Secondhand Collectibles Market Size

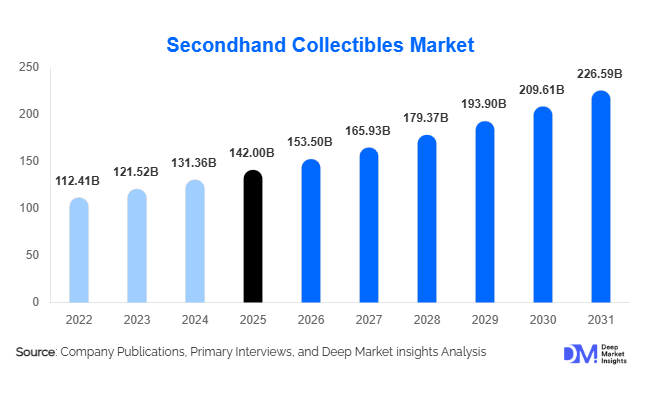

According to Deep Market Insights, the global secondhand collectibles market size was valued at USD 142.0 billion in 2025 and is projected to grow from USD 153.50 billion in 2026 to reach USD 226.59 billion by 2031, expanding at a CAGR of 8.1% during the forecast period (2026–2031). The market growth is primarily driven by increasing demand for alternative investment assets, rising digital marketplace penetration, and growing consumer interest in nostalgia-driven and culturally significant items.

The market has evolved from a niche collector-driven ecosystem into a structured and investment-grade asset class. Segments such as art, luxury watches, trading cards, and memorabilia have witnessed strong appreciation, attracting both retail collectors and institutional investors. The integration of digital technologies, including blockchain-based authentication and AI-driven valuation tools, is enhancing trust and transparency in transactions. Additionally, expanding participation from emerging markets, particularly in the Asia-Pacific region, is broadening the global consumer base and accelerating cross-border trade. Overall, the secondhand collectibles market is poised for sustained growth, supported by strong cultural, financial, and technological tailwinds.

Key Market Insights

- Collectibles are increasingly viewed as alternative investment assets, with strong returns in segments such as art, luxury watches, and trading cards.

- Online marketplaces dominate transactions, accounting for over 60% of global sales due to accessibility and transparency.

- North America leads the global market, driven by strong demand for sports memorabilia and trading cards.

- Asia-Pacific is the fastest-growing region, fueled by rising disposable incomes and an expanding collector base.

- Authentication technologies, including blockchain and AI, are reshaping trust and reducing counterfeit risks.

- Younger demographics are driving demand for pop culture collectibles, including gaming cards and vintage toys.

What are the latest trends in the secondhand collectibles market?

Digital Transformation and Online Auctions

The rapid shift toward digital platforms is redefining the secondhand collectibles market. Online auctions, peer-to-peer marketplaces, and direct-to-consumer platforms have significantly improved accessibility and liquidity. Collectors can now participate in global auctions in real time, compare prices, and access detailed product histories. Digital platforms also enable smaller collectors to enter the market, democratizing access to high-value collectibles. The integration of AI-based pricing tools and predictive analytics is further enhancing decision-making and improving transaction efficiency.

Rise of Fractional Ownership and Investment Platforms

Fractional ownership models are gaining traction, allowing investors to own shares of high-value collectibles such as rare art or vintage watches. This trend is attracting institutional investors and broadening market participation. Investment platforms are also offering curated portfolios of collectibles, positioning them as viable financial assets. This financialization is enhancing market liquidity and facilitating price discovery, particularly in segments that were previously illiquid.

What are the key drivers in the secondhand collectibles market?

Growing Demand for Alternative Investments

Investors are increasingly diversifying portfolios by including tangible assets such as collectibles. With volatility in traditional financial markets, collectibles offer a hedge against inflation and economic uncertainty. Historical price appreciation in segments like art and luxury watches has reinforced their attractiveness as long-term investments, driving sustained demand globally.

Expansion of Digital Marketplaces

The proliferation of online platforms has eliminated geographical barriers, enabling global trade of collectibles. Enhanced payment systems, logistics networks, and user-friendly interfaces have significantly improved transaction efficiency. This has led to increased participation from both buyers and sellers, contributing to overall market growth.

Rising Influence of Nostalgia and Pop Culture

Millennials and Gen Z consumers are driving demand for collectibles linked to entertainment, gaming, and sports. Social media platforms amplify trends and create communities around specific collectibles, increasing engagement and transaction volumes. This cultural influence is expanding the market beyond traditional collectors.

What are the restraints for the global market?

Lack of Standardized Valuation

The absence of uniform pricing mechanisms creates uncertainty in the market. Valuation of collectibles often depends on subjective factors such as rarity, condition, and provenance, leading to price volatility. This can deter institutional investors and new entrants from participating in the market.

Counterfeiting and Authentication Challenges

Fraud and counterfeit products remain significant concerns, particularly in high-value segments. Despite advancements in authentication technologies, the risk of forgery persists, impacting buyer confidence and slowing market expansion.

What are the key opportunities in the secondhand collectibles industry?

Technology-Driven Authentication Systems

The integration of blockchain and AI-based authentication tools presents a major opportunity for market participants. These technologies enhance transparency, verify provenance, and reduce fraud risks. Companies investing in advanced authentication systems can differentiate themselves and command premium pricing, particularly in high-value segments such as art and luxury collectibles.

Expansion in Emerging Markets

Asia-Pacific and Middle Eastern regions offer significant growth potential due to rising disposable incomes and increasing interest in collectibles. Countries such as China, India, and the UAE are witnessing strong demand growth, particularly in the luxury and trading card segments. Localized platforms and culturally relevant offerings can help companies tap into these high-growth markets effectively.

Financialization of Collectibles

The emergence of investment funds, securitization models, and fractional ownership platforms is transforming collectibles into mainstream financial assets. This trend is attracting institutional capital and enhancing market liquidity. Partnerships with financial institutions can further integrate collectibles into diversified investment portfolios, expanding market reach.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 142 Billion |

| Market Size in 2026 | USD 153.50 Billion |

| Market Size in 2031 | USD 226.59 Billion |

| CAGR | 8.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Collectible Type Insights

Art and antiques continue to dominate the secondhand collectibles market, accounting for approximately 32% of the total market share in 2025. High-value transactions, strong institutional participation, and the increasing perception of fine art as a stable long-term investment asset primarily drive this leadership. Auction houses and galleries play a pivotal role in maintaining liquidity and price discovery in this segment, while growing participation from high-net-worth individuals further reinforces demand. Luxury collectibles, including vintage watches, estate jewelry, and designer accessories, account for approximately 18% of the market. This segment is driven by strong brand equity, limited supply, and consistent resale value appreciation. The rising popularity of certified pre-owned luxury goods, combined with the expansion of authentication technologies, is further strengthening buyer confidence and supporting growth.

Numismatics and philately contribute approximately 12% of the market, supported by their intrinsic metal value, historical significance, and relatively stable pricing trends. These collectibles appeal to both investors and historians, making them less volatile compared to other segments. Entertainment memorabilia accounts for nearly 10%, driven by global fan engagement in sports, movies, and music. High-profile auctions and celebrity-linked items significantly boost visibility and demand in this category. Trading cards and gaming collectibles account for approximately 9% of the market and represent one of the fastest-growing segments. Demand is largely driven by younger demographics, digital communities, and robust resale activity, particularly in the sports and fantasy gaming card sectors.

Toys and hobby collectibles contribute approximately 7%, benefiting from nostalgia-driven demand among millennials and Gen X consumers. Limited-edition and discontinued items often command premium pricing, driving steady growth. Books and manuscripts account for around 6%, supported by institutional collectors and academic demand for rare and historical documents. Lastly, digital and hybrid collectibles account for approximately 6% of the market and are rapidly expanding due to blockchain-enabled ownership verification and the growing convergence of physical and digital assets.

End-Use Insights

Individual collectors dominate the secondhand collectibles market, contributing over 45% of total demand. This segment is driven by personal interest, cultural affinity, and emotional value associated with collectibles. The accessibility of online platforms has further expanded participation among casual and first-time collectors, significantly broadening the consumer base. The investment segment is the fastest-growing, registering a CAGR of over 10%, as collectibles increasingly gain recognition as alternative investment assets. Investors are particularly active in high-value categories such as art, luxury watches, and rare coins, where long-term appreciation and portfolio diversification benefits are evident. The emergence of fractional ownership platforms and collectible investment funds is further accelerating growth in this segment.

Museums and institutions account for approximately 15% of market demand, focusing on the preservation, curation, and exhibition of culturally and historically significant items. This segment provides stability to the market, particularly in art, manuscripts, and antiques. Auction houses, dealers, and intermediaries play a critical role in facilitating transactions, ensuring authentication, and maintaining market liquidity. Their expertise in valuation and provenance verification is essential for sustaining trust and transparency in the market. Export-driven demand is particularly strong in luxury collectibles and art, with significant trade flows from Europe and North America to Asia-Pacific markets. The global art industry alone exceeds USD 65 billion, highlighting the strong overlap and interdependence between art and collectibles demand. Increasing cross-border transactions and improved logistics networks are further supporting international trade in collectibles.

Explore more data points, trends and opportunities Download Free Sample Report

Secondhand Collectibles Market Segmentations

By Collectible Type

- Art & Antiques

- Luxury Collectibles

- Numismatics & Philately

- Entertainment Memorabilia

- Trading Cards & Gaming Collectibles

- Toys & Hobby Collectibles

- Books & Manuscripts

- Digital & Hybrid Collectibles

By End-Use

- Individual Collectors

- Investors & Investment Funds

- Museums & Institutions

- Auction Houses & Dealers

By Sales Channel

- Online Marketplaces & Auctions

- Offline Auction Houses

- Dealer Networks & Galleries

- Direct Peer-to-Peer Sales

Regional Insights

North America

North America remains the largest market, accounting for approximately 38% of the global share in 2025, with the United States leading regional demand. The region benefits from a highly developed auction ecosystem, strong collector culture, and high disposable income levels. Key growth drivers include the popularity of sports memorabilia and trading cards, the presence of major auction houses, and the widespread adoption of online marketplaces. Additionally, strong financial market awareness has encouraged investors to diversify into collectibles, further supporting regional growth.

Europe

Europe accounts for approximately 28% of the global market, with significant contributions from the UK, France, and Germany. The region’s dominance in art and antiques is supported by its rich cultural heritage and established auction infrastructure. Growth is driven by strong export activity, particularly to the Asia-Pacific, as well as increasing interest in sustainable and heritage-based assets. Government support for cultural preservation, combined with the presence of world-renowned auction houses, further reinforces Europe’s position in the global market.

Asia-Pacific

Asia-Pacific is the fastest-growing region, with a CAGR exceeding 10%, driven by rising disposable incomes and expanding middle-class populations. China accounts for nearly 18% of global demand, followed by Japan and India. Key growth drivers include increasing interest in luxury collectibles, rapid digital platform adoption, and a growing base of high-net-worth individuals. Cultural affinity for collectibles, particularly in art and antiques, along with government support for digital commerce, is further accelerating market expansion in the region.

Latin America

Latin America accounts for approximately 5% of the global market, with Brazil and Mexico being the leading contributors. Growth in the region is driven by increasing disposable incomes, rising interest in sports memorabilia, and expanding awareness of collectibles as investment assets. The growing penetration of online marketplaces is also improving accessibility and enabling cross-border transactions, supporting regional demand.

Middle East & Africa

The Middle East & Africa region accounts for around 4% of the market, with the UAE emerging as a key hub for luxury collectibles. Growth drivers include high-income populations, strong demand for premium and luxury assets, and an increasing number of investment diversification strategies. The region’s strategic location as a global trade hub and rising interest in art and cultural assets are further contributing to market expansion. Additionally, government initiatives promoting cultural tourism and art exhibitions are supporting demand for collectibles across the region.

Key Players in the Secondhand Collectibles Market

- Sotheby’s

- Christie’s

- Heritage Auctions

- Phillips

- Bonhams

- Poly Auction

- China Guardian Auctions

- Stack’s Bowers Galleries

- Catawiki

- ComicConnect

- Goldin Auctions

- Hake’s Auctions

- RR Auction

- Julien’s Auctions

- Prop Store