Slow Cooker Market Size

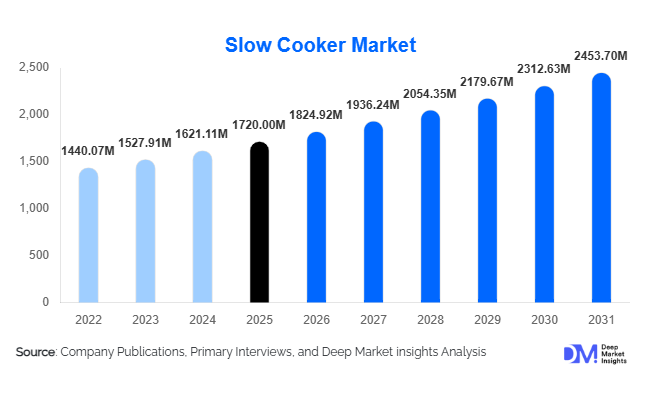

According to Deep Market Insights, the global slow cooker market size was valued at USD 1,720 million in 2025 and is projected to grow from USD 1,824.92 million in 2026 to reach USD 2,453.70 million by 2031, expanding at a CAGR of 6.1% during the forecast period (2026–2031). The slow cooker market growth is primarily driven by increasing demand for convenient cooking appliances, rising adoption of home-cooked meals, and growing consumer preference for energy-efficient kitchen solutions. The integration of smart technologies and multifunctional capabilities is further supporting market expansion globally.

Key Market Insights

- Demand for convenience cooking appliances is rising globally, driven by busy lifestyles and increasing dual-income households.

- Programmable and smart slow cookers are gaining traction, enhancing user control and automation in cooking processes.

- North America dominates the global market due to high product penetration and strong consumer awareness.

- Asia-Pacific is the fastest-growing region, supported by rising disposable incomes and urbanisation.

- Mid-range products lead the market, offering a balance between affordability and advanced features.

- E-commerce channels are rapidly expanding, transforming purchasing behaviour and improving product accessibility.

What are the latest trends in the slow cooker market?

Smart and Connected Cooking Appliances

The adoption of IoT-enabled slow cookers is transforming the market landscape. Consumers increasingly prefer appliances that can be controlled remotely via smartphones or integrated with voice assistants. Features such as real-time monitoring, programmable cooking cycles, and app-based notifications are enhancing user convenience. Manufacturers are focusing on smart ecosystem integration, allowing slow cookers to be part of broader connected kitchens. This trend is particularly strong in developed markets, where smart home adoption is accelerating, enabling premium product penetration and higher margins.

Shift Toward Multi-functional Kitchen Appliances

Consumers are increasingly opting for appliances that combine multiple cooking functions. Slow cookers integrated with pressure cooking, steaming, sautéing, and even air frying capabilities are gaining popularity. This shift is driven by the need to optimise kitchen space and enhance value for money. Manufacturers are innovating hybrid products to cater to evolving consumer preferences, especially in urban households where compact, versatile appliances are highly valued. This trend is also contributing to higher replacement rates as consumers upgrade from basic models to advanced multifunctional devices.

What are the key drivers in the slow cooker market?

Rising Demand for Convenience and Time-Saving Solutions

Modern lifestyles, characterised by long working hours and busy schedules, have increased the demand for appliances that simplify cooking. Slow cookers allow users to prepare meals with minimal supervision, making them ideal for working professionals and families. This convenience factor remains one of the strongest drivers for market growth.

Growing Popularity of Home Cooking

The global shift toward home cooking, accelerated by pandemic-driven behavioural changes, continues to influence demand. Consumers are experimenting with diverse cuisines, including slow-cooked recipes, boosting the adoption of slow cookers. This trend is further supported by the availability of online recipes and cooking tutorials.

Energy Efficiency and Cost Savings

Slow cookers consume less electricity compared to conventional cooking appliances such as ovens. With rising energy costs worldwide, consumers are increasingly prioritising energy-efficient appliances. This advantage is particularly relevant in regions with high electricity prices, supporting steady demand growth.

What are the restraints for the global market?

Competition from Multi-Cookers and Advanced Appliances

The availability of multifunctional appliances such as Instant Pots and multicookers poses a significant challenge. These appliances offer broader functionality, including pressure cooking and faster cooking times, which may limit the adoption of standalone slow cookers.

Perception of Long Cooking Times

Slow cookers are often perceived as time-consuming due to extended cooking durations. This perception can deter consumers seeking quick meal preparation solutions, particularly in fast-paced urban environments. Overcoming this perception remains a key challenge for manufacturers.

What are the key opportunities in the slow cooker industry?

Expansion in Emerging Markets

Emerging economies in the Asia-Pacific and Latin America present significant growth opportunities. Rising disposable incomes, urbanisation, and increasing exposure to global cuisines are driving demand for modern kitchen appliances. Localisation strategies, such as designing products suited to regional cooking styles, can further accelerate adoption.

Integration with Smart Home Ecosystems

The growing adoption of smart homes offers a lucrative opportunity for manufacturers to introduce connected slow cookers. Integration with voice assistants and mobile apps enhances convenience and attracts tech-savvy consumers. This trend is expected to drive premium segment growth.

Product Innovation and Premiumization

Continuous innovation in design, functionality, and materials is creating opportunities for premium product offerings. Features such as touchscreen controls, advanced safety mechanisms, and multi-functionality are enabling manufacturers to differentiate their products and capture higher-value segments.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1720 Million |

| Market Size in 2026 | USD 1824.92 Million |

| Market Size in 2031 | USD 2453.70 Million |

| CAGR | 6.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Programmable slow cookers dominate the global market, accounting for approximately 45% of the total share in 2025, driven primarily by increasing consumer preference for convenience, automation, and precision cooking. These models offer advanced features such as digital timers, preset cooking modes, delayed start functions, and automatic temperature adjustments, making them highly attractive to modern households with busy lifestyles. The shift from manual to programmable appliances has been particularly strong in developed markets, where consumers prioritise time efficiency and ease of use.

Manual slow cookers continue to maintain steady demand, especially in price-sensitive and emerging markets, due to their affordability, durability, and simple operation. These products are widely adopted in regions where consumers prioritise cost over advanced features. Meanwhile, smart slow cookers are the fastest-growing sub-segment, supported by the rapid adoption of connected home ecosystems and IoT-enabled appliances. Integration with mobile applications and voice assistants is enabling remote monitoring and control, positioning this segment as a key growth driver in the premium category over the forecast period.

Application Insights

The residential segment dominates the slow cooker market, accounting for nearly 78% of total demand in 2025, primarily driven by increasing household adoption and the global shift toward home-cooked meals. Changing lifestyles, rising health consciousness, and growing interest in convenient cooking methods are reinforcing demand across urban households. The trend of meal prepping and batch cooking has further strengthened the relevance of slow cookers in residential kitchens.

The commercial segment, although smaller, is witnessing steady growth, supported by the expansion of the global foodservice industry and increasing demand for cost-efficient cooking solutions. Restaurants, catering services, and institutional kitchens are utilising slow cookers for bulk preparation of soups, stews, and slow-cooked dishes. Additionally, emerging applications such as cloud kitchens, meal-prep services, and delivery-focused food businesses are creating incremental demand. These operators benefit from the low energy consumption and minimal supervision requirements of slow cookers, making them suitable for scalable food production models.

Distribution Channel Insights

Offline retail channels continue to dominate the market with approximately 60% share in 2025, as consumers prefer physical inspection of appliances before purchase. Supermarkets, hypermarkets, and specialty appliance stores play a crucial role in influencing buying decisions through product demonstrations and in-store promotions. This channel remains particularly strong in developing markets where digital penetration is still evolving.

However, online retail is the fastest-growing distribution channel, driven by the rapid expansion of e-commerce platforms, increasing internet penetration, and changing consumer purchasing behaviour. Competitive pricing, wider product selection, customer reviews, and convenience are key factors accelerating online sales. Brand-owned websites and global marketplaces are gaining traction, especially in emerging markets, where consumers are increasingly relying on digital platforms for appliance purchases. The online segment is expected to significantly increase its share by 2031, reshaping the overall distribution landscape.

Price Range Insights

Mid-range slow cookers lead the market, accounting for approximately 52% of global share in 2025, as they offer an optimal balance between affordability and advanced functionality. These products typically include programmable features and improved build quality, making them highly appealing to a broad consumer base across both developed and developing regions.

Economy models cater primarily to price-sensitive consumers in emerging markets, where affordability remains a key purchasing criterion. These products are characterised by basic functionality and durable design. On the other hand, premium slow cookers are gaining traction among high-income consumers, particularly in North America and Europe, driven by demand for smart features, multi-functionality, and aesthetic design. The premium segment is also benefiting from the growing trend of smart kitchens and connected appliances, enabling manufacturers to command higher margins.

Explore more data points, trends and opportunities Download Free Sample Report

Slow Cooker Market Segmentations

By Product Type

- Manual Slow Cookers

- Programmable Slow Cookers

- Smart Slow Cookers

By Capacity

- Small

- Medium

- Large

By Application

- Residential/Household

- Restaurants & Cafés

- Catering Services

- Institutional Kitchens

By Distribution Channel

- Online Retail

- Supermarkets/Hypermarkets

- Specialty Appliance Stores

- Department Stores

By Price Range

- Economy

- Mid-Range

- Premium

Regional Insights

North America

North America holds the largest share of the global slow cooker market at approximately 38% in 2025, with the United States accounting for the majority of regional demand. Growth in this region is driven by high product penetration, strong consumer awareness, and a well-established culture of convenience cooking. The widespread adoption of dual-income households and busy lifestyles has significantly increased demand for time-saving kitchen appliances. Additionally, the region is witnessing strong uptake of smart and programmable slow cookers, supported by high smart home penetration and technological adoption. Canada also contributes significantly, benefiting from similar consumption patterns, high disposable income, and increasing preference for energy-efficient appliances.

Europe

Europe accounts for around 27% of the global market, with key demand from the United Kingdom, Germany, and France. The region’s growth is strongly influenced by increasing awareness of energy efficiency and sustainability. Consumers are actively seeking appliances that reduce energy consumption while maintaining cooking quality, positioning slow cookers as an attractive option. Additionally, rising electricity costs across Europe are encouraging the adoption of low-energy cooking solutions. The popularity of home cooking, particularly in Western Europe, and the growing demand for compact kitchen appliances in urban households are further driving market expansion. The UK remains a leading market due to cultural preference for slow-cooked meals.

Asia-Pacific

Asia-Pacific represents approximately 22% of the global market and is the fastest-growing region, with a CAGR of around 7.5%. China and India are the primary growth drivers, supported by rapid urbanisation, rising disposable incomes, and expanding middle-class populations. Increasing exposure to Western cooking habits and growing demand for modern kitchen appliances are accelerating adoption. The rapid growth of e-commerce platforms is also playing a crucial role in improving product accessibility. In addition, smaller household sizes and compact living spaces are driving demand for multifunctional and space-efficient appliances. Japan and South Korea are witnessing demand for technologically advanced and compact slow cookers, driven by innovation-focused consumer preferences.

Latin America

Latin America holds about 7% of the global market, with Brazil and Mexico leading demand. Growth in this region is driven by the expansion of the middle-class population, increasing urbanisation, and rising awareness of modern kitchen appliances. Improving retail infrastructure and growing penetration of e-commerce platforms are enhancing product accessibility. Additionally, the region’s strong culture of home cooking and demand for cost-effective cooking solutions are supporting steady adoption of slow cookers.

Middle East & Africa

The Middle East & Africa region accounts for nearly 6% of the global market. Key demand centres include the UAE and South Africa, where urbanisation, rising disposable incomes, and growing expatriate populations are driving appliance adoption. The increasing influence of Western lifestyles and cooking practices is also contributing to market growth. In addition, the expansion of modern retail formats and e-commerce platforms is improving product availability. While the market is still in a developing stage, increasing awareness and gradual adoption of smart kitchen appliances are expected to support long-term growth in the region.

Key Players in the Slow Cooker Market

- Crock-Pot (Newell Brands)

- Hamilton Beach Brands

- Instant Brands

- Breville Group

- Koninklijke Philips

- Panasonic Corporation

- Electrolux AB

- Whirlpool Corporation

- SEB Group

- Morphy Richards

- Russell Hobbs

- Aroma Housewares

- Black+Decker

- Cuisinart

- KitchenAid