggressively in science, technology, engineering, and mathematics programs to build future workforce pipelines capable of supporting industrial modernization and digital economies. Countries including the United States, China, Germany, India, South Korea, and Japan are prioritizing STEM curriculum expansion to address long-term labor shortages in engineering and technology sectors. Employers increasingly value technical competencies including coding, machine learning, data analytics, and automation skills, further accelerating enrollment in STEM-oriented learning programs.

Rapid Digitization of Global Education Systems

The rapid digital transformation of educational ecosystems is another major growth driver for the STEM education market. Cloud-based learning platforms, online coding academies, digital simulation tools, and hybrid classroom models are improving accessibility and scalability of STEM learning globally. Educational institutions are increasingly integrating remote laboratories, AI-enabled assessments, and virtual collaboration tools into mainstream learning systems. Government-funded digital classroom initiatives and low-cost internet expansion are also improving STEM education accessibility in emerging economies. This digitization trend accelerated significantly following the adoption of hybrid learning models, creating sustained demand for cloud-native STEM learning platforms and subscription-based digital education ecosystems.

STEM Education Market Restraints

Infrastructure and Connectivity Gaps in Emerging Economies

Despite strong long-term growth potential, infrastructure inequality remains a major restraint for the STEM education market. Many developing economies continue to face inadequate broadband connectivity, shortages of digital devices, limited laboratory infrastructure, and insufficient teacher training capabilities. Rural schools often struggle to deploy advanced STEM learning systems due to budgetary constraints and poor internet accessibility. These barriers reduce adoption rates for AI-enabled platforms, virtual laboratories, and cloud-based learning environments, particularly across lower-income regions in Africa, Latin America, and parts of Southeast Asia.

High Implementation and Technology Integration Costs

The deployment of advanced STEM education technologies requires substantial capital investment, creating adoption challenges for many institutions. Robotics laboratories, engineering simulation software, AR/VR systems, AI tutoring platforms, and cloud-based learning infrastructures involve high procurement and maintenance costs. Public schools and smaller academic institutions often face budget limitations that delay technology integration. In addition, institutions must invest in teacher retraining programs and curriculum modernization initiatives to effectively implement advanced STEM learning models. The complexity of integrating multiple educational technologies into legacy learning systems also creates operational challenges for schools and universities.

STEM Education Market Opportunities

Corporate Workforce Reskilling and Industry Partnerships

The growing need for workforce transformation across advanced industries presents major opportunities for STEM education providers. Enterprises in manufacturing, automotive, aerospace, healthcare technology, software, and financial services sectors are investing heavily in employee upskilling programs focused on AI, cybersecurity, cloud computing, robotics, and data analytics. Companies are increasingly partnering with universities, coding academies, and EdTech firms to deliver modular technical certification programs aligned with industrial demand. Industry-oriented STEM certifications and job-ready technical training programs are expected to become one of the fastest-growing opportunities within the market. This trend is particularly strong in the United States, Germany, China, India, and the Gulf region.

Expansion of STEM Education Across Emerging Markets

Emerging economies represent one of the largest untapped growth opportunities for the global STEM education market. Governments across India, Indonesia, Vietnam, Saudi Arabia, Brazil, and Africa are significantly increasing investments in digital education modernization and technical workforce development. National industrial transformation programs focused on semiconductor manufacturing, AI, renewable energy, and smart manufacturing are creating substantial demand for STEM talent development. Low-cost cloud learning platforms, multilingual educational applications, mobile-first coding programs, and remote laboratory access systems are enabling providers to scale rapidly across underserved student populations. Public-private partnerships and government-funded digital education initiatives are expected to accelerate market penetration further over the forecast period.

Education Level Insights

K-12 STEM education dominates the global market, accounting for more than 54% of total revenues in 2025 due to extensive government curriculum integration and increasing parental focus on future-ready technical education. Elementary and middle-school STEM learning programs are witnessing rapid adoption as coding, robotics, and computational thinking become standard components of national education systems. High-school STEM education is increasingly emphasizing applied engineering, AI fundamentals, and data science to prepare students for higher education and technical careers. Undergraduate and postgraduate STEM education remain critical demand generators for advanced engineering, biotechnology, and research-oriented learning platforms. Meanwhile, adult STEM reskilling programs are rapidly emerging as enterprises seek continuous workforce upskilling to address technological disruption and industrial automation.

Learning Mode Insights

Self-paced digital learning platforms represent the largest segment within the STEM education market due to affordability, accessibility, and scalability advantages. Online coding academies, mobile learning applications, and cloud-based certification platforms are enabling learners to access STEM education remotely across both developed and emerging economies. Instructor-led learning continues to grow strongly, particularly for advanced engineering, cybersecurity, robotics, and enterprise-oriented technical training programs that require guided mentorship and project-based collaboration. Hybrid learning models combining classroom instruction with digital simulations and remote laboratories are becoming increasingly mainstream across universities and K-12 institutions. Project-based and experiential learning formats are also gaining traction as employers prioritize practical technical competencies over purely theoretical knowledge.

Subject Area Insights

Coding and programming education remains one of the largest revenue-generating segments within the STEM education market due to widespread integration of computer science curricula into primary and secondary education systems globally. Robotics and automation education are experiencing strong growth as schools and universities increasingly deploy robotics kits, maker labs, and engineering simulation environments. Artificial intelligence and machine learning education represent the fastest-growing segment, driven by rising industry demand for AI-skilled professionals. Data science, cybersecurity, and cloud computing programs are also expanding rapidly due to accelerating enterprise digital transformation initiatives. Environmental and sustainability-focused STEM education is emerging as an important niche category aligned with global clean energy and climate technology investments.

Technology Integration Insights

Cloud-based STEM learning platforms dominate technology deployment across the market due to scalability, subscription-based pricing advantages, and centralized content management capabilities. AI-enabled adaptive learning systems are improving personalization and student performance analytics, particularly in mathematics and coding education. AR/VR-integrated STEM platforms are increasingly being used for virtual laboratories, engineering simulations, and immersive science experiments that replicate real-world technical environments. Gamified learning ecosystems continue gaining popularity among younger students by improving engagement through interactive challenges, rewards, and collaborative projects. IoT-enabled STEM laboratories and remote-access engineering systems are also expanding, allowing students to conduct practical experiments using cloud-connected hardware environments.

End-Use Insights

Public schools remain the largest end-use segment within the STEM education market due to government-funded digital education initiatives and nationwide curriculum reforms integrating science, technology, engineering, and mathematics learning. Private schools continue investing aggressively in robotics labs, AI-enabled classrooms, coding academies, and immersive STEM learning environments to strengthen competitive positioning. Universities and technical institutes are driving demand for advanced engineering simulations, cloud laboratories, and research-oriented STEM platforms. Corporate training organizations represent one of the fastest-growing end-use categories as enterprises increasingly invest in workforce reskilling across cybersecurity, cloud computing, AI, and automation disciplines. Direct-to-consumer STEM learning subscriptions are also expanding rapidly as parents increasingly supplement formal education with online coding and mathematics platforms.

| By Education Level | By Learning Mode | By Delivery Platform | By End User | By Deployment Mode |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America accounted for approximately 44% of the global STEM education market in 2025, making it the largest regional market globally. The United States dominates regional demand due to advanced EdTech infrastructure, strong venture capital investment, high institutional spending, and widespread integration of AI, coding, and robotics into educational systems. Public and private schools across the U.S. continue deploying cloud learning platforms, virtual laboratories, and adaptive learning technologies. Canada is also witnessing rising investment in STEM curriculum modernization and digital classroom initiatives, particularly in engineering and AI-focused education programs.

Europe

Europe remains a significant contributor to global STEM education revenues, led by Germany, the United Kingdom, France, and the Nordic countries. Germany continues emphasizing engineering and technical education aligned with industrial automation and advanced manufacturing requirements. The United Kingdom is experiencing rising adoption of coding and AI-focused curricula across both K-12 and higher education institutions. European governments are investing heavily in sustainability-oriented STEM education, particularly in clean energy engineering, climate science, and digital manufacturing technologies. Demand for vocational STEM training and apprenticeship-oriented technical education also remains strong across the region.

Asia-Pacific

Asia-Pacific is the fastest-growing regional STEM education market and is projected to expand at a CAGR exceeding 16% during the forecast period. China and India represent the largest growth engines due to massive student populations, rapid educational digitization, and increasing government investment in technology-oriented learning. China continues investing heavily in AI, semiconductor engineering, robotics, and coding education aligned with industrial modernization strategies. India is emerging as one of the fastest-growing EdTech markets globally due to expanding online learning ecosystems, mobile-first education platforms, and national digital education initiatives. South Korea, Japan, and Singapore also maintain strong demand for advanced robotics, engineering, and AI education programs.

Latin America

Latin America is gradually emerging as a promising market for STEM education, led by Brazil, Mexico, Chile, and Argentina. Governments across the region are increasing investments in digital classrooms, technical education modernization, and online learning accessibility. Brazil represents the largest regional market due to growing EdTech adoption and rising enterprise demand for technical workforce development. Mobile learning applications and cloud-based STEM platforms are gaining popularity across the region as institutions seek cost-effective digital education solutions. However, infrastructure inequality and funding limitations continue to slow broader market penetration.

Middle East & Africa

The Middle East and Africa region is witnessing accelerating demand for STEM education due to national economic diversification and workforce modernization initiatives. Saudi Arabia and the UAE are heavily investing in AI-focused universities, smart classrooms, engineering institutions, and digital learning ecosystems under long-term innovation strategies. Governments are prioritizing technical workforce development aligned with renewable energy, smart city, and industrial automation initiatives. South Africa is also strengthening STEM education investment to support technology-driven economic growth. Across Africa, mobile-first digital learning platforms are improving accessibility to coding and science education in underserved regions.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the STEM Education Market

- Coursera

- Udemy

- Pearson

- BYJU'S

- Chegg

- Instructure

- Blackboard

- Labster

- Arduino

- LEGO Education

- Stride Inc.

- 2U Inc.

- DreamBox Learning

- Robolink

- Khan Academy