Ski Glasses Market Size

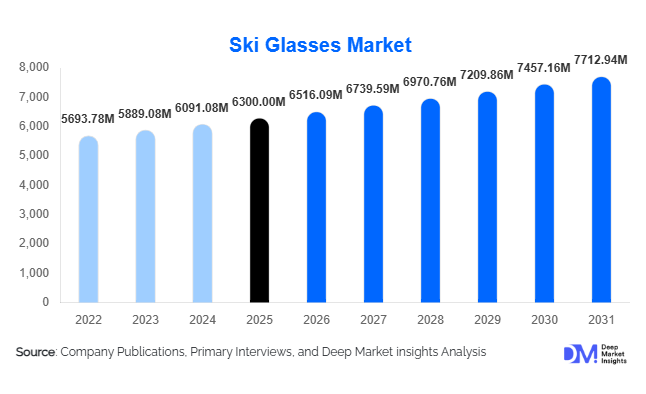

According to Deep Market Insights, the global ski glasses market size was valued at USD 6,300.00 million in 2025 and is projected to grow from USD 6,516.09 million in 2026 to reach USD 7,712.94 million by 2031, expanding at a CAGR of 3.43% during the forecast period (2026–2031). The ski glasses market growth is primarily driven by rising participation in winter sports, increasing safety awareness among skiers and snowboarders, rapid product innovation in lens technologies, and the growing popularity of premium and smart ski eyewear.

Key Market Insights

- Premium and mid-range ski glasses dominate demand, as consumers increasingly prioritize optical clarity, comfort, and anti-fog performance.

- Europe and North America together account for over 65% of global demand, supported by mature ski infrastructure and high winter sports participation.

- Asia-Pacific is the fastest-growing region, driven by government-backed winter sports initiatives and rising disposable income.

- Interchangeable and photochromic lenses are gaining traction as skiers seek adaptability across weather conditions.

- E-commerce and direct-to-consumer channels are reshaping purchasing behavior, offering wider product access and customization.

- Smart ski glasses with HUD and connectivity features are emerging as a high-growth niche within the premium segment.

What are the latest trends in the ski glasses market?

Shift Toward Advanced Lens Technologies

Lens innovation remains the most influential trend shaping the ski glasses market. Interchangeable lens systems, polarized lenses, and photochromic technologies are increasingly preferred as they allow skiers to adapt to varying light and weather conditions. Anti-fog coatings and enhanced ventilation designs have become standard features, significantly improving on-slope visibility and safety. These advancements are driving replacement demand and encouraging consumers to upgrade from basic goggles to technologically advanced models.

Emergence of Smart and Connected Ski Glasses

Smart ski glasses equipped with heads-up displays, GPS tracking, speed metrics, and smartphone connectivity are gradually entering the mainstream. While currently concentrated in the premium segment, declining component costs and growing interest among tech-savvy and professional skiers are accelerating adoption. Smart features enhance performance tracking and safety, positioning connected ski glasses as a future growth engine for the market.

What are the key drivers in the ski glasses market?

Growing Participation in Winter Sports

Rising global participation in skiing and snowboarding is a primary driver of market growth. Expansion of ski resorts, increased winter tourism, and growing youth engagement are fueling consistent demand for ski glasses across recreational and beginner segments. Indoor ski facilities and artificial snowmaking are further mitigating seasonality risks, supporting year-round demand in select regions.

Product Premiumization and Safety Awareness

Consumers are increasingly willing to invest in premium ski glasses that offer superior protection, UV filtering, and optical performance. Heightened awareness around eye safety in extreme weather conditions is pushing demand toward certified, high-quality products. This premiumization trend is boosting average selling prices and overall market value.

What are the restraints for the global market?

Climate Variability and Shorter Ski Seasons

Unpredictable snowfall patterns and climate change pose challenges for the ski glasses market. Shortened ski seasons in traditional regions can negatively impact equipment sales and replacement cycles. Although artificial snowmaking offers partial mitigation, long-term climate risks remain a concern for market stability.

Price Sensitivity in Emerging Markets

High-quality ski glasses, particularly premium and smart variants, remain expensive for first-time users in emerging economies. This price sensitivity limits adoption unless supported by rental programs, entry-level offerings, or localized manufacturing to reduce costs.

What are the key opportunities in the ski glasses industry?

Expansion in Asia-Pacific Winter Sports Markets

Asia-Pacific presents a major growth opportunity, led by China, Japan, and South Korea. Government investments in winter sports infrastructure and rising middle-class participation are creating strong demand for entry-level and mid-range ski glasses. Early brand establishment in these markets can deliver long-term growth advantages.

Sustainable and Eco-Friendly Product Development

Growing consumer preference for sustainable products is opening opportunities for ski glasses made from recycled frames, bio-based materials, and environmentally friendly coatings. Brands aligning with sustainability and ESG goals can attract eco-conscious consumers and command premium pricing.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 6300 Million |

| Market Size in 2026 | USD 6516.09 Million |

| Market Size in 2031 | USD 7712.94 Million |

| CAGR | 3.43% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Spherical lens ski glasses dominate the global market due to their superior peripheral vision, reduced optical distortion, and enhanced comfort, accounting for approximately 34% of the 2024 market. These lenses are particularly preferred by professional and recreational skiers who prioritize performance and safety in varied skiing conditions. Cylindrical and traditional dual-lens models continue to maintain strong demand among recreational and entry-level skiers, primarily driven by affordability, durability, and ease of replacement. Smart ski glasses, though currently a niche segment, are witnessing rapid growth within the premium category due to the integration of features such as heads-up displays, GPS tracking, speed monitoring, and smartphone connectivity. The adoption of smart ski glasses is further supported by tech-savvy skiers and increasing interest in performance analytics, indicating that this segment may gain significant market share by 2030.

Lens Technology Insights

Interchangeable lens systems lead the market with nearly 29% share, driven by their versatility across varying light conditions and the ability to reduce the need for multiple goggles. Professional and frequent skiers favor these systems because they ensure consistent visual clarity in changing weather and light environments, enhancing safety and performance. Photochromic and polarized lenses are witnessing growing adoption due to their adaptive light-filtering properties, which protect against glare, UV exposure, and snow blindness. These lens technologies are also increasingly preferred in regions with highly variable weather, contributing to their steady market expansion.

Distribution Channel Insights

Online and direct-to-consumer (DTC) channels account for approximately 38% of global ski glasses sales, reflecting the increasing shift toward digital purchasing, customization, and brand loyalty programs. Specialty sports retailers remain a critical channel for premium and professional buyers who prefer in-store fitting, expert guidance, and trial of advanced features. Additionally, resort-based retail and rental shops continue to support impulse purchases, short-term rentals, and seasonal replacements, particularly in regions with high winter sports tourism. The combined effect of e-commerce expansion and resort-based sales is facilitating faster market penetration and driving overall revenue growth.

User Type Insights

Recreational skiers represent the largest user group, contributing nearly 56% of global demand. This segment drives consistent demand across mid-range and entry-level products. Professional and competitive skiers influence product innovation adoption, premium sales, and advanced lens technologies. Meanwhile, beginners and youth segments are expanding steadily, especially in emerging ski markets, sustaining demand for affordable and versatile ski glasses, and fostering brand loyalty early in the user lifecycle.

Explore more data points, trends and opportunities Download Free Sample Report

Ski Glasses Market Segmentations

By Product Type

- Spherical Lens Ski Glasses

- Cylindrical Lens Ski Glasses

- Traditional Dual-Lens Ski Glasses

- Smart / HUD-Enabled Ski Glasses

- OTG (Over-The-Glasses) Ski Glasses

By Lens Technology

- Interchangeable Lens Systems

- Photochromic Lenses

- Polarized Lenses

- Standard UV-Protected Lenses

- Anti-Fog & Anti-Scratch Coated Lenses

By Distribution Channel

- Online / Direct-to-Consumer

- Specialty Sports Retail Stores

- Resort-Based & Rental Shops

- E-Commerce Marketplaces

By User Type

- Recreational Skiers

- Professional / Competitive Skiers

- Beginners & Training Participants

- Children & Youth Skiers

By End Use

- Alpine Skiing

- Snowboarding

- Freestyle / Terrain Park Sports

- Ski Touring & Mountaineering

- Military & Cold-Climate Industrial Use

Regional Insights

Europe

Europe leads the global ski glasses market with approximately 36% share in 2024, driven by high participation in winter sports across France, Switzerland, Austria, Italy, and Germany. Strong ski culture, dense networks of ski resorts, and widespread adoption of safety standards support sustained demand across all price segments. Key drivers include rising consumer awareness of eye protection in alpine sports, the popularity of professional competitions and recreational skiing, and a high propensity for premium and technologically advanced products. Government and private investments in ski resort upgrades and winter sports infrastructure further encourage the adoption of premium lenses and smart ski glasses in the region.

North America

North America accounts for around 31% of global demand, with the United States and Canada as primary contributors. High disposable incomes, strong recreational skiing culture, and established winter tourism infrastructure drive demand for premium and smart ski glasses. Key growth drivers include the rising popularity of snowboarding and freestyle skiing, increased focus on safety equipment and wearable technology, and expanding indoor skiing facilities that extend seasonal use. Consumer willingness to invest in advanced lens technologies, including photochromic and interchangeable lenses, supports higher average selling prices and robust market growth.

Asia-Pacific

Asia-Pacific is the fastest-growing region, expanding at over 7.5% CAGR. China represents the fastest-growing country market due to government-backed winter sports programs, Olympic legacy infrastructure, and the rapid expansion of indoor ski facilities. Key drivers include rising middle-class disposable income, increasing winter tourism participation, and the establishment of modern ski resorts in Japan, South Korea, and India. Additionally, growing awareness of eye safety and advanced sports equipment among recreational and professional skiers is driving the adoption of premium lenses and smart ski glasses, particularly in urban centers with access to winter sports destinations.

Latin America

Latin America holds a smaller market share but shows emerging growth in countries such as Chile and Argentina, supported by seasonal tourism and ski resorts in the Andes. Growth is primarily driven by increasing participation in recreational skiing, rising inbound and domestic winter sports tourism, and the adoption of mid-range ski glasses among first-time users. Additionally, local ski competitions and expanding resort amenities are gradually fostering a culture of premium ski equipment adoption.

Middle East & Africa

This region accounts for limited but growing demand, primarily supported by indoor ski facilities in the UAE and the increasing participation of high-income consumers in winter sports tourism. Drivers include the rising interest in experiential and luxury adventure sports, regional investments in artificial ski slopes, and increased exposure to European and North American winter sports culture. Premium and smart ski glasses are particularly favored in urban centers with affluent consumers seeking high-end recreational experiences.

Key Players in the Ski Glasses Market

- EssilorLuxottica (Oakley)

- Safilo Group

- Smith Optics

- Giro Sport Design

- Bollé Brands

- Julbo Group

- POC Sports