Self-Tanning Products Market Size

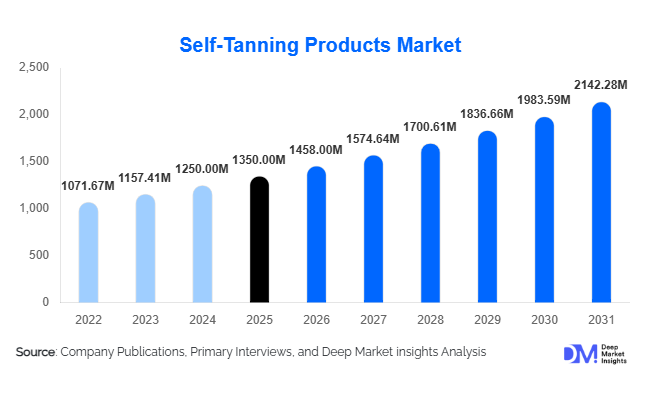

According to Deep Market Insights, the global self-tanning products market size was valued at USD 1,350 million in 2025 and is projected to grow from USD 1,458.00 million in 2026 to reach USD 2,142.28 million by 2031, expanding at a CAGR of 8.0% during the forecast period (2026–2031). The market growth is primarily driven by rising consumer awareness regarding the harmful effects of UV exposure, increasing demand for safer alternatives to sun tanning, and rapid advancements in product formulations that deliver natural-looking results.

Key Market Insights

- Consumers are increasingly shifting toward UV-free tanning solutions, driven by growing awareness of skin cancer and premature aging risks associated with sun exposure.

- Premium and clean-label products are gaining traction, with demand rising for organic, vegan, and dermatologically tested formulations.

- North America dominates the market, supported by strong consumer awareness, high disposable income, and widespread adoption of beauty trends.

- Asia-Pacific is the fastest-growing region, fueled by urbanization, rising middle-class incomes, and evolving beauty standards.

- E-commerce channels are rapidly expanding, enabling direct-to-consumer sales and increasing visibility of niche and indie brands.

- Technological innovation in formulations, including odor-free, streak-free, and customizable tanning solutions, is enhancing user experience.

What are the latest trends in the self-tanning products market?

Shift Toward Natural and Organic Formulations

The self-tanning products market is witnessing a strong shift toward natural and organic ingredients. Consumers are increasingly demanding clean-label products free from parabens, sulfates, and synthetic additives. Manufacturers are incorporating plant-based actives and botanical extracts to meet this demand. This trend is particularly prominent in North America and Europe, where regulatory frameworks and consumer awareness support sustainable and safe cosmetics. Brands are also leveraging certifications such as cruelty-free and vegan to differentiate their offerings, enhancing brand trust and premium positioning.

Personalization and Technology Integration

Technological advancements are enabling greater personalization in self-tanning products. Customizable tanning drops and serums allow users to control intensity and shade, catering to diverse skin tones. AI-powered skin analysis tools and augmented reality (AR) applications are improving online shopping experiences by helping consumers visualize results before purchase. Additionally, innovations in formulation chemistry, such as fast-drying and long-lasting effects, are improving convenience and user satisfaction, making self-tanning more accessible to first-time users.

What are the key drivers in the self-tanning products market?

Rising Awareness of Skin Health

Growing awareness of the harmful effects of UV radiation is a major driver for the market. The increasing incidence of skin cancer and dermatological concerns has led consumers to seek safer alternatives to traditional tanning methods. Public health campaigns and dermatological recommendations are reinforcing the adoption of self-tanning products globally.

Influence of Beauty and Social Media Trends

The rise of social media platforms and beauty influencers has significantly shaped consumer preferences. A bronzed and even skin tone is increasingly associated with aesthetic appeal, driving demand among millennials and Gen Z. Influencer endorsements and product tutorials have improved consumer confidence and accelerated product adoption.

What are the restraints for the global market?

Application Challenges and Product Performance Issues

Despite advancements, achieving a flawless tan remains a challenge for many users. Issues such as streaking, uneven application, and color inconsistencies can lead to dissatisfaction, impacting repeat purchases and brand loyalty.

Availability of Alternative Cosmetic Products

Temporary cosmetic alternatives such as bronzers, tinted moisturizers, and body makeup provide instant results without long-term commitment. These substitutes pose a challenge to the growth of self-tanning products, particularly among casual users seeking convenience.

What are the key opportunities in the self-tanning products industry?

Expansion in Emerging Markets

Emerging economies in the Asia-Pacific and Latin America present significant growth opportunities. Rising disposable incomes, urbanization, and exposure to global beauty trends are driving demand in countries such as India, Brazil, and China. Localized marketing strategies and tailored formulations for diverse skin tones can unlock substantial untapped potential.

Innovation in Product Personalization

The development of customizable and multifunctional products is creating new growth avenues. Hybrid formulations that combine skincare benefits with tanning effects, along with adjustable intensity products, are gaining popularity. Companies investing in R&D and digital integration can capture a larger share of tech-savvy consumers.

Product Type Insights

Lotions and creams dominate the self-tanning products market, accounting for approximately 32% of the global market share in 2025. Their leadership is primarily driven by consumer preference for ease of application, gradual tanning results, and added skincare benefits such as hydration and nourishment. These products are especially popular among first-time users and consumers seeking natural-looking results, as they allow controlled build-up of color over time. Additionally, the integration of skincare ingredients such as hyaluronic acid, aloe vera, and vitamins has strengthened their positioning as hybrid beauty products, further accelerating demand.

Sprays and mousses are gaining traction among experienced users and professional segments due to their quick-drying formulations, streak-free finish, and salon-like results. These formats are particularly popular in urban markets where convenience and speed are key purchase drivers. Meanwhile, drops and concentrates represent a fast-growing niche segment, driven by the trend toward personalization and customizable beauty routines, allowing consumers to mix tanning solutions with existing skincare products.

Application Insights

Body-specific products hold the largest share at around 55% of the market, primarily due to higher usage volume, broader surface area application, and recurring consumption patterns. Consumers often prioritize body tanning for aesthetic purposes, particularly in regions with strong beach culture and seasonal fashion trends, which further reinforces this segment’s dominance.

Face-specific products are witnessing robust growth, supported by increasing demand for skincare-infused formulations that combine tanning with anti-aging, hydration, and sun-care benefits. The rise of facial aesthetics and skincare routines has significantly contributed to this trend. Multi-purpose products that can be used on both face and body are also expanding steadily, driven by consumer demand for convenience, cost efficiency, and minimalist beauty routines, particularly among younger demographics.

Distribution Channel Insights

Online retail channels account for approximately 38% of the market share and represent the fastest-growing segment. This growth is driven by increasing digital adoption, influencer marketing, and direct-to-consumer (D2C) brand strategies. E-commerce platforms enable consumers to access a wide product range, compare prices, read reviews, and benefit from personalized recommendations, significantly improving purchase confidence.

Offline channels, including specialty beauty stores, pharmacies, and supermarkets, continue to play a critical role, particularly for premium and dermatologist-recommended products. Consumers often prefer physical stores for product testing and expert consultation, especially for skincare-related purchases. The coexistence of omnichannel strategies is becoming a key growth driver, as brands integrate both online and offline touchpoints to enhance customer engagement.

End-User Insights

Individual consumers dominate the market with over 80% share, driven by the growing trend of at-home beauty treatments, convenience, and cost savings compared to professional services. The COVID-19 pandemic accelerated this shift, and the trend has persisted due to increased consumer confidence in self-application and availability of easy-to-use products.

The professional segment, including salons, dermatology clinics, and spas, is expanding at a faster pace, supported by demand for precision application, long-lasting results, and premium experiences. Spray tanning services and customized treatments are particularly popular in urban areas and among high-income consumers, contributing to the segment’s higher growth rate despite its smaller base.

Price Range Insights

The premium segment leads the market with around 40% share, reflecting strong consumer inclination toward high-quality, skin-friendly, and clean-label products. Premium products often incorporate organic ingredients, advanced formulations, and multifunctional benefits, which justify higher price points and enhance brand loyalty.

Mass-market products continue to drive volume sales, particularly in emerging markets where price sensitivity remains high. Meanwhile, luxury and professional-grade products cater to niche high-income consumers seeking exclusive formulations, superior performance, and brand prestige. The ongoing premiumization trend is expected to further expand margins and drive innovation across the market.

| By Product Type | By Application | By Distribution Channel |

|---|---|---|

|

|

|

Regional Insights

North America

North America holds the largest share of approximately 38% of the global market, with the United States contributing nearly 30%. The region’s dominance is driven by high consumer awareness regarding UV-related skin risks, strong adoption of beauty and wellness trends, and widespread use of premium personal care products. Additionally, the presence of major global brands, robust e-commerce infrastructure, and strong influence of social media and celebrity endorsements significantly boost market demand. Seasonal demand patterns, particularly in summer, and a well-established tanning culture further reinforce growth in this region.

Europe

Europe accounts for around 30% of the market share, led by the UK, Germany, and France, with the UK alone contributing nearly 10%. Growth in this region is driven by high consumer preference for clean-label, vegan, and sustainable products, supported by stringent regulatory frameworks. The strong tanning culture, especially in Western Europe, combined with increasing adoption of premium skincare-integrated tanning solutions, is fueling demand. Additionally, the rise of eco-conscious consumers and demand for cruelty-free cosmetics are encouraging innovation and product diversification.

Asia-Pacific

Asia-Pacific is the fastest-growing region, with a CAGR exceeding 10% and a current share of about 18%. Growth is driven by rising disposable incomes, rapid urbanization, and increasing exposure to global beauty trends through digital platforms. Countries such as China, India, Japan, and Australia are key contributors. Australia shows strong adoption due to high awareness of sun safety, while emerging markets like India and China are witnessing increasing demand among urban youth. The expansion of e-commerce and the influence of international beauty brands are further accelerating regional growth.

Latin America

Latin America holds approximately 8% of the market, with Brazil and Mexico leading demand. The region’s growth is driven by strong beauty consciousness, cultural emphasis on appearance, and increasing adoption of Western beauty trends. Brazil, in particular, represents a high-potential market due to its large cosmetics industry and favorable climate that supports year-round demand for tanning products. Rising middle-class income and expanding retail infrastructure are also contributing to market expansion.

Middle East & Africa

The Middle East & Africa region accounts for around 6% of the market. Growth is concentrated in urban centers such as the UAE and South Africa and is driven by rising disposable incomes, increasing adoption of international beauty standards, and growing influence of social media. The premium segment is particularly strong in the Middle East due to high purchasing power, while Africa is witnessing gradual growth supported by urbanization and expanding retail networks. Increasing awareness of skincare and beauty products is expected to further boost demand in the coming years.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Self-Tanning Products Market

- L'Oréal Group

- Estée Lauder Companies

- Beiersdorf AG

- Coty Inc.

- Shiseido Company

- Johnson & Johnson

- Unilever

- Kao Corporation

- Clarins Group

- PZ Cussons (St. Tropez)

- Vita Liberata

- Bondi Sands

- Isle of Paradise

- Loving Tan

- Tan-Luxe