Stationery Product Market Size

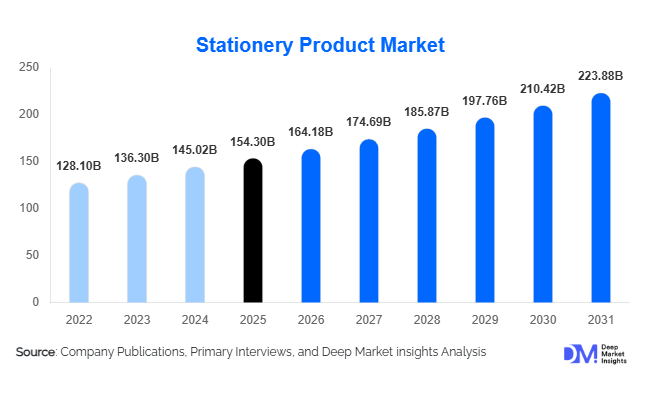

According to Deep Market Insights, the global stationery product market size was valued at USD 154.3 billion in 2025 and is projected to grow from USD 164.18 billion in 2026 to reach USD 223.88 billion by 2031, expanding at a CAGR of 6.4% during the forecast period (2026–2031). The stationery product market growth is primarily driven by rising global education enrollment, expansion of hybrid work environments, increasing demand for creative and journaling products, and the growing adoption of sustainable and premium stationery solutions. Despite ongoing digitalization trends, stationery continues to remain an essential category across educational institutions, corporate offices, households, and creative industries worldwide.

Key Market Insights

- Education sector expansion remains the primary demand driver, particularly across Asia-Pacific and emerging economies with rising literacy initiatives.

- Premium and personalized stationery products are gaining popularity, supported by lifestyle branding and corporate gifting trends.

- Asia-Pacific dominates global production and consumption, led by China and India’s large student populations and manufacturing ecosystems.

- E-commerce channels are reshaping purchasing behavior, enabling direct-to-consumer customization and subscription-based stationery models.

- Sustainable stationery solutions, including recycled paper and refillable writing instruments, are rapidly gaining traction.

- Creative hobbies and journaling culture are accelerating growth in art and specialty stationery segments globally.

What are the latest trends in the stationery product market?

Sustainable and Eco-Friendly Stationery Adoption

Environmental awareness among consumers and corporate buyers is transforming product development strategies in the stationery market. Manufacturers are increasingly introducing recycled notebooks, biodegradable packaging, refillable pens, and FSC-certified paper products to comply with sustainability standards. Institutional buyers, including schools and corporations, are prioritizing environmentally responsible procurement, encouraging manufacturers to redesign supply chains and materials sourcing. Eco-labeling and green certifications are becoming strong differentiators, allowing brands to capture premium pricing while aligning with global ESG commitments.

Rise of Lifestyle and Creative Stationery

Stationery is evolving beyond functional office supplies into lifestyle and self-expression products. Journaling, calligraphy, sketching, and planner culture have gained global momentum through social media influence. Consumers increasingly seek aesthetically designed notebooks, colored pens, and themed stationery collections. Influencer-driven product launches and limited-edition collections are creating recurring demand cycles. Creative stationery is particularly popular among younger demographics and remote workers seeking productivity tools that blend creativity with organization.

What are the key drivers in the stationery product market?

Expansion of Global Education Infrastructure

Rising student enrollment worldwide continues to sustain consistent demand for writing instruments, notebooks, and educational stationery. Governments across developing economies are investing heavily in school infrastructure and literacy programs, directly increasing bulk procurement volumes. Educational institutions account for the largest consumption share, ensuring stable baseline demand irrespective of economic cycles.

Hybrid Work and Productivity Culture

The shift toward hybrid work models has reinforced the importance of physical note-taking and workspace organization tools. Professionals increasingly rely on planners, sticky notes, and desk organization products to manage productivity. Companies also use branded stationery to reinforce corporate identity and employee engagement, contributing to steady office supply demand even in digitally enabled workplaces.

What are the restraints for the global market?

Digital Substitution and Paperless Workflows

Digital documentation tools and cloud-based collaboration platforms continue to reduce long-term paper consumption in corporate environments. Organizations adopting paperless operations limit growth potential for traditional paper stationery categories, compelling manufacturers to diversify into premium and creative segments.

Raw Material Price Volatility

Fluctuations in pulp, paper, and plastic resin prices significantly impact manufacturing costs. Since stationery products are price-sensitive in emerging markets, manufacturers face margin pressure when input costs rise. Supply chain disruptions and energy cost inflation further amplify pricing challenges.

What are the key opportunities in the stationery product industry?

Premiumization and Personalization

Consumers increasingly value customized and premium stationery products, including executive notebooks, luxury pens, and branded corporate gifting kits. Personalization technologies such as digital printing and on-demand customization allow companies to offer higher-margin products and strengthen customer loyalty.

Emerging Market Education Demand

Rapid urbanization and expanding middle-class populations in India, Southeast Asia, and Africa present significant opportunities. Localized manufacturing and affordable product innovation enable companies to penetrate price-sensitive but high-volume markets, ensuring long-term revenue growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 154.30 Billion |

| Market Size in 2026 | USD 164.18 Billion |

| Market Size in 2031 | USD 223.88 Billion |

| CAGR | 6.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global stationery products market is segmented across multiple product categories, each contributing distinct value propositions and growth dynamics. Writing instruments represent the largest product segment, accounting for approximately 28% of the global market. Their dominance is primarily driven by continuous and recurring consumption across educational institutions, corporate offices, and government organizations where pens, pencils, and markers remain essential daily tools. The leading driver for this segment is the consistent demand generated by academic enrollment growth and workplace documentation needs, combined with increasing innovation in ergonomic design, refillable formats, and premium writing experiences that encourage repeat purchases.Paper products follow closely with a 26% market share, supported by sustained academic usage alongside expanding lifestyle trends such as journaling, note-taking, and productivity planning. The leading growth driver for paper products is the resurgence of analog productivity methods as consumers seek reduced digital fatigue and improved focus through physical writing formats. Additionally, eco-certified paper materials and recycled notebooks are gaining popularity, particularly among environmentally conscious consumers and institutions implementing sustainability procurement policies.Educational stationery contributes nearly 15% of total demand and benefits significantly from institutional procurement programs and government-led literacy initiatives worldwide. The primary driver for this segment is expanding global student populations, especially in emerging economies where investments in school infrastructure and digital-plus-physical hybrid learning models continue to increase supply requirements.

Office organization supplies account for approximately 14% of the market, supported by hybrid work adoption and increasing home-office setups. The leading driver for this category is workspace optimization, as professionals seek productivity-enhancing solutions such as file organizers, planners, and desk accessories that support efficient work environments both at home and in corporate settings.Art and creative supplies hold around 12% share and represent the fastest-growing product category. Growth is largely driven by rising participation in creative hobbies, DIY crafts, and therapeutic art activities. Social media influence, online tutorials, and growing interest in creative self-expression have significantly expanded the consumer base beyond professional artists to include students and hobbyists.Premium and corporate stationery, while smaller at approximately 5% market share, generates higher profit margins and strong brand loyalty. The leading driver for this segment is the increasing demand for personalized, luxury, and gifting-oriented stationery products used in corporate branding, executive gifting, and special occasions. Customization capabilities and design-focused branding strategies continue to elevate this category’s value contribution.

Application Insights

Educational institutions remain the dominant application segment, contributing nearly 42% of global stationery demand. Growth is primarily driven by rising global enrollment rates, curriculum expansion, and government-supported education programs that require continuous replenishment of writing and paper supplies. The leading driver within this segment is recurring academic consumption, ensuring stable demand cycles aligned with school calendars worldwide.Corporate offices account for approximately 27% of total consumption, supported by hybrid workplace models and increasing emphasis on professional organization and brand identity. Businesses continue investing in branded stationery, documentation tools, and office organization products to enhance operational efficiency and reinforce corporate image. The shift toward collaborative workspaces and employee productivity initiatives further strengthens demand.

Household and personal usage represents one of the fastest-growing application areas, fueled by lifestyle-oriented stationery adoption. Consumers increasingly use planners, journals, and creative supplies for personal organization, mindfulness practices, and hobby engagement. The leading driver for this segment is the growing integration of stationery into wellness and productivity lifestyles, particularly among younger demographics.Art professionals and designers utilize specialty stationery products for illustration, drafting, and creative production, contributing to steady niche demand. Meanwhile, emerging applications such as therapy journaling, productivity coaching tools, and subscription-based planner ecosystems are expanding stationery usage beyond traditional academic and office environments, creating new revenue streams and diversified consumer engagement.

Distribution Channel Insights

Offline retail channels, including dedicated stationery stores, supermarkets, and hypermarkets, continue to dominate global sales with approximately 65% market share. Physical retail remains strong due to immediate product availability, tactile purchasing experiences, and established distribution networks, particularly in developing economies where traditional retail infrastructure remains central to consumer purchasing behavior.Online platforms represent the fastest-growing distribution channel, driven by increasing digital adoption, convenience, and access to wider product assortments. The leading driver for online growth is product customization and direct brand engagement, allowing consumers to personalize stationery products while benefiting from competitive pricing and subscription delivery models.

Institutional procurement remains a critical distribution pathway through bulk purchasing agreements with schools, universities, corporations, and government agencies. These long-term contracts provide stable revenue streams for manufacturers and distributors while supporting large-scale educational and administrative supply requirements.Direct-to-consumer brand websites and subscription-based sales models are emerging as influential channels, particularly for premium and niche stationery brands. These platforms enable stronger brand storytelling, customer loyalty programs, and recurring revenue generation through curated stationery kits and planner subscriptions.

End-Use Insights

Educational end users lead overall consumption due to recurring academic requirements and structured procurement cycles. The leading driver in this segment is consistent institutional demand supported by public education investments, textbook integration, and standardized learning materials that require complementary stationery supplies.Corporate users remain significant contributors, purchasing organizational products, documentation tools, and branded materials for internal operations and external communication. Increasing emphasis on workplace productivity and professional presentation continues to sustain demand across this segment.

Household users represent the fastest-growing end-use category, driven by lifestyle adoption of stationery for planning, journaling, crafting, and personal organization. Rising interest in analog productivity systems and creative hobbies has expanded stationery consumption beyond necessity-based purchasing toward experience-driven buying behavior.Government agencies and public institutions also contribute substantial demand through administrative operations and educational supply distribution programs. This is particularly evident in developing regions investing heavily in public infrastructure, literacy programs, and administrative modernization initiatives.

Explore more data points, trends and opportunities Download Free Sample Report

Stationery Product Market Segmentations

By Product Type

- Writing Instruments

- Paper Products

- Office Organization Supplies

- Art & Creative Supplies

- Educational Stationery

- Premium & Corporate Stationery

By Application / End Use

- Educational Institutions

- Corporate Offices

- Household & Personal Use

- Art & Creative Professionals

- Government & Public Sector

By Distribution Channel

- Offline Retail Stores

- Online Retail & E-commerce

- Institutional Procurement (B2B)

- Wholesale & Distributors

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global stationery products market, accounting for approximately 41% market share in 2025. China remains the global manufacturing hub due to large-scale production capabilities, cost efficiencies, and extensive export networks. India represents one of the fastest-growing consumption markets, supported by expanding education infrastructure, rising literacy rates, and increasing disposable income among middle-class populations. Key regional growth drivers include rapid urbanization, large student populations, government education spending, and expanding e-commerce penetration across Southeast Asia. Countries such as Indonesia, Vietnam, and the Philippines are experiencing accelerating demand as improving access to education and retail modernization enhance stationery accessibility.

North America

North America accounts for nearly 23% of global demand, led primarily by the United States. Regional growth is driven by strong adoption of premium stationery, creative supplies, and corporate branding products. Consumers increasingly view stationery as lifestyle and productivity tools rather than purely functional items. Key growth drivers include high consumer purchasing power, rising popularity of journaling and planning culture, expansion of home-office environments, and growing demand for personalized and design-focused stationery products. The presence of established retail chains and advanced e-commerce infrastructure further supports consistent market expansion.

Europe

Europe holds approximately 20% market share, with Germany, France, and the United Kingdom serving as major contributors. The region emphasizes sustainability and product quality, driving strong adoption of eco-friendly stationery solutions. Regional growth is supported by stringent environmental regulations encouraging recycled materials, FSC-certified paper products, and refillable writing instruments. Consumer preference for premium craftsmanship and durable products also supports higher-value segments, particularly in writing instruments and specialty paper goods. Increasing awareness of sustainable consumption practices remains the primary driver shaping long-term market growth across Europe.

Latin America

Latin America demonstrates steady market expansion, led by Brazil and Mexico. Growth is primarily supported by expanding education systems, improving retail penetration, and rising urban populations. Regional demand benefits from increasing school enrollment rates and government initiatives focused on improving educational accessibility. The leading drivers include urbanization, modernization of retail distribution channels, and growing middle-class consumption patterns that encourage higher spending on educational and personal stationery products.

Middle East & Africa

The Middle East and Africa region represents the fastest-growing market, expanding at nearly 7.5% CAGR. Growth is strongly supported by large-scale investments in education infrastructure across Saudi Arabia, the United Arab Emirates, and several African nations. Increasing private school enrollment, a rapidly growing youth population, and government-led literacy initiatives significantly boost stationery procurement. Additional regional drivers include economic diversification programs, expanding retail networks, and rising awareness of educational development as a key economic priority, positioning the region for sustained long-term demand growth.

Key Players in the Stationery Product Market

- Newell Brands

- BIC Group

- Pilot Corporation

- Faber-Castell AG

- Kokuyo Co., Ltd.

- Mitsubishi Pencil Co.

- Staedtler Mars GmbH

- Pentel Co., Ltd.

- ACCO Brands Corporation

- ITC Limited

- Navneet Education Limited

- Maped Group

- Zebra Co., Ltd.

- Linc Limited

- DOMS Industries Ltd.