Smart Home-Based Beverage Machine Market Size

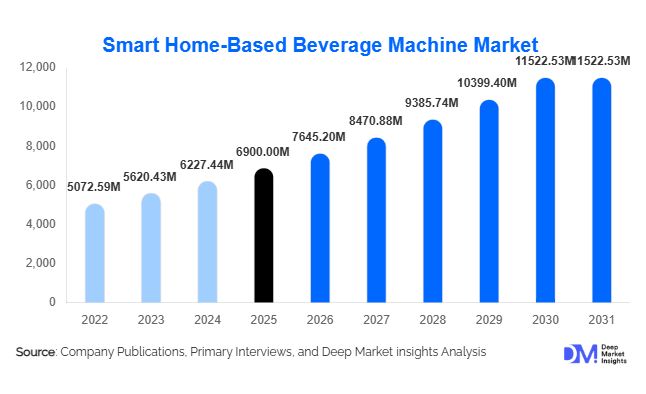

According to Deep Market Insights, the global smart home-based beverage machine market size was valued at USD 6,900 million in 2025 and is projected to grow from USD 7,645.20 million in 2026 to reach USD 11,522.53 million by 2031, expanding at a CAGR of 10.8% during the forecast period (2026–2031). The market growth is primarily driven by the increasing adoption of smart home ecosystems, rising demand for premium in-home beverage experiences, and continuous technological advancements in connected kitchen appliances. The integration of IoT, AI-driven personalization, and app-based controls is transforming traditional beverage machines into intelligent lifestyle devices. Additionally, the shift toward remote work and home-centric consumption patterns has accelerated investments in smart kitchen solutions, further boosting demand for smart coffee machines, multi-beverage systems, and connected brewing technologies globally.

Key Market Insights

- Smart coffee machines dominate the market, accounting for nearly 48% of total demand due to high global coffee consumption and premiumization trends.

- Wi-Fi-enabled machines lead connectivity adoption, contributing over 40% share as consumers prefer remote access and cloud integration.

- North America holds the largest market share (34%), driven by strong smart home adoption and high disposable income.

- Asia-Pacific is the fastest-growing region, with a CAGR exceeding 13% due to urbanization and rising middle-class demand.

- Online retail channels dominate distribution, accounting for approximately 44% of global sales.

- AI-based personalization and subscription ecosystems are emerging as key differentiators among leading manufacturers.

What are the latest trends in the smart home-based beverage machine market?

AI-Driven Personalization Transforming User Experience

One of the most prominent trends in the market is the integration of artificial intelligence for personalized beverage preparation. Smart machines are increasingly capable of learning user preferences, including beverage strength, temperature, and timing, to deliver customized outputs automatically. These systems use data analytics and machine learning algorithms to recommend beverages based on consumption patterns and lifestyle habits. This trend is particularly appealing to tech-savvy consumers seeking convenience and premium experiences. Manufacturers are also integrating mobile applications that allow users to store multiple profiles, making these machines suitable for households with diverse preferences.

Subscription-Based Ecosystems and Smart Refill Models

Another key trend is the rise of subscription-based ingredient ecosystems. Many smart beverage machine manufacturers are offering integrated services that include automatic reordering of coffee pods, tea capsules, and flavor cartridges. This not only ensures consistent product usage but also creates recurring revenue streams for companies. Subscription models enhance customer retention and allow manufacturers to gather valuable consumption data, which can be used to improve product offerings. This trend is particularly strong in developed markets, where convenience and seamless user experiences are highly valued.

What are the key drivers in the smart home-based beverage machine market?

Expansion of Smart Home Ecosystems

The rapid adoption of smart home technologies is a primary driver for the market. Consumers increasingly prefer interconnected devices that can be controlled through centralized platforms such as smartphones or voice assistants. Smart beverage machines fit seamlessly into these ecosystems, offering automation, remote control, and integration with other smart appliances. As smart home penetration continues to rise globally, demand for connected kitchen appliances is expected to increase significantly.

Growing Demand for Premium Home Experiences

The shift toward premium in-home experiences is another major growth driver. Consumers are increasingly investing in high-end appliances that replicate café-quality beverages at home. This trend has been amplified by remote working and changing lifestyle preferences, which have increased the time spent at home. Premium smart espresso machines and multi-beverage systems are particularly benefiting from this trend, as they offer convenience, quality, and customization.

What are the restraints for the global market?

High Initial Cost of Smart Machines

The high upfront cost of smart beverage machines remains a significant barrier to adoption, especially in price-sensitive markets. Premium models often cost substantially more than conventional machines, limiting their accessibility to high-income consumers. While mid-range options are expanding, affordability continues to be a challenge for mass-market penetration.

Ecosystem Dependency and Compatibility Issues

Many smart beverage machines operate within proprietary ecosystems, requiring specific apps or consumables such as branded pods and cartridges. This lack of interoperability can deter consumers who prefer flexibility and compatibility with multiple platforms. Additionally, long-term costs associated with subscription-based models may impact consumer adoption in emerging markets.

What are the key opportunities in the smart home-based beverage machine industry?

Emerging Market Expansion

Emerging economies such as India, China, and Southeast Asian countries present significant growth opportunities due to increasing urbanization and rising disposable incomes. As smart home adoption expands in these regions, demand for mid-range smart beverage machines is expected to grow rapidly. Manufacturers can tap into this opportunity by offering cost-effective products tailored to local preferences.

Integration of AI and Smart Assistants

The integration of AI-driven personalization and voice assistants offers strong opportunities for innovation. Machines that can seamlessly interact with smart home ecosystems and provide predictive recommendations are likely to gain a competitive advantage. This trend will also enhance user engagement and create opportunities for ecosystem-based revenue models.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 6900 Million |

| Market Size in 2026 | USD 7645.20 Million |

| Market Size in 2031 | USD 11522.53 Million |

| CAGR | 10.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Smart coffee machines dominate the product segment, accounting for approximately 48% of the global market in 2025. This leadership is primarily driven by high global coffee consumption, particularly in North America and Europe, where coffee is a daily essential. The increasing preference for café-style beverages at home, coupled with rising disposable incomes and premiumization trends, is further accelerating demand for fully automatic espresso machines and capsule-based systems. Additionally, the integration of AI-driven brewing customization, app-based controls, and voice assistant compatibility has made smart coffee machines the most technologically advanced and widely adopted category.

Smart multi-beverage machines are rapidly gaining traction as a high-growth segment due to their versatility in offering both hot and cold beverages, including coffee, tea, and flavored drinks from a single device. These machines are particularly popular among urban households seeking multifunctional appliances to optimize kitchen space. Meanwhile, smart soda and cold beverage machines are witnessing steady growth, especially among younger consumers and health-conscious users who prefer customizable, low-sugar, and carbonated drink options at home. The expansion of flavored beverage ecosystems and reusable cartridge systems is also contributing to the growth of this segment.

Connectivity Insights

Wi-Fi-enabled beverage machines lead the connectivity segment with over 42% market share, driven by their ability to provide seamless remote operation, real-time monitoring, and integration with cloud-based platforms. These machines allow users to control brewing schedules, customize beverage settings, and receive maintenance alerts through mobile applications, making them highly attractive within modern smart home ecosystems. The increasing penetration of high-speed internet and smart home hubs is further reinforcing the dominance of Wi-Fi connectivity.

Bluetooth-enabled devices are more prevalent in entry-level smart machines, offering basic connectivity features at a lower cost. However, their limited range and functionality compared to Wi-Fi systems restrict their adoption in advanced applications. Voice assistant-compatible machines are rapidly emerging as a key growth segment, supported by the widespread adoption of smart speakers such as Alexa and Google Home. Consumers are increasingly favoring hands-free operation, which enhances convenience and aligns with broader home automation trends. App-controlled systems are now becoming standard across mid-range and premium segments, with manufacturers focusing on enhancing user interfaces, personalization features, and cross-device compatibility.

Distribution Channel Insights

Online retail platforms dominate the distribution landscape, accounting for approximately 44% of global sales. This dominance is driven by the growing preference for digital shopping, where consumers can easily compare features, read reviews, and access competitive pricing. E-commerce platforms also enable manufacturers to reach a global customer base without the constraints of physical retail infrastructure. Promotional discounts, bundled offers, and flexible financing options further enhance online sales growth.

Direct-to-consumer (D2C) sales through brand-owned websites are gaining significant momentum, as they allow manufacturers to establish direct relationships with customers, offer personalized recommendations, and promote subscription-based services for consumables such as coffee pods and flavor cartridges. Offline retail channels, including consumer electronics stores and specialty kitchen appliance outlets, continue to play an important role, particularly in the premium segment where customers prefer in-store demonstrations before making high-value purchases. Hybrid omnichannel strategies are increasingly being adopted to provide a seamless buying experience.

End-Use Insights

Residential smart homes represent the largest end-use segment, contributing approximately 55% of the global market. The rapid adoption of connected home ecosystems and the growing trend of smart kitchens are key drivers for this segment. Consumers are increasingly investing in appliances that offer convenience, automation, and energy efficiency, positioning smart beverage machines as essential components of modern households. The demand is particularly strong among urban, tech-savvy consumers seeking premium lifestyle upgrades.

The small office/home office (SOHO) segment is the fastest-growing end-use category, driven by the global shift toward remote and hybrid work models. Professionals are investing in smart beverage machines to enhance productivity and convenience, reducing reliance on external coffee shops. Additionally, co-living spaces, serviced apartments, and premium rental housing are emerging as new application areas, where property developers integrate smart kitchen appliances to attract high-value tenants. This expansion into semi-commercial residential environments is expected to create new demand avenues for the market.

Explore more data points, trends and opportunities Download Free Sample Report

Smart Home-Based Beverage Machine Market Segmentations

By Product Type

- Smart Coffee Machines

- Smart Tea & Specialty Beverage Machines

- Smart Carbonated & Cold Beverage Machines

- Smart Multi-Beverage Machines

By Connectivity Type

- Wi-Fi Enabled Beverage Machines

- Bluetooth-Connected Beverage Machines

- App-Controlled (Cloud-Integrated) Machines

- Voice-Assistant Compatible Machines

By Distribution Channel

- Online Retail Platforms

- Direct-to-Consumer (Brand Websites)

- Consumer Electronics Retail Stores

- Kitchen Appliance Specialty Stores

- Hypermarkets & Supermarkets

By End-Use

- Residential Smart Homes

- Premium Urban Households

- Small Office/Home Office (SOHO)

- Co-living & Rental Spaces

Regional Insights

North America

North America leads the global market with approximately 34% share in 2025, driven by high smart home penetration, strong consumer purchasing power, and a well-established coffee culture. The United States accounts for the majority of regional demand, supported by widespread adoption of connected appliances and a strong preference for premium lifestyle products. The presence of leading smart appliance manufacturers and advanced retail infrastructure further strengthens market growth. Additionally, the increasing adoption of voice assistants and IoT-enabled home ecosystems is accelerating demand for Wi-Fi-enabled beverage machines. Canada is also experiencing steady growth, driven by rising urbanization, increasing disposable income, and growing interest in smart kitchen solutions.

Europe

Europe holds around 29% of the global market share, with Germany, the United Kingdom, France, and Italy serving as key markets. The region’s strong coffee culture, combined with high consumer awareness of premium appliances, is a major driver of demand. Germany leads the market due to its large consumer base and preference for technologically advanced, energy-efficient appliances. The United Kingdom and France are witnessing increased adoption of smart home technologies, supported by favorable regulations promoting energy efficiency. Additionally, sustainability trends, including demand for recyclable pods and eco-friendly appliances, are influencing purchasing decisions across the region, further supporting market growth.

Asia-Pacific

Asia-Pacific is the fastest-growing region, with a CAGR exceeding 13% during the forecast period. China dominates the regional market due to rapid urbanization, expanding middle-class population, and strong government support for smart home manufacturing. The widespread adoption of IoT devices and competitive pricing strategies by domestic manufacturers are further boosting market growth. India is emerging as a high-growth market, driven by rising disposable incomes, increasing urbanization, and growing awareness of smart appliances among younger consumers. Japan and South Korea also contribute significantly due to their advanced technological infrastructure and high adoption of connected home devices. The region’s growth is further supported by increasing e-commerce penetration and local manufacturing capabilities.

Latin America

Latin America is witnessing moderate growth, led by Brazil and Mexico. Increasing middle-class income, urban expansion, and growing awareness of smart home technologies are key drivers in the region. Brazil represents the largest market due to its sizable population and expanding consumer electronics sector. Mexico is also experiencing steady growth due to its proximity to North American markets and the increasing adoption of connected devices. However, price sensitivity and limited penetration of high-end smart appliances remain key challenges, restricting faster adoption in certain segments.

Middle East & Africa

The Middle East & Africa region is experiencing steady growth, particularly in the UAE and Saudi Arabia, where high-income consumers are investing in premium smart appliances. The region benefits from rapid urbanization, luxury lifestyle preferences, and increasing adoption of smart home technologies in residential developments. Government-led smart city initiatives and real estate developments integrating connected home solutions are further supporting market growth. In Africa, growth is comparatively slower but gradually improving due to increasing urbanization and rising awareness of smart appliances in key economies such as South Africa. Overall, the region presents long-term growth potential driven by infrastructure development and increasing digital connectivity.

Key Players in the Smart Home-Based Beverage Machine Market

- De'Longhi S.p.A.

- Koninklijke Philips N.V.

- Nestlé S.A.

- Breville Group Limited

- Panasonic Corporation

- Electrolux AB

- Haier Smart Home Co., Ltd.

- LG Electronics Inc.

- Samsung Electronics Co., Ltd.

- Xiaomi Corporation

- Jura Elektroapparate AG

- Miele & Cie. KG

- Keurig Dr Pepper Inc.

- Bosch Home Appliances

- Whirlpool Corporation