Smart Diapers Market Size

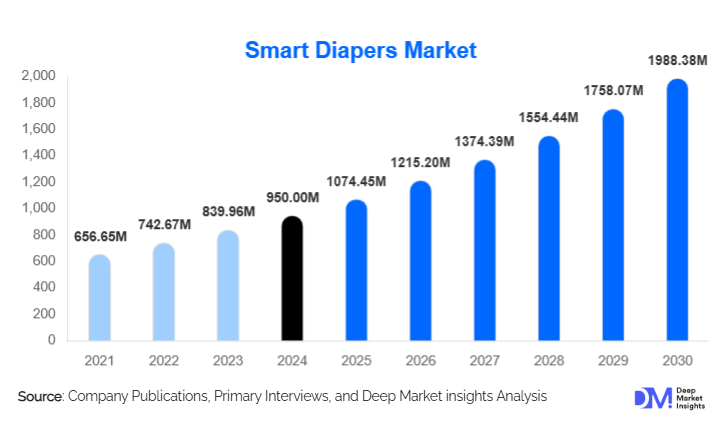

According to Deep Market Insights, the global smart diapers market was valued at USD 950 million in 2025 and is projected to grow from USD 1074.45 million in 2026 to USD 1988.38 million by 2031, expanding at a CAGR of 13.1% (2026–2031). This robust growth is driven by rising parental inclination towards digital parenting tools, increased focus on infant health monitoring, and the growing integration of wearable sensor technologies in consumer hygiene products. The market is further supported by expanding birth rates in Asia Pacific and the increasing geriatric population in North America and Europe, who require continuous monitoring for incontinence management and urinary health. The emergence of AI-powered diaper platforms capable of analyzing hydration, pH levels, and early signs of skin irritation is transforming smart diapers from basic notification tools into proactive healthcare solutions. Additionally, favorable insurance policies for reimbursable elderly care products and growing adoption across hospitals and assisted living facilities are accelerating institutional demand.

Smart diapers are made using conventional absorbent layers combined with embedded moisture, temperature, pH, or pressure sensors that detect wetness or potential skin risk conditions. These diapers connect via Bluetooth or Wi-Fi to smartphones or caregiver monitoring systems, providing real-time alerts, analyzable data logs, and diaper change histories. Prominent brands such as Procter & Gamble, Kimberly-Clark, Essity AB, Ontex, Monit Corp., and Simavita are investing in smart diaper platforms that combine sensor-equipped diapers, wearable patches, and mobile apps offering predictive analytics and remote monitoring. Leading companies are focusing on developing washable, detachable sensors, reusable wireless strips, eco-friendly materials, and AI-enabled digital dashboards to enhance user experience, reduce waste, and improve cost-effectiveness for both households and healthcare providers.

Smart Diapers Market Trends

- AI-driven predictive diaper monitoring: Increasing integration of AI-based algorithms allows smart diapers to analyze moisture levels, usage patterns, and urinary biomarkers to predict skin irritation, dehydration, or infection risks. These AI tools generate care recommendations for caregivers and healthcare providers.

- Geriatric care digitalization: Long-term care facilities are integrating smart diaper dashboards that monitor multiple patients, detect delayed changes, and alert caregivers to prevent pressure ulcers and diaper rash. This is reducing labor strain and improving hygiene outcomes.

- Bluetooth and NFC-based sensor integration: Advanced BLE and NFC sensors are making diapers more responsive, battery-efficient, and capable of complex data transmission without discomfort to the wearer. These lightweight sensors are increasingly being used in both baby and adult smart diapers.

- Sustainability and reusable sensors: Manufacturers are introducing eco-friendly versions with biodegradable diaper layers and detachable, waterproof, reusable sensors. These hybrid models reduce waste and lower long-term cost for institutional buyers.

- Consumer-focused subscription platforms: Smart diaper companies are launching digital care ecosystems offering monthly diaper delivery, mobile health tracking, diaper usage analytics, and expert consultation services for parents and caregivers.

- Healthcare system integration: Hospitals and assisted living centers are using smart diaper monitoring to improve patient comfort, reduce manual monitoring time, and maintain digital hygiene records that aid in clinical care decisions.

- Partnerships with telehealth providers: Telehealth collaborations are enabling real-time sharing of diaper monitoring data with pediatricians and geriatric care specialists, allowing early detection of health risks from remote locations.

Smart Diapers Market Opportunities

The global smart diapers market growth is supported by advances in IoT-enabled hygiene solutions, growing awareness of diaper-associated dermatitis prevention, and increasing demand from pediatric and geriatric care segments. A significant growth opportunity lies in the integration of urinary biomarker monitoring technology. Smart diapers equipped with pH, ketone, and protein-detecting sensors are being developed to detect early signs of urinary tract infections, dehydration, and metabolic disorders. This opens new use cases in pediatric hospitals, neonatal intensive care units (NICUs), and care facilities for patients with chronic incontinence conditions.

Another promising area is the adoption of cloud-connected platforms in elderly long-term care management. Institutional smart diapers paired with wearable health trackers and automated alert systems allow caregivers to monitor multiple patients simultaneously, reducing manual checks, improving hygiene efficiency, and preventing bed sores. Research and development opportunities also exist in designing waterproof, flexible sensors suitable for multiple wash cycles, reducing costs and achieving a more sustainable product line. Additionally, healthcare partnerships for reimbursement-based eldercare smart diaper programs are gaining traction in the U.S., Germany, Japan, and South Korea.

Direct-to-consumer subscription models that combine smart diapers with mobile health apps, diaper usage forecasting, refill reminders, and pediatric nutrition tips are also emerging as high-margin opportunities. These platforms track diaper usage patterns, sleeping schedules, and hydration levels to offer personalized care recommendations, increasing consumer engagement and brand loyalty.

Smart diapers encompass disposable or reusable absorbent hygiene products fitted with detachable sensors and wireless communication modules. They serve both consumer and institutional purposes, supporting infant wellness tracking, elderly incontinence management, and remote health monitoring. These products help reduce overuse of diapers, prevent skin irritation, and enable timely medical intervention through digital analytics.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 950 Million |

| Market Size in 2026 | USD 1074.45 Million |

| Market Size in 2031 | USD 1988.38 Million |

| CAGR | 13.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Insights

By Product Type

Based on product type, the market is segmented into baby smart diapers, adult smart diapers, and sensor-based add-on devices.

- Baby smart diapers: This segment leads due to rising adoption of smart parenting technologies, increased childcare spending, and rising digital penetration in emerging markets. They are equipped with moisture, temperature, and rash prediction sensors and linked to mobile parenting apps.

- Adult smart diapers: This segment is rapidly growing due to geriatric population increase, higher prevalence of incontinence, and rising demand from hospitals and assisted living facilities for remote hygiene monitoring solutions.

- Sensor-based add-ons: Includes detachable, reusable patches and wireless sensor strips that can be used with conventional diaper products. These are popular for institutional usage due to lower cost and compatibility with multiple diaper formats.

By Technology

Based on technology, the market is segmented into RFID, Bluetooth Low Energy (BLE), and wearable sensors.

- RFID: Primarily used in hospitals and clinical settings for hygiene tracking, diaper change documentation, and health record integration.

- Bluetooth Low Energy (BLE): Most widely adopted in consumer smart diapers due to mobile connectivity, long battery life, and low energy consumption.

- Wearable sensors: Offer advanced features such as pH-level tracking, biometric analysis, and predictive rash assessment, providing enhanced functionality for pediatric and geriatric applications.

By Distribution Channel

Based on distribution channel, the market is segmented into supermarkets & hypermarkets, pharmacies, online retail, and institutional supply.

- Supermarkets & hypermarkets: Most common retail channel, offering branded smart diapers bundled with refills, sensor kits, and promotional offers.

- Pharmacies: Preferred for adult smart diaper purchases, especially for medically approved or insurance-reimbursable products.

- Online retail: Fastest-growing channel, driven by app-based subscription orders, home delivery, and bundled digital monitoring services.

- Institutional supply: Includes hospitals, nursing homes, and healthcare groups procuring smart diaper systems in volume for patient monitoring and hygiene management.

By End Use

Based on end use, the market is segmented into homecare, hospitals, and long-term care facilities.

- Homecare: Dominant segment due to widespread usage among households managing babies, young children, and elderly individuals with incontinence.

- Hospitals: Preferred for neonatal monitoring, surgery recovery support, and patient hydration tracking.

- Long-term care facilities: Increasing adoption of smart diaper systems with centralized monitoring dashboards for efficient patient care.

Explore more data points, trends and opportunities Download Free Sample Report

Smart Diapers Market Segmentations

By Product Type

- Baby Smart Diapers

- Adult Smart Diapers

- Sensor-Based Add-On Devices

By Technology

- RFID

- Bluetooth Low Energy (BLE)

- Wearable Sensors

By Distribution Channel

- Supermarkets & Hypermarkets

- Pharmacies

- Online Retail

- Institutional Supply

By End Use

- Homecare

- Hospitals

- Long-Term Care Facilities

Regional Insights

North America accounted for 35.6% of the global smart diapers market in 2025.

- The U.S. leads the region due to high device connectivity, strong healthcare infrastructure, and broad insurance coverage for smart eldercare products. Advanced pediatric and geriatric hospitals are integrating cloud-based diaper monitoring systems.

- Canada shows growing demand for digital caregiving tools, especially for elderly incontinence monitoring, supported by government initiatives in remote healthcare.

Europe smart diapers market was valued at USD 410 million in 2025 and is expected to record strong growth through 2031.

- High elderly population, strict hygiene regulations, and government focus on digital nursing tools are optimizing adoption in hospitals and care centers across Germany, France, and the UK.

- Increasing collaboration between diaper manufacturers, health tech companies, and telehealth providers is driving product innovation and distribution.

Asia Pacific region is among the fastest-growing smart diapers markets globally.

- China, Japan, and South Korea lead the region, with strong manufacturing infrastructure, advanced consumer technology adoption, and rapidly expanding eldercare networks.

- India and Southeast Asia show rising adoption in urban areas driven by higher birth rates, expanding online retail, and greater awareness of hygiene and infant health monitoring.

Japan is experiencing high demand for smart adult diapers due to a rapidly aging population.

- Government-backed healthcare digitization initiatives and hospital digital automation are boosting usage in geriatric and surgical recovery applications.

Brazil and Saudi Arabia are emerging markets with increasing focus on digital health integration in care management.

- Adoption is driven by growing healthcare investments, urbanization, and rising awareness of digital hygiene solutions for infants and elderly.

Smart Diapers Market Share

- The top 5 players, Procter & Gamble, Kimberly-Clark, Ontex, Essity AB, and Simavita, collectively accounted for approximately 48% of global smart diapers revenue in 2025, with the remainder captured by emerging tech startups and regional diaper manufacturers.

- Leading companies are focusing on AI-integrated sensor platforms, digital-care subscription services, and cross-industry collaborations with telehealth providers to enhance market penetration.

- Emerging players are capitalizing on niche opportunities such as eco-friendly smart diapers, reusable sensor systems, and localized baby care apps.

- Institutional demand is driving partnerships between diaper manufacturers and hospital procurement networks to supply IoT-enabled hygiene monitoring systems.

Smart Diapers Market Companies

Few of the prominent players operating in the smart diapers market include:

- Procter & Gamble

- Kimberly-Clark Corporation

- Essity AB

- Ontex Group

- Simavita

- Monit Corp.

- Abena Healthcare

- Hengan Group

- Unicharm Corporation

- Wonderkin Co. Ltd.

- Kao Corporation

- Tytex A/S

- Nobel Hygiene

- Verily Life Sciences

- Dyper Inc.

- Procter & Gamble focuses on expanding its smart baby diaper segment with mobile app integration, predictive moisture alerts, and personalized digital parenting support, targeting premium household customers globally.

- Kimberly-Clark Corporation offers advanced smart adult diapers equipped with wireless health monitoring systems for hospitals and eldercare facilities, focusing on large-scale institutional distribution.

- Simavita specializes in clinical incontinence monitoring solutions using wearable sensors and cloud-based reporting platforms for hospitals and assisted living care units.