Steel Furniture Market Size

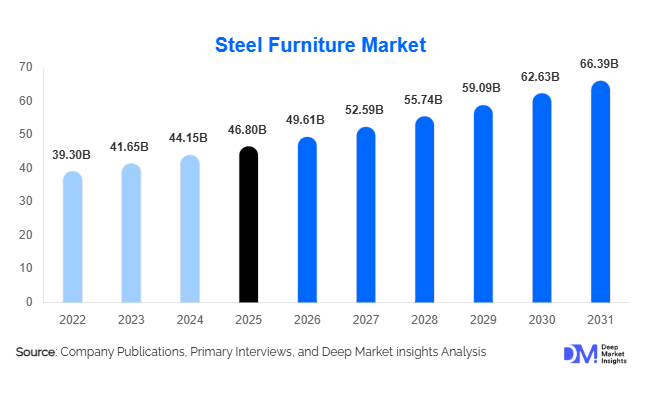

According to Deep Market Insights, the global steel furniture market size was valued at USD 46.8 billion in 2025 and is projected to grow from USD 49.61 billion in 2026 to reach USD 66.39 billion by 2031, expanding at a CAGR of 6.0% during the forecast period (2026–2031). The steel furniture market growth is primarily driven by increasing urbanization, rising investments in commercial and institutional infrastructure, growing preference for durable and low-maintenance furniture, and the rapid adoption of modular and ergonomic steel furniture solutions across residential and commercial applications.

Key Market Insights

- Steel furniture is increasingly replacing traditional wooden furniture across offices, healthcare facilities, educational institutions, and industrial environments due to superior durability, lower maintenance costs, and longer lifecycle performance.

- Modular and multifunctional furniture systems are witnessing strong global demand, particularly in urban residential markets where compact living spaces are driving demand for foldable and space-efficient furniture solutions.

- Asia-Pacific dominates the global steel furniture market, led by China and India due to strong manufacturing ecosystems, rapid urbanization, and growing institutional infrastructure investments.

- North America remains a major premium market, driven by ergonomic office furniture demand, workplace modernization, and increasing adoption of sustainable furniture procurement practices.

- Healthcare and educational infrastructure expansion globally is significantly accelerating demand for stainless steel furniture products, including hospital beds, laboratory furniture, lockers, and storage systems.

- Technological advancements in robotic welding, CNC fabrication, and powder coating are enabling manufacturers to improve customization, production efficiency, and product aesthetics while reducing operational costs.

What are the latest trends in the steel furniture market?

Growing Adoption of Modular and Smart Furniture

The steel furniture industry is witnessing a strong shift toward modular, ergonomic, and multifunctional furniture systems. Urban housing constraints and evolving workplace designs are increasing demand for compact furniture solutions that maximize space utilization without compromising durability. Manufacturers are increasingly offering customizable steel furniture platforms with adjustable configurations, integrated storage systems, and foldable designs tailored for both residential and commercial environments. The rise of hybrid work culture has further accelerated demand for ergonomic steel desks, home-office workstations, and collaborative office furniture systems. Smart furniture integration, including cable management systems, height-adjustable desks, sensor-enabled workstations, and digitally connected office environments, is also emerging as a key differentiator in premium commercial furniture categories.

Sustainability and Recycled Steel Integration

Sustainability has become a major strategic focus within the global steel furniture market. Manufacturers are increasingly adopting recycled steel inputs, low-emission powder coating technologies, and energy-efficient production systems to align with global environmental standards and green procurement requirements. Steel furniture is gaining traction as a sustainable alternative due to its high recyclability and longer replacement cycle compared with plastic and engineered wood furniture. Corporate buyers, educational institutions, and government procurement agencies are prioritizing environmentally certified furniture products to support ESG commitments and green building standards such as LEED certifications. Additionally, manufacturers are investing in lightweight steel alloys and eco-friendly coatings to improve both sustainability performance and product aesthetics.

What are the key drivers in the steel furniture market?

Rapid Urbanization and Commercial Infrastructure Expansion

Rapid urbanization and increasing investments in commercial infrastructure development are among the strongest drivers of the global steel furniture market. Governments and private enterprises worldwide are investing heavily in offices, educational institutions, healthcare facilities, transportation infrastructure, hotels, and co-working spaces, all of which require durable and cost-effective furniture systems. Steel furniture is increasingly preferred due to its strength, longevity, corrosion resistance, and low maintenance costs. Emerging economies such as India, China, Indonesia, Vietnam, and Saudi Arabia are experiencing particularly strong demand growth due to expanding urban populations and rising infrastructure investments. Large-scale smart city projects and institutional modernization programs are also creating substantial procurement opportunities for steel furniture manufacturers.

Increasing Demand for Ergonomic and Flexible Furniture Solutions

Changing workplace dynamics and evolving consumer lifestyles are driving demand for ergonomic and flexible furniture systems. Businesses are redesigning office layouts to improve employee productivity, collaboration, and workplace wellness, leading to higher adoption of modular steel workstations, adjustable desks, ergonomic chairs, and collaborative office furniture systems. In residential applications, consumers increasingly favor compact and multifunctional furniture due to shrinking apartment sizes and urban living constraints. The rise of remote and hybrid work models has significantly boosted demand for steel home-office furniture globally. Manufacturers are integrating modern aesthetics, ergonomic designs, and smart functionalities into steel furniture products to cater to evolving customer preferences.

What are the restraints for the global market?

Volatility in Steel Raw Material Prices

Fluctuations in global steel prices remain a significant challenge for steel furniture manufacturers. Variations in iron ore prices, energy costs, freight expenses, and geopolitical trade disruptions directly impact manufacturing costs and profit margins. Sudden increases in steel prices often create pricing pressure across the value chain, limiting profitability for manufacturers operating in highly competitive and price-sensitive markets. Smaller manufacturers with limited procurement capabilities are particularly vulnerable to raw material price instability. In addition, rising transportation and logistics costs further compound operational challenges, especially for export-oriented furniture manufacturers.

Competition from Alternative Furniture Materials

The steel furniture market faces strong competition from engineered wood, aluminum, plastic composites, and hybrid furniture materials. In residential applications, especially, consumers often prefer the visual warmth and premium aesthetics associated with wooden furniture. While steel furniture offers superior durability and longevity, manufacturers must continuously innovate in coatings, design aesthetics, and hybrid material integration to compete effectively. Low-cost plastic furniture alternatives also remain highly competitive in developing economies due to affordability and lightweight characteristics. Consumer perception regarding metallic furniture aesthetics can also act as a barrier in certain residential markets.

What are the key opportunities in the steel furniture industry?

Expansion of Institutional Infrastructure Projects

Large-scale investments in healthcare, education, transportation, and government infrastructure present major growth opportunities for steel furniture manufacturers. Hospitals, laboratories, schools, universities, airports, and public offices require highly durable, hygienic, and low-maintenance furniture solutions that steel furniture is well-positioned to provide. Stainless steel hospital furniture, laboratory workstations, storage systems, and educational furniture are witnessing particularly strong procurement demand across Asia-Pacific, the Middle East, and Africa. Government modernization programs and public infrastructure expansion initiatives are expected to continue supporting long-term demand growth within institutional segments.

Growth of E-commerce and Direct-to-Consumer Sales

The rapid expansion of digital commerce platforms is transforming the global steel furniture industry. Online furniture retail channels are enabling manufacturers to directly access residential consumers and small businesses while improving profit margins through reduced intermediary dependence. Digital visualization tools, augmented reality product previews, customizable modular platforms, and omnichannel marketing strategies are enhancing online consumer engagement. Younger consumers increasingly prefer online furniture purchases due to convenience, transparent pricing, and product customization capabilities. This trend is particularly strong in North America, India, China, and Southeast Asia, where organized online furniture retail penetration continues to rise rapidly.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 46.8 Billion |

| Market Size in 2026 | USD 49.61 Billion |

| Market Size in 2031 | USD 66.39 Billion |

| CAGR | 6.0% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Office steel furniture represents the largest product category globally, accounting for nearly 28% of the overall steel furniture market in 2025. Rising investments in commercial real estate, corporate workplace modernization, and co-working infrastructure are driving strong demand for steel workstations, filing cabinets, ergonomic chairs, and modular office systems. Residential steel furniture is also witnessing significant growth due to increasing urban housing demand and rising preference for compact, durable, and affordable furniture solutions. Institutional steel furniture remains another key segment, supported by procurement from schools, hospitals, laboratories, and government offices. Industrial and warehouse furniture categories, including lockers, heavy-duty storage racks, and workbenches, are experiencing rapid growth due to expanding logistics and manufacturing sectors globally. Hospitality-focused steel furniture demand is also increasing with rising investments in hotels, restaurants, resorts, and outdoor leisure infrastructure.

Material Type Insights

Stainless steel furniture accounted for approximately 34% of the global market in 2025, making it the leading material segment due to superior corrosion resistance, hygiene performance, and durability. Stainless steel products are widely utilized across healthcare, hospitality, laboratory, and food-service environments where sanitation standards are critical. Mild steel furniture continues to dominate cost-sensitive residential and commercial applications because of affordability and structural strength. Powder-coated steel furniture is witnessing rapid growth as manufacturers focus on improved aesthetics, scratch resistance, and color customization. Hybrid steel-wood furniture designs are also gaining traction among urban consumers seeking modern industrial aesthetics combined with premium visual appeal. Recycled steel integration is increasingly becoming important as sustainability-focused procurement practices expand globally.

Distribution Channel Insights

Direct B2B sales remain the dominant distribution channel within the steel furniture market, contributing nearly 39% of global revenues in 2025. Institutional procurement contracts from offices, schools, hospitals, hotels, and government agencies continue to generate stable long-term demand for manufacturers. Furniture specialty stores also maintain significant market presence by offering product customization and showroom-based purchasing experiences. However, online retail channels are emerging as the fastest-growing distribution segment globally due to increasing digital commerce penetration and changing consumer buying behavior. Manufacturers are increasingly investing in direct-to-consumer platforms, digital product configurators, and omnichannel sales strategies to improve market reach and customer engagement. Interior designers and project-based procurement channels are also gaining importance within premium commercial and hospitality furniture segments.

Application Insights

Indoor steel furniture applications account for nearly 71% of the global steel furniture market due to widespread usage across residential, commercial, healthcare, and educational environments. Office interiors remain the largest demand-generating application area globally. Outdoor steel furniture is witnessing strong growth due to increasing investments in hospitality infrastructure, urban landscaping, public parks, and residential outdoor living spaces. Hygienic and sterile applications, particularly within healthcare and laboratory environments, are driving demand for stainless steel furniture systems. Industrial applications such as warehouse storage, factory workstations, and maintenance furniture are also expanding rapidly due to rising industrial automation and logistics infrastructure development. Compact urban living applications continue to support innovation in foldable and multifunctional steel furniture designs.

End-Use Industry Insights

Corporate offices represent the leading end-use industry within the global steel furniture market, accounting for approximately 24% of overall market demand in 2025. Rising investments in smart office infrastructure, collaborative workspaces, and ergonomic workplace modernization are driving strong procurement activity globally. Residential demand continues to expand steadily alongside urban housing development and increasing consumer preference for durable furniture solutions. Healthcare infrastructure represents one of the fastest-growing end-use industries due to rising investments in hospitals, clinics, and laboratories globally. Educational institutions remain important consumers of steel desks, benches, lockers, and storage systems through ongoing school modernization programs. Manufacturing, warehousing, hospitality, and transportation infrastructure sectors are also emerging as major demand contributors due to industrial expansion and public infrastructure development worldwide.

Explore more data points, trends and opportunities Download Free Sample Report

Steel Furniture Market Segmentations

By Product Type

- Residential Steel Furniture

- Commercial Steel Furniture

- Institutional Steel Furniture

- Industrial & Warehouse Furniture

- Hospitality & Leisure Furniture

By Material Type

- Mild Steel Furniture

- Stainless Steel Furniture

- Galvanized Steel Furniture

- Powder-coated Steel Furniture

- Hybrid Steel Furniture

By Design Category

- Traditional Steel Furniture

- Contemporary Steel Furniture

- Modular Furniture

- Foldable & Space-saving Furniture

- Ergonomic Steel Furniture

- Smart Steel Furniture

By Distribution Channel

- Direct/B2B Sales

- Furniture Specialty Stores

- Hypermarkets & Supermarkets

- Online Retail/E-commerce

- Institutional Procurement Contracts

- Interior Designers & Project Sales

By Application

- Indoor Furniture

- Outdoor Furniture

- Industrial Applications

- Healthcare & Hygienic Applications

- Compact Urban Living Applications

By End-use Industry

- Residential

- Corporate Offices

- Education

- Healthcare

- Hospitality

- Manufacturing & Warehousing

- Government & Defense

- Retail & Commercial Spaces

Regional Insights

North America

North America accounted for approximately 21% of the global steel furniture market in 2025, led primarily by the United States. Demand within the region is driven by office modernization, healthcare infrastructure investments, and increasing preference for ergonomic and sustainable furniture systems. Corporate workplace redesign initiatives and hybrid work trends continue to accelerate the adoption of modular office furniture solutions. Canada also contributes a stable demand from the healthcare and educational infrastructure sectors. Growing emphasis on environmentally sustainable procurement practices is further supporting demand for recyclable steel furniture products across the region.

Europe

Europe represented nearly 19% of the global steel furniture market in 2025. Germany remains the leading regional market due to strong commercial infrastructure investments, advanced manufacturing capabilities, and high adoption of modular office furniture systems. France, the United Kingdom, and Italy continue to generate significant demand from hospitality, healthcare, and residential renovation sectors. Sustainability regulations and green building standards are strongly influencing furniture procurement trends across Europe, encouraging adoption of recyclable steel-based products. The region also demonstrates growing demand for premium ergonomic office furniture integrated with smart workplace technologies.

Asia-Pacific

Asia-Pacific dominates the global steel furniture market with approximately 48% market share in 2025. China remains the world’s largest steel furniture producer and exporter due to extensive manufacturing ecosystems, integrated steel supply chains, and competitive production costs. India is emerging as one of the fastest-growing markets globally, supported by urbanization, smart city projects, educational infrastructure expansion, and rising middle-class housing demand. Japan and South Korea continue to generate stable demand for premium minimalist and ergonomic steel furniture. Southeast Asian countries including Vietnam, Indonesia, and Thailand, are also witnessing strong industrial and commercial furniture demand due to manufacturing expansion and export-oriented production growth.

Latin America

Latin America represents a steadily growing market led by Brazil and Mexico. Rising commercial infrastructure investments, industrialization, and hospitality sector expansion are supporting demand for steel furniture across the region. Brazil continues to dominate regional demand due to growth in corporate offices, educational institutions, and public infrastructure projects. Mexico is benefiting from increasing manufacturing investments and logistics infrastructure development linked to nearshoring trends. Demand for affordable modular residential furniture is also increasing across major urban centers within the region.

Middle East & Africa

The Middle East & Africa region is emerging as one of the fastest-growing steel furniture markets globally, supported by large-scale infrastructure investments and hospitality expansion projects. Saudi Arabia and the UAE are investing heavily in airports, hotels, healthcare facilities, and smart city developments, creating strong demand for institutional and commercial furniture systems. South Africa remains a key regional market due to industrial infrastructure and educational procurement demand. Across Africa, increasing urbanization and public infrastructure development are expected to support long-term growth in educational and healthcare furniture segments.

Key Players in the Steel Furniture Market

- Steelcase

- Herman Miller

- HNI Corporation

- IKEA

- Godrej Interio

- Haworth

- Kokuyo

- Okamura Corporation

- Kimball International

- Global Furniture Group

- Virco

- Nilkamal

- Inter IKEA Systems

- USM

- Spacesaver Corporation