Smart Faucets Market Size

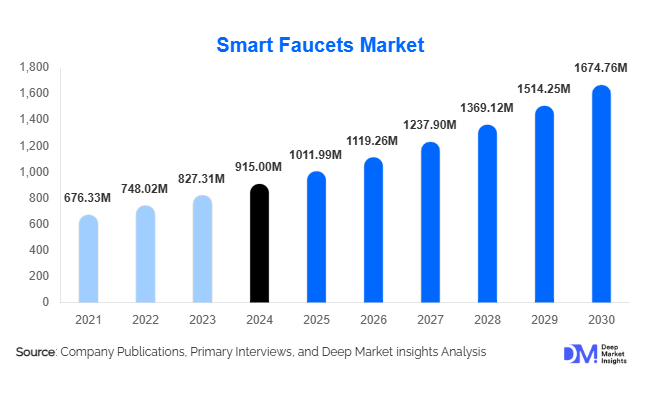

According to Deep Market Insights, the global smart faucets market size was valued at USD 915.00 million in 2025 and is projected to grow from USD 1,011.99 million in 2026 to reach USD 1,674.76 million by 2031, expanding at a CAGR of 10.6% during the forecast period (2026–2031). The smart faucets market growth is primarily driven by rising hygiene awareness, increasing adoption of water-efficient plumbing solutions, rapid penetration of smart homes and buildings, and government-led initiatives promoting sustainable water management across residential and commercial infrastructure.

Key Market Insights

- Touchless smart faucets dominate global demand due to heightened hygiene standards in healthcare, hospitality, and public infrastructure.

- Commercial applications account for the largest revenue share, supported by mandatory sensor-based installations in public and institutional buildings.

- North America leads the global market, driven by strong smart home adoption and premium housing developments.

- Asia-Pacific is the fastest-growing region, fueled by urbanization, smart city projects, and water scarcity concerns.

- Wi-Fi and IoT integration is becoming a key differentiator, enabling real-time monitoring and smart home ecosystem compatibility.

- Mid-range smart faucets are gaining maximum traction by balancing affordability and advanced functionality.

Smart Faucets Market Trends

Touchless and Hygiene-Focused Adoption Accelerating

Smart faucets with infrared and motion-sensing technologies are witnessing rapid adoption as hygiene becomes a core design requirement rather than a premium feature. Commercial buildings, hospitals, airports, and educational institutions are mandating touchless fixtures to reduce cross-contamination risks. This trend is also extending into residential bathrooms and kitchens, where consumers increasingly prioritize cleanliness, convenience, and modern aesthetics. Manufacturers are improving sensor accuracy, response time, and durability to cater to high-traffic environments, making touchless smart faucets the fastest-adopted product category globally.

Integration with Smart Home and IoT Ecosystems

Smart faucets are increasingly being integrated into broader smart home platforms, enabling voice control, app-based customization, and real-time water usage analytics. Compatibility with voice assistants and centralized home automation systems is enhancing consumer appeal, particularly among tech-savvy urban households. Advanced models now offer features such as leak detection, temperature presets, and usage tracking, supporting both sustainability goals and premium pricing strategies. This trend is strengthening the transition of smart faucets from standalone fixtures to connected home infrastructure components.

Smart Faucets Market Drivers

Growing Focus on Water Conservation and Sustainability

Global water scarcity and sustainability mandates are major growth drivers for the smart faucets market. Smart faucets can reduce water consumption by 30–50% through precise flow control, automatic shut-off, and usage monitoring. Governments and green building certification bodies are encouraging or mandating water-efficient fixtures in new construction and renovation projects. As sustainability becomes a priority for both policymakers and consumers, smart faucets are emerging as essential solutions for long-term water management.

Expansion of Smart Buildings and Urban Infrastructure

The rapid expansion of smart cities, commercial complexes, and high-end residential developments is accelerating demand for intelligent plumbing solutions. Real estate developers increasingly position smart faucets as value-enhancing features that improve building efficiency, hygiene, and user experience. Growth in urban housing, mixed-use developments, and premium office spaces is directly translating into higher adoption rates for smart faucets globally.

Smart Faucets Market Restraints

High Initial Costs and Price Sensitivity

Smart faucets are priced significantly higher than conventional faucets, which can limit adoption in cost-sensitive markets and low-income housing segments. Although long-term water and energy savings offset initial investments, upfront affordability remains a challenge, particularly in emerging economies. Price sensitivity continues to restrain large-scale penetration in budget residential projects.

Installation and Maintenance Complexity

Advanced smart faucets require a stable power supply, reliable connectivity, and technical expertise for installation and maintenance. In regions with underdeveloped infrastructure or limited technical support, these complexities can deter adoption. Maintenance costs and sensor calibration issues in high-usage environments also present operational challenges for end users.

Smart Faucets Market Opportunities

Government-Led Water Efficiency Programs

Government initiatives promoting water conservation present significant growth opportunities. Public infrastructure upgrades, smart city projects, and sustainability-focused housing programs are creating long-term demand for smart faucets. Regions facing water stress are increasingly incorporating sensor-based fixtures into building codes, offering manufacturers stable, large-volume procurement opportunities.

Growth in Healthcare and Hospitality Infrastructure

Rising investments in hospitals, clinics, hotels, and airports—particularly in Asia-Pacific and the Middle East—are creating strong demand for hygienic, touchless plumbing solutions. Smart faucets are becoming standard installations in new healthcare and hospitality projects, offering suppliers opportunities for long-term institutional contracts and repeat orders.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 915 Million |

| Market Size in 2026 | USD 1011.99 Million |

| Market Size in 2031 | USD 1674.76 Million |

| CAGR | 10.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Touchless smart faucets dominate the market, accounting for approximately 46% of global revenue in 2025, driven by hygiene regulations and high commercial adoption. Touch-activated faucets hold a significant share in residential kitchens, while voice-controlled and app-enabled faucets are emerging in premium housing. IoT-integrated models are gaining momentum as smart home adoption accelerates, particularly in North America and Europe.

Installation Type Insights

Deck-mounted smart faucets lead the market with nearly 62% share, favored for ease of installation and retrofitting in existing buildings. Wall-mounted faucets are primarily used in commercial and healthcare settings where space optimization and hygiene standards are critical.

End-Use Insights

The commercial segment accounts for approximately 58% of the global smart faucets market in 2025, driven by healthcare, hospitality, offices, and public restrooms. Residential demand is growing faster, supported by smart home adoption and premium housing projects, and is expected to gain share through 2031.

Distribution Channel Insights

Direct sales dominate large-scale commercial and infrastructure projects, accounting for about 44% of market revenue. Specialty plumbing retailers remain important for residential buyers, while online and e-commerce channels are expanding rapidly due to increased digital purchasing and product comparison behavior.

Explore more data points, trends and opportunities Download Free Sample Report

Smart Faucets Market Segmentations

By Product Type

- Touchless / Sensor-Based Smart Faucets

- Touch-Activated Smart Faucets

- Voice-Controlled Smart Faucets

- App-Enabled / IoT-Integrated Smart Faucets

By Installation Type

- Deck-Mounted Smart Faucets

- Wall-Mounted Smart Faucets

By Connectivity Type

- Bluetooth-Enabled Smart Faucets

- Wi-Fi-Enabled Smart Faucets

- Hybrid Connectivity

By Power Source

- Battery-Operated Smart Faucets

- Hardwired / AC-Powered Smart Faucets

- Hybrid Power

By Distribution Channel

- Direct Sales / Institutional Projects

- Specialty Plumbing & Sanitary Retail

- Online / E-Commerce Channels

Regional Insights

North America

North America accounts for approximately 32% of the global smart faucets market in 2025, led by the United States. Strong smart home adoption, stringent hygiene standards, and high disposable incomes are key demand drivers. The U.S. alone contributes nearly 26% of global revenue.

Europe

Europe holds around 28% market share, supported by sustainability regulations and green building mandates. Germany, the U.K., and France are major contributors, with strong adoption in commercial and residential renovation projects.

Asia-Pacific

Asia-Pacific represents about 25% of the market and is the fastest-growing region, with a CAGR exceeding 17%. China, Japan, South Korea, and India are key markets, driven by urbanization, smart city initiatives, and water conservation needs.

Latin America

Latin America accounts for nearly 7% of global demand, with Brazil and Mexico leading adoption in commercial buildings and premium residential projects.

Middle East & Africa

This region holds around 8% market share, driven by hospitality infrastructure, luxury real estate, and acute water scarcity concerns in countries such as the UAE and Saudi Arabia.

Key Players in the Smart Faucets Market

- Moen Incorporated

- Kohler Co.

- LIXIL Group

- TOTO Ltd.

- Delta Faucet Company

- Hansgrohe Group

- Grohe AG

- American Standard Brands

- Roca Group

- Jaquar Group

- Villeroy & Boch

- Sloan Valve Company

- Oras Group

- Pfister

- Brizo