Sports Wearables Market Size

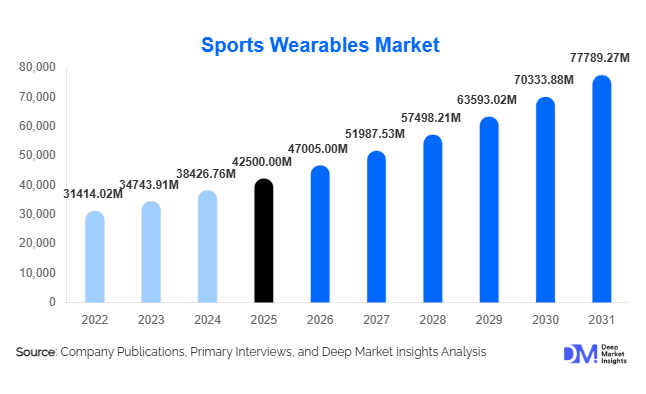

According to Deep Market Insights, the global sports wearables market size was valued at USD 42,500 million in 2025 and is projected to grow from USD 47,005.00 million in 2026 to reach USD 77,789.27 million by 2031, expanding at a CAGR of 10.6% during the forecast period (2026–2031). The sports wearables market growth is primarily driven by increasing consumer awareness regarding fitness and preventive healthcare, rising adoption of connected devices, and continuous advancements in sensor technologies and AI-based analytics.

Key Market Insights

- Smartwatches and fitness trackers dominate the market, accounting for a significant share due to multifunctionality and ease of integration with smartphones.

- AI-driven analytics and personalized insights are transforming wearables from tracking tools into predictive health and performance systems.

- North America leads the global market, supported by high disposable income and early technology adoption.

- Asia-Pacific is the fastest-growing region, driven by expanding middle-class populations and increasing fitness awareness.

- Online distribution channels dominate, benefiting from convenience, competitive pricing, and product accessibility.

- Integration with healthcare ecosystems is emerging as a key trend, enabling remote monitoring and preventive care.

What are the latest trends in the sports wearables market?

AI-Driven Personalization and Predictive Analytics

Sports wearables are increasingly incorporating artificial intelligence to provide personalized fitness recommendations and predictive health insights. Devices now analyze user behavior, physiological metrics, and activity patterns to offer tailored training plans, recovery guidance, and injury prevention alerts. This shift toward intelligent wearables is enhancing user engagement and creating new revenue streams through subscription-based services. AI integration is particularly valuable for professional athletes, where data-driven performance optimization can significantly impact outcomes.

Expansion of Smart Clothing and Embedded Wearables

Smart clothing is emerging as a transformative segment within the sports wearables market. Embedded sensors in garments enable seamless monitoring of muscle activity, posture, and movement without the need for additional devices. This trend is gaining traction among professional athletes and fitness enthusiasts seeking more accurate and unobtrusive data collection. Advances in textile technology and miniaturization of sensors are making smart apparel more practical and commercially viable, expanding its adoption across sports training and rehabilitation applications.

What are the key drivers in the sports wearables market?

Rising Health and Fitness Awareness

Growing global awareness around health, fitness, and preventive care is a primary driver of the sports wearables market. Consumers are increasingly adopting devices that track physical activity, heart rate, sleep patterns, and overall wellness. This trend has been further accelerated by lifestyle changes and the increasing prevalence of chronic diseases, prompting individuals to monitor their health proactively.

Technological Advancements in Sensors and Connectivity

Continuous improvements in sensor accuracy, battery efficiency, and connectivity technologies such as Bluetooth and 5G are significantly enhancing wearable functionality. Modern devices offer real-time tracking, seamless data synchronization, and integration with digital ecosystems, improving user experience and driving widespread adoption.

Growing Adoption in Professional Sports

Professional sports teams and organizations are increasingly using wearables for performance monitoring, injury prevention, and training optimization. This adoption is driving innovation and setting benchmarks for consumer devices, as technologies initially developed for elite athletes gradually become accessible to the broader market.

What are the restraints for the global market?

Data Privacy and Security Concerns

Sports wearables collect sensitive personal and health data, raising concerns about data privacy and cybersecurity. Any breach or misuse of data can negatively impact consumer trust and hinder adoption. Regulatory compliance and robust data protection measures are essential but increase operational complexity for manufacturers.

High Cost of Advanced Wearables

While entry-level devices are becoming more affordable, advanced wearables with sophisticated features remain expensive. This limits adoption in price-sensitive markets and creates a barrier for widespread penetration, particularly in developing economies.

What are the key opportunities in the sports wearables industry?

Integration with Healthcare and Telemedicine

The convergence of sports wearables with healthcare systems presents a significant opportunity for market expansion. Wearables are increasingly being used for continuous health monitoring, enabling remote patient care and early diagnosis of medical conditions. Partnerships with healthcare providers and insurance companies can unlock new revenue streams and enhance device utility beyond fitness tracking.

Expansion in Emerging Markets

Emerging economies in Asia-Pacific, Latin America, and Africa offer substantial growth potential due to rising disposable incomes, increasing smartphone penetration, and growing awareness of fitness and wellness. Companies focusing on affordable and feature-rich devices can capture significant market share in these regions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 42500 Million |

| Market Size in 2026 | USD 47005 Million |

| Market Size in 2031 | USD 77789.27 Million |

| CAGR | 10.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Smartwatches lead the sports wearables market, accounting for approximately 38% of the total market share in 2025. Their dominance is primarily driven by multifunctional capabilities, combining fitness tracking, heart rate monitoring, GPS tracking, communication, and app integration in a single device. Smartwatches appeal to both professional athletes and general consumers, offering real-time performance analytics, connectivity with smartphones, and lifestyle applications. Fitness trackers closely follow, particularly in the entry-level segment, providing cost-effective solutions for basic activity monitoring. Emerging product types, such as smart clothing and smart footwear, are gaining traction due to their specialized applications in muscle activity monitoring, gait analysis, and training optimization. The adoption of these advanced wearables is being further boosted by technological advancements in embedded sensors, flexible electronics, and AI-driven analytics, which allow more precise tracking of performance metrics in both professional and recreational settings.

Application Insights

Fitness and activity monitoring remains the dominant application segment, holding nearly 40% of the market share. This is largely driven by the widespread adoption among general consumers seeking to maintain health, track workouts, and manage lifestyle-related metrics. Performance monitoring is rapidly gaining prominence, particularly among professional athletes and sports teams, as wearables provide actionable insights for training optimization and injury prevention. Health monitoring applications are also expanding, fueled by integration with medical and wellness ecosystems. Features such as sleep tracking, heart rate variability monitoring, and oxygen saturation measurement are increasingly used in preventive healthcare, rehabilitation, and remote patient monitoring, further widening the applicability and value of wearables across multiple sectors.

Distribution Channel Insights

Online retail channels dominate the market, contributing approximately 55% of total sales. Growth is supported by e-commerce platforms offering convenience, a wide range of options, competitive pricing, and home delivery. Offline retail, including specialty sports stores, electronics retailers, and brand-specific outlets, continues to play a vital role, particularly for high-value and premium devices where consumers prefer hands-on evaluation and personalized assistance. Hybrid distribution strategies, combining online platforms with experiential stores, are also emerging as a growth driver, enhancing brand visibility and consumer trust while reaching diverse customer segments.

End-User Insights

Fitness enthusiasts represent the largest end-user segment, accounting for nearly 50% of the market share. Their growth is driven by increasing participation in gym memberships, home fitness programs, and outdoor sports activities, as well as rising awareness of preventive healthcare. Professional athletes and sports teams remain high-value users, leveraging wearables for performance analytics, training optimization, and injury prevention. Healthcare and rehabilitation centers are emerging as fast-growing segments, adopting wearables for patient monitoring, post-operative recovery, and remote health tracking. The expanding use of wearables in corporate wellness programs and insurance-driven health initiatives is also contributing to this segment’s growth.

Explore more data points, trends and opportunities Download Free Sample Report

Sports Wearables Market Segmentations

By Product Type

- Smartwatches

- Fitness Trackers

- Smart Clothing

- Smart Footwear

- Chest Straps & Heart Rate Monitors

- Smart Glasses & AR Wearables

By Application

- Fitness & Activity Monitoring

- Performance Monitoring

- Health Monitoring

- Injury Prevention & Rehabilitation

- Coaching & Training Optimization

By End-User

- Fitness Enthusiasts

- Professional Athletes & Sports Teams

- Healthcare & Rehabilitation Centers

- Military & Defense Training Units

By Distribution Channel

- Online Retail

- Specialty Sports Stores

- Electronics Retailers

- Brand Stores / Flagship Stores

Regional Insights

North America

North America dominates the sports wearables market, accounting for approximately 35% of the global market share in 2025. Growth is driven by high consumer awareness of fitness and health monitoring, high disposable income, and a culture of early technology adoption. The United States, as the largest contributor, benefits from well-established fitness ecosystems, widespread gym infrastructure, and strong brand presence of leading wearables manufacturers. Key growth drivers include the integration of AI-based analytics in consumer devices, the expansion of online retail platforms, and the increasing adoption of digital health programs in both corporate and healthcare settings. The region’s robust smartphone penetration and high-tech lifestyle culture further reinforce the adoption of smartwatches and advanced wearables.

Asia-Pacific

Asia-Pacific holds around 30% market share and is the fastest-growing region, with countries such as China, India, and Japan driving demand. China leads manufacturing and consumption due to its technological infrastructure and strong presence of local manufacturers, while India is witnessing rapid growth with a CAGR exceeding 12%, fueled by increasing fitness awareness, rising disposable incomes, and expanding smartphone penetration. Key drivers include government-led health initiatives, growing middle-class urban populations, and rising interest in wearable-integrated wellness programs. Japan and South Korea benefit from tech-savvy consumers who adopt advanced wearables for both professional and lifestyle applications. Online retail platforms and cross-border exports further support regional expansion.

Europe

Europe accounts for nearly 20% of the global market, with Germany, the UK, and France as major contributors. The region’s growth is driven by strong health consciousness, supportive regulatory frameworks for medical-grade devices, and increasing adoption of digital health technologies. Consumers in Europe favor multifunctional smartwatches and sensor-based wearables that provide both fitness and medical insights. Growth is further supported by the increasing integration of wearables into corporate wellness programs, health insurance incentives, and widespread participation in organized fitness activities, driving demand for reliable, high-quality devices.

Latin America

Latin America is an emerging market, led by Brazil and Mexico, where sports wearables adoption is accelerating due to increasing urbanization, rising disposable incomes, and growing awareness of personal fitness and wellness. The availability of affordable fitness trackers and smartwatches, combined with the expansion of online retail infrastructure, is fueling market penetration. Key drivers include rising participation in recreational sports, government programs promoting physical activity, and growing consumer preference for connected health devices in urban centers.

Middle East & Africa

The Middle East & Africa region is witnessing steady growth, particularly in the UAE and Saudi Arabia. High disposable incomes, increasing interest in wellness and fitness, and growing urbanization are driving demand. Investments in healthcare infrastructure, corporate wellness programs, and integration of wearables into preventive health initiatives are additional growth enablers. The adoption of high-end smartwatches and AI-enabled wearables is being supported by lifestyle-focused consumers, expatriate populations, and government campaigns promoting active and healthy living. In Africa, emerging urban fitness hubs and local technology initiatives are beginning to create new opportunities for wearable manufacturers.

Key Players in the Sports Wearables Market

- Apple Inc.

- Samsung Electronics

- Garmin Ltd.

- Fitbit (Google)

- Xiaomi Corporation

- Huawei Technologies

- Polar Electro

- Suunto

- Whoop Inc.

- Oura Health

- Zepp Health (Amazfit)

- Under Armour

- Sony Corporation

- Bose Corporation

- Nike Inc.