SPC Flooring Market Size

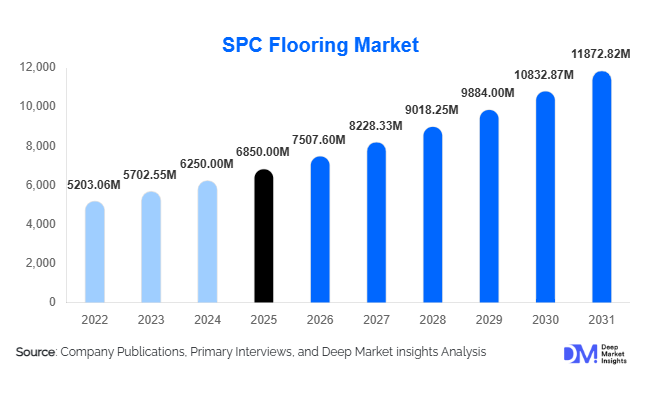

According to Deep Market Insights, the global SPC (Stone Plastic Composite) flooring market size was valued at USD 6,850 million in 2025 and is projected to grow from USD 7507.60 million in 2026 to reach USD 11,872.82 million by 2031, expanding at a CAGR of 9.6% during the forecast period (2026–2031). The SPC flooring market growth is primarily driven by increasing demand for durable, water-resistant, and cost-effective flooring solutions across residential and commercial construction sectors. Rising urbanization, rapid infrastructure development, and the growing trend of home renovation are further accelerating adoption globally.

Key Market Insights

- Rigid core SPC flooring dominates the market, accounting for over 60% share due to its superior durability and dimensional stability.

- Wood-look designs lead the aesthetic segment, capturing more than half of global demand driven by consumer preference for natural finishes.

- Asia-Pacific dominates the global market, supported by strong manufacturing capabilities and expanding construction activity.

- Commercial infrastructure expansion, particularly in healthcare and retail, is driving high-volume adoption of SPC flooring.

- Click-lock installation systems are gaining traction, fueled by DIY trends and ease of installation.

- Technological advancements in digital printing and coatings are enhancing product quality and differentiation.

What are the latest trends in the SPC flooring market?

Rise of Sustainable and Low-VOC Flooring Solutions

Sustainability has become a defining trend in the SPC flooring market, with manufacturers increasingly focusing on low-VOC emissions and recyclable materials. Regulatory frameworks promoting green buildings are encouraging the use of eco-friendly flooring products. SPC flooring aligns well with these requirements due to its composition and durability, reducing replacement cycles and environmental impact. Manufacturers are also introducing certifications and eco-labeling to enhance product transparency, which is influencing purchasing decisions in both residential and commercial sectors.

Advanced Design and Digital Printing Innovations

Technological advancements in high-definition digital printing and embossing techniques are transforming SPC flooring aesthetics. Manufacturers are now able to replicate natural materials such as hardwood and stone with high precision, improving visual appeal while maintaining cost efficiency. This trend is particularly appealing in premium residential and hospitality segments, where design plays a critical role. Enhanced surface coatings are also improving scratch resistance and longevity, making SPC flooring a competitive alternative to traditional materials.

What are the key drivers in the SPC flooring market?

Growth in Residential Renovation Activities

The surge in home renovation and remodeling projects is a major driver for SPC flooring demand. Consumers are increasingly opting for flooring solutions that are easy to install, low-maintenance, and cost-effective. SPC flooring’s click-lock installation system and durability make it ideal for DIY projects, especially in developed markets such as North America and Europe. Rising disposable incomes and changing lifestyle preferences are further boosting renovation spending globally.

Expansion of Commercial Infrastructure

The rapid development of commercial spaces, including offices, retail outlets, hospitals, and educational institutions, is significantly contributing to market growth. SPC flooring’s resistance to heavy foot traffic, moisture, and wear makes it suitable for high-performance environments. The recovery of global tourism and retail sectors is also driving demand in hospitality and retail applications, further strengthening market expansion.

What are the restraints for the global market?

Raw Material Price Volatility

Fluctuations in the prices of key raw materials such as PVC and limestone pose a challenge to manufacturers. These variations impact production costs and profit margins, creating pricing pressure across the value chain. Manufacturers must adopt cost optimization strategies and diversify sourcing to mitigate these risks.

Intense Market Competition

The SPC flooring market is highly competitive, with numerous regional and global players entering the market. This has led to aggressive pricing strategies and margin compression, particularly in the mid-range segment. Maintaining product differentiation and brand value remains a key challenge for market participants.

What are the key opportunities in the SPC flooring industry?

Expansion into Emerging Markets

Emerging economies in Asia-Pacific, Latin America, and Africa present significant growth opportunities due to rapid urbanization and increasing housing demand. SPC flooring’s affordability and performance advantages make it well-suited for these markets. Government housing initiatives and infrastructure projects are further creating large-scale demand for flooring materials.

Technological Product Differentiation

Innovation in product features such as anti-bacterial coatings, acoustic insulation, and enhanced durability is creating opportunities for premium offerings. Manufacturers investing in R&D can capture higher margins and differentiate themselves in a competitive market. Integration of smart features and customization options is also emerging as a niche growth area.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 6850 Million |

| Market Size in 2026 | USD 7507.60 Million |

| Market Size in 2031 | USD 11872.82 Million |

| CAGR | 9.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Rigid core SPC flooring dominates the global market, accounting for approximately 62% of total market share in 2025. This segment’s leadership is primarily driven by its superior dimensional stability, impact resistance, and waterproof properties, making it highly suitable for both residential and high-traffic commercial environments. The rigid limestone-based core enhances durability and prevents expansion or contraction under temperature fluctuations, which is a critical advantage over traditional vinyl flooring. Additionally, increasing demand for low-maintenance and long-lasting flooring solutions in renovation projects has significantly boosted the adoption of rigid core variants. While flexible SPC flooring continues to find applications in cost-sensitive markets, acoustic-backed SPC flooring is gaining traction in premium segments such as offices, hotels, and multi-family housing, where sound insulation is a key requirement. However, these remain niche compared to the dominant rigid core segment due to higher costs and limited mass adoption.

Application Insights

Indoor applications dominate the SPC flooring market, contributing over 85% of total demand, driven by widespread use in residential, commercial, and institutional spaces. The primary growth driver for this segment is the increasing preference for moisture-resistant and easy-to-install flooring solutions in kitchens, living areas, offices, and retail spaces. Residential applications lead in volume due to rising home renovation activities and increasing consumer awareness of SPC flooring benefits such as durability and aesthetic versatility. Meanwhile, commercial applications, including healthcare, hospitality, and retail, are witnessing faster growth rates, supported by the need for high-performance flooring capable of withstanding heavy foot traffic and strict hygiene requirements. Additionally, emerging applications in modular construction and prefabricated housing are expanding demand, as SPC flooring aligns well with the need for quick installation and standardized building components.

Distribution Channel Insights

Distributors and wholesalers account for the largest share of SPC flooring sales, contributing around 46% of the market. This dominance is driven by well-established supply chains, strong relationships with contractors, and the ability to handle bulk procurement for large construction and renovation projects. The key growth driver for this segment is the continued reliance of builders and commercial buyers on trusted distribution networks for consistent supply and product availability. Retail stores also play a significant role in serving individual consumers and small contractors. However, e-commerce platforms are rapidly gaining traction, particularly in developed markets, due to increasing digitalization and changing purchasing behaviors. Online platforms offer advantages such as price transparency, product comparison, and doorstep delivery, making them attractive for DIY consumers and small-scale projects. This shift is expected to gradually reshape the distribution landscape over the forecast period.

End-Use Insights

The residential segment remains the largest end-use category, with a market size exceeding USD 3,200 million in 2025. This dominance is driven by rising housing construction, increased renovation spending, and growing consumer preference for cost-effective yet aesthetically appealing flooring solutions. SPC flooring’s ease of installation and low maintenance requirements make it particularly attractive for homeowners. However, the commercial segment is the fastest growing, supported by rapid expansion in infrastructure and commercial real estate. Sectors such as healthcare and hospitality are key growth drivers due to their need for durable, hygienic, and visually appealing flooring. Healthcare facilities, in particular, require flooring solutions that are resistant to moisture and easy to sanitize, while hospitality spaces prioritize aesthetics and durability. Industrial applications, although smaller in share, are stable and driven by demand for heavy-duty flooring in warehouses and manufacturing facilities.

Explore more data points, trends and opportunities Download Free Sample Report

SPC Flooring Market Segmentations

By Product Type

- Rigid Core SPC Flooring

- Flexible SPC Flooring

- Acoustic Backed SPC Flooring

- Anti-Slip / Textured SPC Flooring

By Application

- Indoor Flooring

- Outdoor / Semi-Outdoor Flooring

By Distribution Channel

- Direct Sales (B2B)

- Distributors / Wholesalers

- Retail Stores

- E-commerce Platforms

Regional Insights

Asia-Pacific

Asia-Pacific leads the SPC flooring market with approximately 42% share in 2025, driven by a combination of strong manufacturing capacity and rapidly growing domestic demand. China remains the largest producer and exporter, benefiting from cost-efficient production and established supply chains. India, Vietnam, and Indonesia are emerging as high-growth markets due to rapid urbanization, increasing disposable incomes, and government-led infrastructure and housing initiatives. The key drivers for regional growth include large-scale construction activities, expansion of affordable housing projects, and rising adoption of modern building materials. Additionally, the presence of major manufacturing hubs enables competitive pricing and supports export-driven growth.

North America

North America holds around 26% of the global market, with the United States accounting for the majority of demand. The region’s growth is primarily driven by strong residential renovation activity, high consumer awareness, and a preference for premium and technologically advanced flooring solutions. The increasing trend of DIY home improvement projects is also boosting demand for click-lock SPC flooring. Furthermore, the commercial sector, particularly retail and healthcare, is contributing to market expansion due to the need for durable and low-maintenance flooring. Well-developed distribution networks and a strong presence of leading manufacturers further support regional growth.

Europe

Europe accounts for approximately 20% market share, with key markets including Germany, the UK, and France. Growth in this region is largely driven by stringent environmental regulations and increasing demand for sustainable and low-emission building materials. SPC flooring’s compliance with eco-friendly standards makes it an attractive option for both residential and commercial applications. Additionally, renovation activities across aging building infrastructure in Western Europe are boosting demand. The commercial sector, particularly offices and hospitality, is also contributing to growth due to increasing emphasis on aesthetic and functional flooring solutions.

Middle East & Africa

The Middle East and Africa region is an emerging market for SPC flooring, supported by large-scale infrastructure and real estate projects in countries such as the UAE and Saudi Arabia. The primary growth drivers include increasing investments in tourism, hospitality, and commercial construction. Mega projects and smart city initiatives are creating substantial demand for durable and high-performance flooring materials. In Africa, urbanization and improving economic conditions are gradually driving adoption, although the market remains in an early growth stage compared to other regions.

Latin America

Latin America is gradually expanding, with Brazil and Mexico leading demand. The region’s growth is driven by increasing residential construction, urbanization, and improving economic stability. Rising middle-class populations are boosting demand for affordable and durable flooring solutions, making SPC flooring an attractive option. Additionally, growth in the retail and hospitality sectors is contributing to increased adoption. However, market expansion is somewhat constrained by economic volatility, although long-term prospects remain positive, particularly in mid-range product segments.

Key Players in the SPC Flooring Market

- Shaw Industries Group

- Mohawk Industries

- Tarkett

- Armstrong Flooring

- Mannington Mills

- Gerflor Group

- Forbo Flooring Systems

- Beaulieu International Group

- LG Hausys

- NOX Corporation

- CFL Flooring

- Zhejiang Walrus New Material

- Taide Plastic Flooring

- Kentier Flooring

- Decno Group