Steam Cleaner Market Size

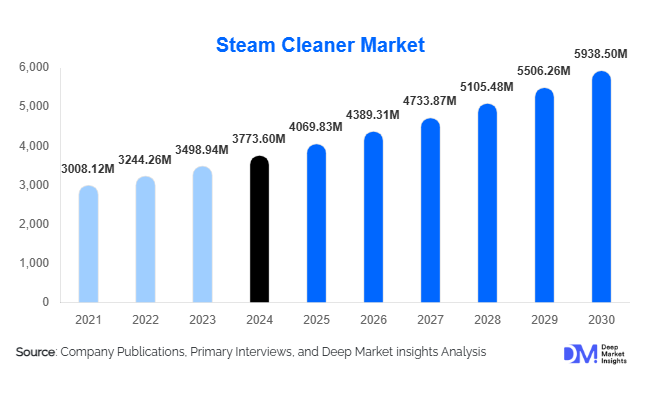

According to Deep Market Insights, the global steam cleaner market size was valued at USD 3,773.60 million in 2025 and is projected to grow from USD 4,069.83 million in 2026 to reach USD 5,938.50 million by 2031, expanding at a CAGR of 7.85% during the forecast period (2026–2031). Growth in the steam cleaner market is primarily driven by rising consumer preference for chemical-free cleaning solutions, expansion of commercial hygiene requirements, and rapid technological innovation in portable, cordless, and industrial-grade steam cleaning systems.

Key Market Insights

- Rising demand for eco-friendly and chemical-free cleaning is significantly boosting adoption across residential, commercial, and industrial applications.

- Handheld and portable steam cleaners dominate household usage, driven by compact living spaces and increasing dual-income households.

- Industrial and institutional buyers are rapidly increasing procurement due to stringent hygiene and safety regulations in the food, healthcare, and manufacturing sectors.

- Asia-Pacific leads global demand growth, with expanding middle-class populations in China and India accelerating appliance adoption.

- Online retail channels are becoming major sales drivers, as consumers prefer digital comparison, reviews, and discount-driven purchasing.

- Technological integration, including cordless systems, smart sensors, and automated steam control, is elevating product performance and customer satisfaction.

Steam Cleaner Market Trends

Eco-conscious & Chemical-free Cleaning Driving Adoption

Consumers are increasingly prioritizing non-toxic, chemical-free cleaning methods due to rising awareness about indoor air quality, allergens, and environmental sustainability. Steam cleaners meet these needs by providing deep sanitization using only heated water vapor. Manufacturers are responding with models optimized for low water usage, high-efficiency steam production, and multi-surface capabilities. The trend is particularly pronounced in households with children, pets, or elderly occupants, where health-oriented cleaning is prioritized.

Technological Advancements in Smart & Portable Steam Cleaning

Technological innovation is reshaping the steam cleaner landscape. Cordless and battery-powered models are gaining traction due to improved run-time and flexible maneuvering. Smart steam cleaners with microprocessor-controlled steam output, auto-descaling, IoT connectivity, and app-based controls are entering the premium segment. Commercial units now integrate real-time temperature monitoring and high-pressure delivery systems for industrial sanitation tasks. These innovations appeal to both residential and B2B buyers seeking efficiency, convenience, and durability.

Steam Cleaner Market Drivers

Growing Preference for Eco-friendly Cleaning Solutions

Growing health awareness and the desire to minimize exposure to harsh chemicals have pushed consumers toward steam-based cleaning. Steam cleaners eliminate bacteria, viruses, and allergens effectively without chemical residues, an especially compelling value proposition in post-pandemic households and businesses.

Urbanization & Rise of Dual-income Households

Increasing urbanization, smaller living spaces, and time-constrained lifestyles have accelerated the demand for compact, fast-cleaning devices. Dual-income families favor handheld and portable steam cleaners due to their ability to perform deep cleaning in less time, contributing significantly to residential market growth.

Commercial & Industrial Hygiene Regulations

Healthcare, food processing, hospitality, and automotive industries face stricter sanitation standards. Steam cleaners provide high-temperature sterilization suitable for industrial surfaces, equipment, and machinery. This regulatory-driven adoption boosts demand for high-pressure and industrial-grade steam cleaners.

Steam Cleaner Market Restraints

High Initial Cost of Premium & Industrial Steam Cleaners

Industrial-grade models require significant capital investment, making them inaccessible for small businesses or low-income households. This cost barrier slows penetration in emerging economies and price-sensitive segments, especially when cheaper traditional cleaning alternatives are available.

Competition from Traditional Cleaning Methods

Despite their benefits, steam cleaners face strong competition from conventional mop-and-bucket cleaning methods, chemical-based solutions, and low-cost vacuum cleaners. Consumer inertia and limited awareness in emerging markets further restrict adoption rates.

Steam Cleaner Market Opportunities

Strong Demand in Emerging Markets with Rising Middle Class

Urban growth in Asia-Pacific, Latin America, and the Middle East is creating a large new consumer base for home-cleaning appliances. Affordable handheld and mid-priced steam cleaners tailored to these regions present substantial market-entry and expansion opportunities for both global and regional players.

IoT-enabled Steam Cleaners & Smart Home Integration

The growing “smart home” ecosystem opens room for IoT-based steam cleaners that can automate cleaning cycles, monitor hygiene levels, and optimize energy consumption. This technology-driven differentiation can attract premium buyers and help manufacturers establish brand leadership.

Industrial Expansion Driven by Regulatory Compliance

Stricter hygiene guidelines in healthcare, pharmaceuticals, food & beverage production, and automotive maintenance have created sustained demand for industrial-grade steam cleaning systems. Vendors who introduce high-pressure, customizable, and energy-efficient solutions can capitalize on a rapidly expanding B2B segment.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3773.60 Million |

| Market Size in 2026 | USD 4069.83 Million |

| Market Size in 2031 | USD 5938.50 Million |

| CAGR | 7.85% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Residential handheld steam cleaners dominate the market, accounting for approximately 25–30% of 2025 revenue. Their success is attributed to versatility, affordability, and suitability for quick cleaning tasks in small urban homes. Steam mops and hybrid steam vacuum cleaners are also expanding rapidly as consumers seek multi-function appliances.

In the commercial and industrial category, high-pressure steam systems are witnessing heightened adoption, especially in manufacturing, food processing, and automotive workshops requiring deep sanitization and degreasing. Manufacturers are developing heavy-duty units designed for long operational cycles and enhanced temperature consistency.

Application Insights

Residential use represents the largest application segment, comprising 45–50% of global demand in 2025. Growth is fueled by post-pandemic hygiene awareness and increasing demand for eco-friendly household products. Commercial applications, hotels, offices, malls, and cleaning services, are the fastest-growing due to rising institutional hygiene standards.

Industrial applications, including pharmaceutical plants, food processing facilities, automotive factories, and heavy-equipment workshops, are adopting high-pressure units for compliance-driven cleaning. New applications such as automotive detailing and school sanitation programs are broadening the scope for steam cleaner adoption.

Distribution Channel Insights

Online retail dominates steam cleaner distribution, accounting for 30–35% of global sales in 2025. E-commerce platforms provide price transparency, diverse model availability, and review-based purchasing decisions, particularly appealing to younger consumers. Specialty home appliance stores and industrial distributors continue to serve as crucial offline channels, especially for high-end or industrial-grade models.

Direct B2B sales remain essential for industrial steam cleaners, where buyers require customized configurations, servicing contracts, and installation assistance. Hybrid online-offline models are expanding as global brands strengthen omnichannel footprints.

Explore more data points, trends and opportunities Download Free Sample Report

Steam Cleaner Market Segmentations

By Product Type

- Handheld Steam Cleaners

- Steam Mops / Floor Steam Cleaners

- Steam Vacuum Cleaners (Hybrid Models)

- Garment / Fabric Steamers

- Industrial High-Pressure Steam Cleaners

- Portable / Mobile Industrial Steam Cleaners

By Power Source

- Electric Steam Cleaners

- Battery-Operated / Cordless Steam Cleaners

- Gas / Fuel-Based Industrial Steam Cleaners

By Distribution Channel

- Online Retail

- Specialty Stores / Appliance Retailers

- Direct B2B Sales

- Wholesale & Institutional Procurement

By End-Use

- Residential

- Commercial (Offices, Retail, Hospitality)

- Industrial / Manufacturing

- Institutional (Healthcare, Schools, Public Facilities)

Regional Insights

North America

North America accounts for 25–30% of the global market share. High hygiene awareness, strong purchasing power, and wide availability of premium products support growth. The U.S. leads with substantial adoption in both residential and commercial spaces, particularly in hospitality and healthcare.

Europe

Europe holds 20–25% of the global market, driven by a strong preference for eco-friendly cleaning and strict sanitation regulations. Germany, the U.K., Italy, and France dominate regional demand. Residential adoption is high due to energy-efficient appliance standards and advanced retail ecosystems.

Asia-Pacific

Asia-Pacific is the fastest-growing region, accounting for 30–35% market share in 2025. Demand is driven by urbanization, growing middle-class incomes, and expanding commercial infrastructure in China, India, Japan, and Southeast Asia. APAC’s dynamic e-commerce sector accelerates household adoption.

Latin America

Latin America comprises 8–10% of the market. Brazil and Mexico lead demand for residential appliances and commercial cleaning solutions. Economic improvements and increasing urban lifestyles continue to support expansion in mid-range product segments.

Middle East & Africa

MEA accounts for 5–8% of the global share. High commercial and hospitality growth in the UAE, South Africa, and Saudi Arabia is boosting demand for both portable and industrial-grade equipment. Rising hygiene standards in schools, hospitals, and shopping centers also contribute.