Self-Cleaning Water Bottles Market Size

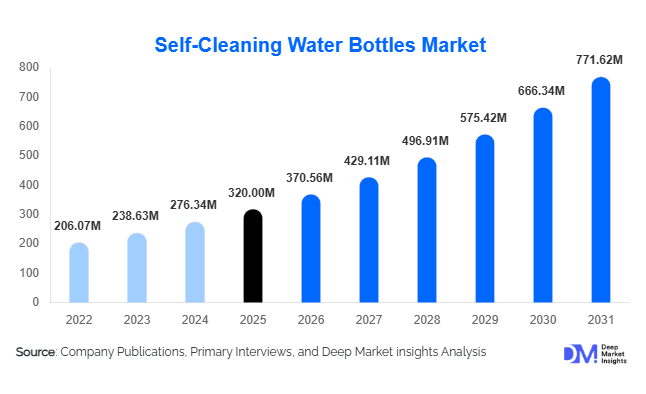

According to Deep Market Insights, the global self-cleaning water bottles market size was valued at USD 320 million in 2025 and is projected to grow from USD 370.56 million in 2026 to reach USD 771.62 million by 2031, expanding at a CAGR of 15.8% during the forecast period (2026–2031). The market growth is primarily driven by increasing consumer awareness of hygiene, rising demand for portable water purification solutions, and the growing adoption of sustainable and reusable hydration products.

Key Market Insights

- UV-C LED sterilization technology dominates the market, accounting for nearly 68% share due to its effectiveness in eliminating bacteria and viruses.

- Stainless steel bottles lead material adoption, driven by durability, insulation benefits, and premium consumer perception.

- North America dominates the global market, supported by strong consumer awareness, fitness trends, and high disposable income.

- Asia-Pacific is the fastest-growing region, fueled by urbanization, water quality concerns, and expanding middle-class populations.

- Online retail channels account for over 60% of sales, reflecting the rise of direct-to-consumer brands and e-commerce penetration.

- Mid-range priced bottles (USD 50–100) are the most popular, balancing affordability with advanced features.

What are the latest trends in the self-cleaning water bottles market?

Smart and Connected Hydration Solutions

One of the most prominent trends in the self-cleaning water bottles market is the integration of smart technologies. Manufacturers are incorporating features such as hydration tracking, mobile app connectivity, and real-time water quality monitoring. These smart bottles enable users to track their daily water intake, receive reminders, and access personalized hydration insights. The convergence of IoT and wellness devices is positioning self-cleaning bottles as part of the broader health-tech ecosystem. This trend is particularly appealing to tech-savvy consumers and fitness enthusiasts who value data-driven lifestyle management.

Sustainability-Driven Product Innovation

Sustainability is playing a crucial role in shaping product innovation. Consumers are increasingly shifting away from single-use plastics toward reusable and environmentally friendly alternatives. Self-cleaning bottles align with this trend by reducing the need for disposable bottles while ensuring hygiene. Manufacturers are focusing on eco-friendly materials, recyclable packaging, and energy-efficient sterilization technologies. Additionally, brands are emphasizing carbon-neutral production processes and sustainable sourcing, further strengthening their appeal among environmentally conscious consumers.

What are the key drivers in the self-cleaning water bottles market?

Rising Health and Hygiene Awareness

The growing awareness of waterborne diseases and microbial contamination is a key driver of market growth. Consumers are increasingly concerned about the cleanliness of reusable bottles, particularly in urban environments and during travel. Self-cleaning bottles offer a convenient solution by eliminating bacteria without requiring manual cleaning. This heightened focus on personal hygiene has significantly boosted demand across both developed and emerging markets.

Technological Advancements in UV-C Systems

Advancements in UV-C LED technology have made it possible to integrate effective sterilization systems into compact, portable bottles. Improvements in battery efficiency, durability, and cost reduction have enhanced product accessibility and performance. These innovations have enabled manufacturers to offer reliable and user-friendly solutions, driving widespread adoption.

Growing Demand for Sustainable Alternatives

Environmental concerns and regulatory pressures to reduce plastic waste are encouraging consumers to adopt reusable products. Self-cleaning water bottles provide a sustainable alternative by combining reusability with advanced hygiene features. This alignment with global sustainability goals is accelerating market growth and attracting environmentally conscious consumers.

What are the restraints for the global market?

High Product Costs

The relatively high cost of self-cleaning water bottles compared to traditional reusable bottles remains a significant barrier to adoption. Premium models with advanced features can be expensive, limiting their accessibility in price-sensitive markets. This cost factor restricts market penetration, particularly in developing regions.

Limited Awareness in Emerging Markets

Despite growing adoption in developed economies, awareness of self-cleaning technology remains limited in many emerging markets. Consumers may be unfamiliar with the benefits and functionality of these products, leading to slower adoption rates. This necessitates increased marketing and educational efforts by manufacturers.

What are the key opportunities in the self-cleaning water bottles industry?

Expansion in Emerging Economies

Emerging markets in Asia-Pacific, Latin America, and Africa present significant growth opportunities due to concerns about water quality and increasing urbanization. Governments and organizations focusing on public health can collaborate with manufacturers to promote adoption, creating both commercial and social impact opportunities.

Integration with Smart Health Ecosystems

The integration of self-cleaning bottles with wearable devices and health apps offers new avenues for innovation. Features such as hydration tracking, personalized recommendations, and connectivity with fitness platforms can enhance user experience and create premium product segments.

Institutional and Commercial Adoption

There is growing potential for adoption in corporate offices, healthcare facilities, and hospitality sectors. Organizations are increasingly prioritizing hygiene and sustainability, creating opportunities for bulk procurement and long-term partnerships with manufacturers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 320 Million |

| Market Size in 2026 | USD 370.56 Million |

| Market Size in 2031 | USD 771.62 Million |

| CAGR | 15.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Technology Type Insights

UV-C LED sterilization bottles dominate the global market with approximately 68% share in 2025, primarily due to their scientifically proven ability to eliminate up to 99.9% of bacteria and viruses. The widespread adoption of UV-C technology is driven by its ease of use, low maintenance requirements, and growing consumer trust in non-chemical purification methods. Additionally, advancements in LED miniaturization, battery efficiency, and cost optimization have significantly enhanced product affordability and performance, further strengthening this segment’s leadership. Ozone-based and electrolytic sterilization technologies occupy smaller but relevant niches, particularly in industrial or high-contamination environments where additional purification layers are required. Meanwhile, hybrid technologies, combining UV-C with ozone or electrolytic systems, are emerging within the premium segment, appealing to high-end consumers seeking advanced, multi-layered purification and superior reliability. This segment is expected to gain traction as product innovation accelerates and consumers increasingly prioritize comprehensive hygiene solutions.

Material Type Insights

Stainless steel bottles lead the market with an estimated 55% share, driven by their durability, corrosion resistance, and superior thermal insulation capabilities. These bottles are particularly favored in the premium segment due to their ability to maintain beverage temperature while offering a robust and long-lasting design. The rising consumer preference for sustainable and reusable products further supports stainless steel adoption, as it is recyclable and perceived as environmentally responsible. Plastic bottles, especially BPA-free variants such as Tritan and polypropylene, cater to the economy and mid-range segments, offering lightweight and cost-effective alternatives. However, concerns regarding long-term durability and environmental impact slightly limit their growth. Glass bottles, although niche, attract health-conscious consumers who prefer chemical-free materials, while silicone and collapsible bottles are gaining traction among travelers and outdoor users due to their portability and space-saving features. Overall, material innovation is increasingly aligned with sustainability and user convenience trends.

Capacity Insights

Bottles with capacities between 500 ml and 750 ml account for approximately 40% of the market, making them the most popular choice globally. This segment’s dominance is driven by its versatility, offering an optimal balance between portability and sufficient hydration for daily use. Urban consumers, office workers, and fitness enthusiasts particularly favor this size due to its convenience in carrying and compatibility with standard bag sizes and cup holders. Larger capacity bottles (above 1 liter) are primarily used in outdoor activities such as hiking, camping, and long-distance travel, where extended hydration is required. Conversely, smaller capacity bottles (below 500 ml) cater to short-duration usage scenarios, including commuting and casual use. The growing emphasis on personalized hydration habits and portability continues to reinforce the dominance of the mid-capacity segment.

Distribution Channel Insights

Online retail channels dominate the market with over 60% share, driven by the rapid expansion of e-commerce platforms and direct-to-consumer (D2C) business models. Consumers increasingly prefer online channels due to the convenience of product comparison, access to detailed specifications, customer reviews, and competitive pricing. Brand-owned websites and global marketplaces have enabled manufacturers to reach a wider audience while maintaining higher profit margins by reducing intermediary costs. Offline channels, including specialty stores, sports retailers, and supermarkets, continue to play an important role in enhancing product visibility and providing hands-on experience to consumers. These channels are particularly relevant for first-time buyers who prefer physical interaction before purchase. However, the ongoing digital transformation and increasing internet penetration are expected to further strengthen online dominance in the coming years.

End-Use Insights

Individual consumers represent the largest end-use segment, accounting for nearly 70% of the global market. This dominance is driven by increasing adoption among fitness enthusiasts, travelers, and urban populations seeking convenient and hygienic hydration solutions. The rising popularity of wellness and active lifestyles, coupled with growing awareness of water contamination risks, has significantly boosted demand in this segment. Institutional and commercial demand is also gaining momentum, particularly in corporate offices, healthcare facilities, and hospitality sectors. Organizations are increasingly adopting self-cleaning bottles to enhance hygiene standards, reduce reliance on single-use plastics, and align with sustainability goals. The expansion of bulk procurement models and corporate wellness programs is expected to further accelerate growth in the institutional segment.

Explore more data points, trends and opportunities Download Free Sample Report

Self-Cleaning Water Bottles Market Segmentations

By Technology Type

- UV-C LED Sterilization Bottles

- Ozone-Based Self-Cleaning Bottles

- Electrolytic Sterilization Bottles

- Hybrid Technology Bottles

By Material Type

- Stainless Steel Bottles

- Plastic (BPA-Free) Bottles

- Glass Bottles

- Silicone/Collapsible Bottles

By Capacity

- Below 500 ml

- 500 ml – 750 ml

- 751 ml – 1 Liter

- Above 1 Liter

By Distribution Channel

- Online Retail

- Specialty Stores

- Supermarkets/Hypermarkets

- Electronics Retail Stores

By End-Use

- Individual Consumers

- Corporate Offices

- Healthcare Facilities

- Hospitality Industry

- Military & Defense

Regional Insights

North America

North America holds the largest share of the global self-cleaning water bottles market at approximately 35% in 2025, with the United States being the primary contributor. The region’s dominance is driven by high consumer awareness regarding hygiene and health, strong adoption of smart and connected devices, and a well-established fitness culture. Additionally, the presence of leading market players and a mature e-commerce ecosystem supports widespread product availability. Increasing environmental awareness and government initiatives to reduce single-use plastics further contribute to market growth. The growing trend of outdoor recreation and travel also fuels demand for portable water purification solutions.

Europe

Europe accounts for around 25% of the global market, with key countries including Germany, the United Kingdom, and France driving demand. The region’s growth is strongly influenced by stringent environmental regulations and policies aimed at reducing plastic waste. Consumers in Europe are highly inclined toward sustainable and eco-friendly products, which aligns with the value proposition of self-cleaning water bottles. Additionally, increasing participation in outdoor and fitness activities, along with rising health consciousness, supports market expansion. Government-backed sustainability initiatives and circular economy frameworks are further accelerating adoption across the region.

Asia-Pacific

Asia-Pacific holds approximately 20% market share and is the fastest-growing region, with a projected CAGR exceeding 18%. Major markets such as China, Japan, and India are experiencing rapid growth due to rising urbanization, increasing disposable incomes, and heightened awareness of water quality issues. In many parts of the region, concerns regarding access to clean drinking water are driving demand for portable purification solutions. Additionally, the expansion of e-commerce platforms and the growing middle-class population are facilitating product accessibility. Government initiatives promoting health and hygiene, along with increasing adoption of smart consumer products, are key growth drivers in this region.

Latin America

Latin America represents approximately 10% of the global market, with Brazil and Mexico leading regional demand. Market growth is driven by increasing urbanization, rising middle-class income levels, and growing awareness of health and hygiene. Additionally, concerns about water quality in certain regions are encouraging consumers to adopt self-cleaning bottles as a reliable solution. The expansion of retail and e-commerce infrastructure is also improving product availability. However, price sensitivity remains a challenge, limiting the adoption of premium products in some markets.

Middle East & Africa

The Middle East & Africa region accounts for around 10% market share, with demand primarily concentrated in urban centers and water-scarce areas. The region’s growth is driven by increasing awareness of water quality issues, particularly in areas facing water scarcity and infrastructure limitations. Countries in the Middle East, such as the UAE and Saudi Arabia, are witnessing rising demand due to high disposable incomes and a strong preference for premium lifestyle products. In Africa, the market is gradually expanding as awareness improves and access to innovative hydration solutions increases. Government initiatives focused on water conservation and public health are also contributing to market growth.

Key Players in the Self-Cleaning Water Bottles Market

- LARQ Inc.

- CrazyCap

- Philips

- Hidrate Inc.

- Monos Travel

- Equa

- ICEWATER

- Water.io

- Aquapure Technologies

- UVBrite

- Pure Hydration

- HydraSmart

- Caktus Inc.

- ÖKO Water

- Loop Bottle