Slot Machine Market Size

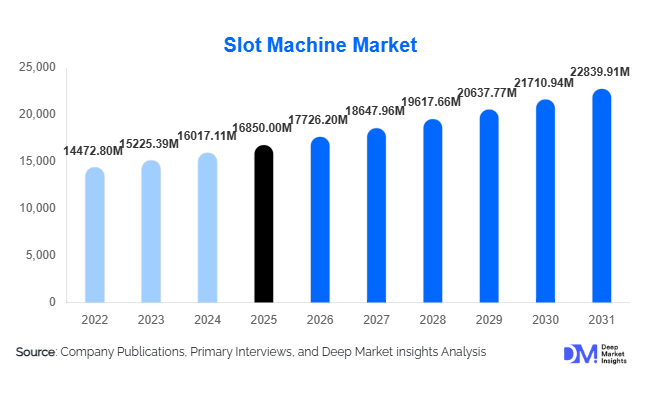

According to Deep Market Insights, the global slot machine market size was valued at USD 16,850 million in 2025 and is projected to grow from USD 17,726.20 million in 2026 to reach USD 22,839.91 million by 2031, expanding at a CAGR of 5.2% during the forecast period (2026–2031). The market growth is primarily driven by expanding casino infrastructure, replacement demand across mature gaming jurisdictions, increasing adoption of server-based gaming systems, and the steady rise of regulated online slot platforms. Slot machines continue to generate nearly two-thirds of total casino floor revenues globally, making them the most critical revenue engine for commercial and tribal gaming operators. Growth in integrated resort developments across Asia-Pacific and regulatory modernization in select Latin American and European markets further support steady long-term expansion.

Key Market Insights

- Video slot machines dominate globally, accounting for over 50% of total installations due to immersive graphics and multi-line gameplay features.

- North America holds the largest market share (around 42%), led by strong replacement cycles in the United States.

- Asia-Pacific is the fastest-growing region, supported by integrated resort expansion and regulatory developments.

- Participation (revenue-sharing) models are increasing, now representing nearly 45% of new installations globally.

- Cashless gaming and server-based platforms are reshaping casino floor management and enhancing analytics-driven revenue optimization.

- Online slot integration is accelerating, with omnichannel content strategies linking land-based and digital platforms.

What are the latest trends in the slot machine market?

Shift Toward Cashless and Server-Based Gaming

Casino operators are increasingly deploying ticket-in-ticket-out (TITO) systems, mobile wallet integrations, and centralized server-based architectures. These technologies enable dynamic game configuration, real-time analytics, and enhanced player tracking. Cashless gaming improves operational efficiency, reduces handling costs, and enhances regulatory compliance. In major markets such as the United States and parts of Europe, regulatory bodies are approving digital wallet-based casino ecosystems, positioning cashless infrastructure as a standard feature in new installations. Server-based gaming also allows casinos to update content remotely, reducing downtime and increasing floor productivity.

Premium Cabinets and Immersive Content

Manufacturers are focusing on curved 4K displays, multi-screen cabinets, surround sound systems, and branded entertainment themes to enhance player engagement. Licensed content partnerships with entertainment franchises are driving premium pricing and higher win-per-unit performance. Progressive jackpot systems continue to attract high-value players seeking life-changing payouts. Immersive and skill-influenced slot formats are also emerging to attract younger demographics, combining elements of interactive gaming with traditional slot mechanics.

What are the key drivers in the slot machine market?

Expansion of Legalized Gaming Markets

Governments in the Asia-Pacific and Latin America are gradually liberalizing gaming regulations to boost tourism and tax revenues. Integrated resort developments in markets such as Japan and the Philippines require large-scale slot installations, often exceeding 2,000 machines per property. These greenfield developments significantly boost primary sales for manufacturers.

Replacement Demand in Mature Markets

In North America, the average slot machine replacement cycle ranges between 5 and 7 years. Casinos consistently upgrade cabinets to maintain player engagement and comply with evolving regulatory standards. Replacement demand accounts for nearly 60% of annual shipments in mature jurisdictions, ensuring stable baseline revenue for manufacturers.

What are the restraints for the global market?

Regulatory Complexity

The slot machine industry is highly regulated, with each jurisdiction requiring certification, licensing, and compliance testing. Policy shifts, tax increases, or delays in gaming approvals can postpone casino projects and reduce capital expenditure commitments from operators.

Social Concerns and Responsible Gaming Measures

Public opposition to gambling expansion and stricter responsible gaming regulations may limit installation growth. Advertising restrictions, mandatory player tracking, and betting limits can moderate revenue expansion in certain regions.

What are the key opportunities in the slot machine industry?

Omnichannel Gaming Convergence

Manufacturers that provide unified content libraries across land-based and online platforms are gaining a competitive advantage. Operators increasingly demand seamless integration between physical cabinets and digital slot ecosystems. This convergence creates recurring licensing revenue streams and strengthens brand loyalty.

Emerging Latin American and Asian Markets

Regulatory reforms in Brazil and Southeast Asia are creating new market entry opportunities. Early partnerships with local operators and governments allow global manufacturers to secure long-term supply contracts and participation agreements.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 16850 Million |

| Market Size in 2026 | USD 17726.20 Million |

| Market Size in 2031 | USD 22839.91 Million |

| CAGR | 5.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Video slot machines lead the global market, accounting for approximately 54% of total revenue in 2025. Their dominance is primarily driven by advanced graphics engines, immersive multi-screen cabinets, skill-enhanced bonus features, and multi-denomination flexibility that appeal to both casual and high-frequency players. The shift from mechanical reels to fully digital video formats has enabled manufacturers to integrate licensed entertainment content, progressive jackpot linkages, and real-time software upgrades. Casinos favor video slots due to their higher average win-per-unit (WPU) performance and stronger player retention metrics compared to traditional mechanical models.

Progressive jackpot slot machines represent around 22% of the market, supported by strong demand from high-stakes players seeking large pooled prize payouts. Wide-area progressive (WAP) networks that connect machines across multiple casinos significantly enhance jackpot sizes, increasing footfall and dwell time. Meanwhile, multi-game cabinets are gaining adoption in space-constrained casino environments, particularly in mature North American and European markets, as operators aim to optimize floor productivity and maximize revenue per square foot. These cabinets allow operators to rotate game libraries without physical machine replacement, reducing capital expenditure while improving content refresh cycles.

Technology Platform Insights

Standalone land-based slot machines continue to dominate with nearly 68% market share in 2025, driven by strong physical casino footfall and replacement demand across established gaming jurisdictions. The leading position of this segment is reinforced by long-term infrastructure investments in commercial and tribal casinos, particularly in the United States, where replacement cycles occur every 5–7 years.

However, server-based and networked slot systems are witnessing accelerated adoption as casinos modernize floor management. These systems allow centralized game configuration, performance analytics, and remote content updates, significantly reducing operational downtime. Digital and online slots represent the fastest-growing sub-segment, supported by regulatory expansion of iGaming in Europe and select U.S. states. Omnichannel strategies, where the same game titles are deployed across physical cabinets and online platforms, are further strengthening digital growth and recurring content licensing revenue for manufacturers.

Deployment Location Insights

Casinos dominate deployment, contributing approximately 72% of global slot machine revenue in 2025. The leadership of this segment is directly linked to large-scale gaming floors in integrated resorts and commercial casinos, where slots account for nearly two-thirds of total gaming revenue. Commercial casinos remain the primary procurement drivers due to consistent reinvestment in premium cabinets and participation-based installations.

Tribal casinos in the United States significantly influence replacement demand, supported by stable gaming revenues and reinvestment mandates. Cruise ships represent a niche but steadily expanding segment, driven by global cruise tourism recovery and rising onboard entertainment spending. Route operations and distributed gaming locations, such as licensed bars and entertainment centers, are growing selectively in regulated European and North American jurisdictions where limited gaming terminals are permitted.

Ownership Model Insights

The participation or revenue-sharing model represents roughly 45% of new installations globally, making it the fastest-expanding ownership format. Under this model, manufacturers install machines at reduced upfront cost while sharing revenue generated from gameplay. The segment’s growth is driven by operator preference for capital-light strategies, particularly during economic uncertainty. Participation agreements also incentivize manufacturers to deploy high-performing premium content, as revenues are directly linked to machine productivity. Direct sales remain prevalent in emerging markets and new casino developments where operators prefer asset ownership, while leasing models are selectively used in smaller jurisdictions.

End-User Insights

Commercial casinos account for approximately 58% of total global demand, supported by integrated resort expansion, tourism inflows, and reinvestment in premium gaming floors. Tribal casinos represent around 28% of demand, particularly strong in the United States, where tribal gaming continues to expand under sovereign regulatory frameworks. Online gaming operators are the fastest-growing end-user segment, expanding at a significantly higher CAGR than land-based casinos. Regulatory approvals in Europe and North America, combined with rising digital payment adoption, are accelerating online slot deployment. The integration of physical casino brands into digital ecosystems further enhances cross-platform engagement and brand monetization opportunities.

Explore more data points, trends and opportunities Download Free Sample Report

Slot Machine Market Segmentations

By Product Type

- Mechanical Slot Machines

- Video Slot Machines

- Multi-Game Slot Machines

- Progressive Jackpot Slot Machines

- ETG-Integrated Slot Units

By Technology Platform

- Standalone Land-Based Slot Machines

- Server-Based / Networked Slot Machines

- Digital / Online Slot Machines

By Deployment Location

- Casinos

- Gaming Arcades & Entertainment Centers

- Bars & Clubs (Limited Gaming Venues)

- Cruise Ships

- Route Operations

By Ownership Model

- Direct Sales

- Participation / Revenue-Sharing

- Leasing Model

By End-User

- Commercial Casinos

- Tribal Casinos

- Government-Owned Gaming Facilities

- Online Gaming Operators

Regional Insights

North America

North America holds approximately 42% of the global market share in 2025, with the United States accounting for nearly 38% of worldwide demand. Regional growth is primarily driven by stable replacement cycles, strong tribal gaming revenues, and continuous capital reinvestment in premium cabinets. The presence of large-scale commercial casinos in Las Vegas and regional gaming hubs ensures consistent procurement. Expansion of cashless gaming approvals and server-based upgrades further strengthens modernisation-driven demand. Canada contributes through provincially regulated gaming systems, where government-operated casinos maintain structured replacement programs and compliance-driven upgrades.

Asia-Pacific

Asia-Pacific represents roughly 26% of global revenue and is the fastest-growing region with an estimated CAGR exceeding 7%. Growth is fueled by integrated resort expansion in Macau and the Philippines, alongside the long-term impact of Japan’s integrated resort development pipeline. Rising tourism inflows, growing middle-class disposable income, and government-backed resort infrastructure projects are major demand catalysts. Casinos in the region typically deploy high machine densities per property, amplifying installation volumes. Additionally, Southeast Asian markets are gradually liberalising gaming policies, creating incremental opportunities for global manufacturers.

Europe

Europe accounts for approximately 21% of the global market, led by the United Kingdom, Germany, and Italy. Regional growth is supported by the modernisation of gaming halls, the expansion of regulated online gambling frameworks, and technological upgrades in server-based gaming systems. Strict compliance standards drive regular machine replacement and certification upgrades. Furthermore, distributed gaming models in licensed betting shops and entertainment venues sustain steady machine demand across select European jurisdictions.

Latin America

Latin America is emerging as a high-growth frontier, with Brazil and Mexico leading demand. Regulatory reforms encouraging casino legalisation and structured licensing frameworks are driving new installations. The region benefits from low penetration levels, creating strong greenfield opportunities. Rising tourism, increasing foreign direct investment in hospitality infrastructure, and improving macroeconomic stability are additional regional growth drivers.

Middle East & Africa

The Middle East & Africa region currently represents a smaller share of global demand but demonstrates long-term potential. Growth is primarily driven by tourism-oriented casino developments and cruise-based gaming operations. South Africa remains the largest contributor within Africa due to its established casino industry and regulatory clarity. In select Middle Eastern jurisdictions, large-scale tourism and hospitality investments are gradually opening discussions around regulated gaming frameworks, which could unlock future demand for slot installations.

Key Players in the Slot Machine Market

- International Game Technology (IGT)

- Light & Wonder

- Aristocrat Leisure Limited

- NOVOMATIC

- Konami Gaming

- Ainsworth Game Technology

- Everi Holdings

- AGT (Apex Gaming Technology)

- Incredible Technologies

- Zitro

- Playtech

- Scientific Games

- Universal Entertainment

- Gaming Arts

- TCS John Huxley