Smart Fridge Market Size

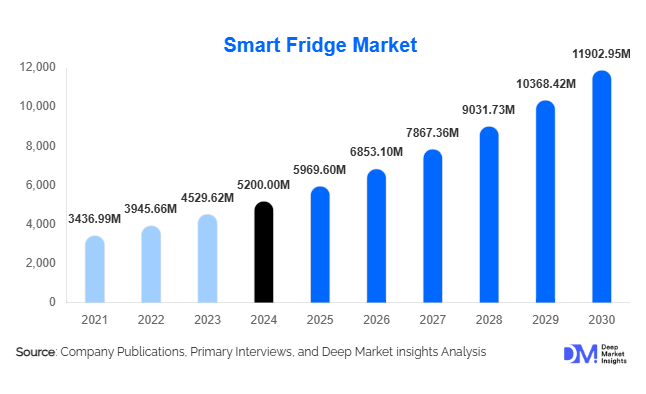

According to Deep Market Insights, the global smart fridge market size was valued at USD 5,200 million in 2025 and is projected to grow from USD 5969.60 million in 2026 to reach USD 11902.95 million by 2031, expanding at a CAGR of 14.8% during the forecast period (2026–2031). The smart fridge market growth is primarily driven by the increasing integration of IoT and AI technologies in home appliances, rising demand for energy-efficient connected devices, and the expansion of smart home ecosystems across global urban centers.

Key Market Insights

- IoT-enabled home appliances are becoming mainstream, with smart fridges leading the adoption curve due to their multifunctional capabilities, including inventory management, voice assistance, and remote monitoring.

- AI-powered food management and predictive maintenance are key differentiators driving consumer upgrades from conventional refrigerators.

- North America dominates the global market, supported by high smart home penetration and strong demand for premium appliances.

- Asia-Pacific is the fastest-growing region, propelled by expanding middle-class households, rapid urbanization, and government initiatives promoting energy-efficient appliances.

- Energy efficiency regulations and sustainability standards are encouraging manufacturers to develop eco-friendly, low-power smart refrigerators.

- Integration with digital assistants and home ecosystems such as Alexa, Google Assistant, and Samsung SmartThings is transforming user convenience and connectivity.

Smart Fridge Market Trends

AI and Machine Learning Integration

Smart fridges are increasingly equipped with AI-based systems capable of analyzing user behavior and optimizing food storage conditions. Advanced models now feature automatic inventory tracking through internal cameras and sensors, alerting users about expiring items and suggesting recipes based on available ingredients. Machine learning algorithms also enable predictive maintenance, reducing downtime and extending appliance lifespan. These innovations reflect a broader consumer shift toward intelligent, self-regulating kitchen appliances that enhance both convenience and sustainability.

Energy Efficiency and Sustainability Focus

Growing environmental awareness and stricter energy regulations are accelerating the adoption of energy-efficient smart fridges. Manufacturers are incorporating inverter compressors, smart temperature controls, and eco-modes to minimize power consumption. Additionally, many brands are utilizing recyclable materials and natural refrigerants to reduce carbon emissions. Integration with smart grids and renewable power sources is also gaining traction, allowing consumers to manage energy use more effectively and align with global sustainability goals.

Smart Fridge Market Drivers

Rising Smart Home Penetration

The rapid expansion of smart home infrastructure is a major driver for smart fridge adoption. As consumers embrace IoT-enabled ecosystems, demand for interconnected appliances that provide convenience, automation, and energy management continues to surge. The integration of smart fridges with home assistants, mobile applications, and voice command systems enhances household efficiency, appealing to tech-savvy and time-conscious users globally.

Consumer Preference for Health and Convenience

Health-conscious consumers are increasingly adopting smart fridges for features such as real-time food freshness monitoring, dietary tracking, and automated grocery list generation. These appliances help users reduce food waste while promoting healthier eating habits. Integration with nutrition apps and digital assistants further supports lifestyle management, positioning smart fridges as central components of modern connected kitchens.

Smart Fridge Market Restraints

High Cost of Smart Appliances

Smart fridges remain significantly more expensive than conventional models due to advanced sensors, connectivity modules, and AI integration. This cost factor limits adoption in price-sensitive markets, particularly in developing economies. Although long-term energy savings partially offset initial expenses, affordability continues to be a barrier to mass-market penetration.

Cybersecurity and Privacy Concerns

As connected appliances gather and transmit data, cybersecurity threats pose a growing challenge. Unauthorized access to personal information or home networks through IoT vulnerabilities can undermine consumer trust. Manufacturers are addressing this by implementing encrypted communication protocols and AI-driven threat detection systems, but widespread apprehension about data privacy remains a restraint on market growth.

Smart Fridge Market Opportunities

Expansion of Connected Kitchen Ecosystems

The rise of fully integrated smart kitchens presents major growth opportunities. Smart fridges can act as central hubs, connecting with ovens, microwaves, and grocery delivery apps to automate meal planning and preparation. Partnerships between appliance manufacturers and tech companies such as Samsung, LG, and Google are expanding interoperability, paving the way for holistic smart living solutions.

Subscription-Based and Aftermarket Services

Smart fridges are increasingly enabling new business models through data-driven services, such as automatic grocery replenishment, predictive maintenance subscriptions, and recipe recommendations. This recurring revenue potential attracts both appliance makers and retailers, creating new monetization opportunities and fostering long-term customer engagement.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5200 Million |

| Market Size in 2026 | USD 5969.60 Million |

| Market Size in 2031 | USD 11902.95 Million |

| CAGR | 14.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

French-door smart fridges continue to dominate the market due to their advanced connectivity features, large storage capacity, and seamless integration with home automation systems, which appeals to premium consumers seeking turnkey solutions. Side-by-side and bottom-freezer models remain popular among mid-range buyers, balancing affordability with smart functionality. Compact and mini smart fridges are gaining traction among urban dwellers and small households, particularly in Asia-Pacific and Europe, where space optimization and multifunctionality are critical. Manufacturers are also expanding modular and customizable smart fridge designs, allowing users to personalize storage compartments, display interfaces, and connectivity levels, which is driving enhanced user experience and adoption. Retrofit smart modules, which upgrade existing appliances, are also seeing increased demand, acting as an affordability driver for households unwilling to invest in a full smart refrigerator.

Application Insights

Residential applications account for the majority of smart fridge deployments, fueled by the growing smart home trend, demand for convenience, and sustainability-conscious consumer behavior. Advanced AI-enabled fridges with inventory tracking, expiry alerts, and recipe suggestions provide significant value for households, particularly in North America and Europe. Commercial applications, including hotels, restaurants, and corporate cafeterias, are expanding as businesses seek operational efficiency, food safety compliance, and integration with kitchen management systems. Hospitality sectors are also investing in smart mini-bars and beverage fridges to enhance service personalization, reduce food wastage, and improve guest experience. Institutional use, such as hospitals and educational facilities, is gradually increasing, driven by the need for precise temperature control for food and medical storage.

Distribution Channel Insights

Online retail platforms dominate smart fridge sales, providing transparent pricing, product comparison, and home delivery services, which accelerate adoption across urban and semi-urban markets. E-commerce giants like Amazon, Alibaba, and local marketplaces are particularly influential in Asia-Pacific and Latin America. Offline channels, including brand-exclusive stores and consumer electronics chains, remain important for high-value purchases that require in-person consultation and demonstration. Direct-to-consumer (D2C) models, increasingly adopted by major brands, enable better control over the software ecosystem, subscription services, and customer loyalty programs. B2B contracts, targeting hotels, cloud kitchens, and commercial kitchens, provide stable, bulk orders for smart refrigerators with specialized features. Aftermarket upgrades and retrofit modules are also expanding the installed base, particularly in mid-range and developing markets.

End-User Insights

Residential households remain the primary end-user segment, motivated by convenience, connected kitchen ecosystems, and energy-efficient operations. Foodservice and commercial buyers, including restaurants, hotels, and catering services, are increasingly adopting smart refrigerators for inventory management, operational efficiency, and compliance with food safety regulations. Institutional buyers such as hospitals, schools, and universities are integrating smart fridges for precise temperature control in food and medical storage applications, expanding the commercial scope of the market. The premium residential and commercial segments are driving early adoption, while mid-range and economy segments continue to grow as affordability improves through financing and retrofit solutions.

Explore more data points, trends and opportunities Download Free Sample Report

Smart Fridge Market Segmentations

By Product Type

- French-Door Smart Refrigerators

- Side-by-Side Smart Refrigerators

- Bottom-Freezer Smart Refrigerators

- Compact & Mini Smart Refrigerators

- Modular and Customizable Smart Refrigerators

By Application

- Residential

- Commercial (Hotels, Restaurants, Cafeterias)

- Institutional (Hospitals, Educational Facilities)

- Retail and Foodservice

By Distribution Channel

- Online Retail

- Brand-Owned E-Commerce Platforms

- Electronics & Appliance Stores

- Department Stores

- Direct-to-Consumer (D2C) Sales

By Connectivity Technology

- Wi-Fi Enabled Smart Refrigerators

- Bluetooth & NFC Connected Models

- AI and Voice Assistant Integrated Refrigerators

- Smart Grid & Energy Monitoring Refrigerators

By End User

- Individual Households

- Commercial Enterprises

- Institutional Buyers

Regional Insights

North America

North America leads the global smart fridge market, driven by high smart-home penetration and robust voice-assistant ecosystems such as Alexa and Google Assistant, which facilitate easy appliance integration. The U.S. dominates regional demand, supported by large retail and e-commerce channels, appliance financing options, and high disposable incomes that reduce upfront cost barriers. Demand is also fueled by advanced AI features and predictive inventory management, which appeal to tech-savvy consumers. Canada is emerging as a strong secondary market, driven by urban apartment living and the increasing adoption of energy-efficient appliances. Key players such as Whirlpool, GE Appliances, and Samsung Electronics continue to innovate with enhanced energy ratings and smart ecosystem integration.

Europe

Europe’s smart fridge market growth is supported by strict energy-efficiency regulations, eco-design standards, and sustainability-conscious consumers, which favor energy-saving and certified smart fridges. Countries such as Germany, the U.K., and France are leading adopters due to high urban apartment density, increasing demand for space-optimizing, multifunctional refrigerators, and advanced connectivity features. Additional drivers include government incentives for energy-efficient appliances and a well-established retail network, enabling both premium and mid-range adoption. Consumers in Europe also increasingly seek appliances integrated with AI, voice assistants, and cloud-enabled features.

Asia-Pacific

Asia-Pacific is the fastest-growing smart fridge market, fueled by rapid urbanization, a rising middle class, and increasing disposable incomes. Domestic manufacturers like Haier, Hisense, and Midea are driving adoption through low-cost production and regional electronics ecosystem support, enabling competitive pricing for both premium and mid-range models. High-density urban centers in China, India, and Indonesia are creating strong demand for compact, modular, and multifunctional smart fridges, while e-commerce expansion further accelerates accessibility. Partnerships with global tech firms are helping integrate cloud features, AI, and IoT connectivity, making smart fridges a central component of modern connected kitchens in the region.

Latin America

Latin America is experiencing steady growth, led by Brazil and Mexico, with urbanization, growing e-commerce, and appliance financing driving smart fridge adoption. Mid-range and value-oriented smart fridges are gaining popularity as they balance affordability with essential smart features such as inventory alerts, Wi-Fi connectivity, and temperature optimization. Online retail channels play a key role in boosting awareness and accessibility, while increasing consumer preference for convenience, energy efficiency, and connectivity is pushing adoption in both residential and commercial sectors.

Middle East & Africa

The Middle East is emerging as a promising market for premium and connected smart appliances, with high-income urban centers in the UAE, Saudi Arabia, and Qatar driving demand. The hospitality sector, including hotels and resorts, acts as an early adopter of smart refrigerators with advanced features like AI inventory and energy-management systems. In Africa, adoption remains nascent but is expected to accelerate due to improving electricity access, urbanization, and expanding middle-class populations. Smart fridges with energy backup and power optimization features are particularly attractive in regions with intermittent electricity supply, combining convenience with reliability.

Key Players in the Smart Fridge Market

- Samsung Electronics Co., Ltd.

- LG Electronics Inc.

- Haier Group Corporation

- Whirlpool Corporation

- Electrolux AB

- Hisense Group

- Panasonic Corporation

- BSH Home Appliances Group

Recent Developments

- In August 2025, LG Electronics launched its new “MoodUP” refrigerator featuring color-changing LED panels and AI freshness monitoring, enhancing personalization and visual appeal.

- In June 2025, Samsung introduced AI-powered SmartThings integration across its Bespoke fridge lineup, enabling seamless interoperability with other connected kitchen appliances.

- In March 2025, Whirlpool Corporation announced its partnership with Amazon for in-fridge grocery replenishment, integrating automatic ordering for frequently purchased items.