School Furniture Market Size

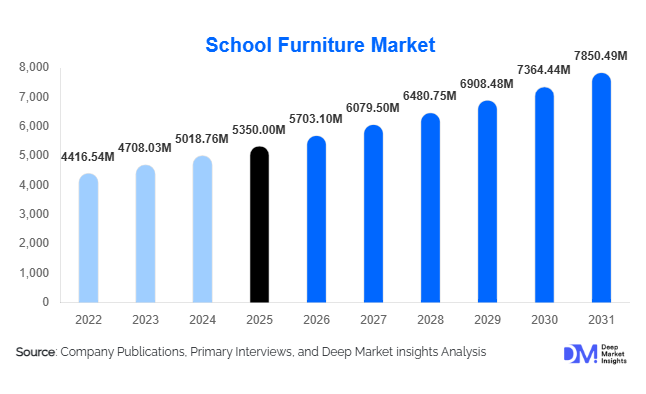

According to Deep Market Insights, the global school furniture market size was valued at USD 5,350 million in 2025 and is projected to grow from USD 5,703.10 million in 2026 to reach USD 7,850.49 million by 2031, expanding at a CAGR of 6.6% during the forecast period (2026–2031). The market growth is driven by rising global education infrastructure investments, increasing demand for ergonomic and student-centric classroom environments, rapid expansion of private and public schooling systems, and growing adoption of smart and flexible learning spaces.

Key Market Insights

- Global education infrastructure expansion is accelerating procurement of modern school furniture, particularly across Asia-Pacific and the Middle East.

- Ergonomic and modular furniture systems are gaining strong traction due to increasing focus on student health, comfort, and collaborative learning environments.

- Asia-Pacific dominates the global school furniture market, driven by large-scale school construction in China, India, and Southeast Asia.

- North America remains a premium replacement-driven market with strong demand for smart and technology-integrated classroom furniture.

- Europe is increasingly focused on sustainability-led procurement, emphasizing recyclable materials and low-carbon manufacturing standards.

- Smart classroom integration is reshaping demand patterns, with rising adoption of digital-compatible desks and flexible seating systems.

School Furniture Market Trends

Shift Toward Ergonomic and Student-Centric Design

Educational institutions are increasingly prioritizing ergonomically designed furniture to improve student posture, engagement, and long-term health outcomes. Adjustable desks, posture-support chairs, and height-flexible furniture are becoming standard in modern classrooms. This trend is strongly influenced by rising awareness of student well-being and the growing adoption of activity-based learning models. Schools are moving away from rigid seating arrangements toward flexible layouts that support group discussions, collaborative learning, and individualized teaching approaches. Manufacturers are responding with lightweight, durable, and modular designs tailored for evolving classroom needs.

Integration of Smart and Digital Learning Infrastructure

The rapid digitization of education is significantly reshaping furniture design requirements. Schools are adopting furniture integrated with charging ports, cable management systems, and mobile configurations to support digital learning devices such as tablets and laptops. Hybrid learning models and STEM-focused education programs are further driving demand for adaptable classroom setups. Smart furniture solutions are increasingly being designed to enhance mobility, connectivity, and space optimization, particularly in urban schools and technologically advanced educational institutions.

School Furniture Market Drivers

Expansion of Global Education Infrastructure

Governments across emerging and developed economies are heavily investing in expanding and upgrading educational infrastructure. Large-scale school construction projects in countries such as India, China, Indonesia, Saudi Arabia, and several African nations are generating sustained demand for classroom furniture. Additionally, modernization initiatives in North America and Europe are driving replacement cycles for outdated furniture systems. Public funding programs and education reforms continue to be key contributors to long-term market expansion.

Rising Demand for Flexible Learning Environments

Modern teaching methodologies are shifting toward collaborative and interactive learning models, requiring flexible classroom furniture solutions. Schools are increasingly adopting modular desks, foldable seating systems, and reconfigurable tables to support dynamic classroom layouts. This shift is particularly strong in STEM education environments and higher education institutions, where adaptability and space efficiency are critical. Flexible furniture solutions also enhance classroom utilization and support multi-purpose learning environments.

School Furniture Market Restraints

Volatility in Raw Material Prices

Fluctuations in the prices of wood, steel, aluminum, and plastic materials significantly impact manufacturing costs and profit margins. Supply chain disruptions and global commodity price instability create uncertainty for manufacturers, particularly those operating in price-sensitive institutional procurement markets. These cost pressures often limit the ability of manufacturers to invest in innovation and premium product development.

Price-Driven Procurement Pressure in the Public Sector

Government procurement systems in many regions prioritize cost efficiency over product innovation, leading to intense price competition among manufacturers. This environment restricts premium product adoption and limits margins for companies offering advanced ergonomic or smart furniture solutions. The dominance of low-cost bidding in public tenders remains a key challenge, especially in developing economies.

School Furniture Market Opportunities

Growth of Smart Classroom Ecosystems

The expansion of digital education infrastructure presents significant opportunities for furniture manufacturers. Increasing adoption of smart classrooms, hybrid learning systems, and STEM education programs is driving demand for technology-integrated furniture. Products such as charging-enabled desks, modular workstations, and mobile classroom units are gaining popularity. Manufacturers that integrate digital compatibility and smart functionality into furniture design are well-positioned to capture premium institutional demand.

Sustainability and Eco-Friendly Furniture Demand

Environmental sustainability is becoming a key procurement criterion for educational institutions worldwide. Schools and governments are increasingly adopting furniture made from recycled materials, low-emission laminates, and certified sustainable wood. ESG compliance and green building certifications are further accelerating demand for eco-friendly furniture solutions. Manufacturers investing in sustainable production processes and circular economy practices are expected to gain long-term institutional contracts.

Product Type Insights

Seating furniture dominates the global school furniture market with approximately 38% share in 2025, primarily driven by its universal requirement across classrooms, auditoriums, laboratories, and training spaces. The segment’s leadership is strongly supported by rising demand for ergonomic seating systems designed to improve student posture, comfort, and long-duration learning efficiency. Governments and private institutions are increasingly prioritizing student wellness, leading to large-scale replacement of traditional rigid seating with adjustable and ergonomically engineered designs. Additionally, the growing adoption of collaborative and activity-based learning models is accelerating demand for flexible seating configurations that support group learning environments.

Desks and tables represent the second-largest segment, with strong demand driven by modular classroom transformation and the shift toward digital learning environments. Storage furniture, including lockers and cabinets, continues to witness stable demand supported by infrastructure expansion in schools and universities. Technology-integrated furniture is emerging as the fastest-growing segment, driven by the rapid penetration of smart classrooms, hybrid learning models, and the increasing use of digital devices in education systems globally.

Material Type Insights

Metal-based furniture leads the market with approximately 34% share in 2025, supported by its durability, structural strength, and long lifecycle performance in high-usage educational environments. This segment benefits significantly from government procurement policies that prioritize long-term value and low maintenance costs. Steel-based classroom furniture is particularly preferred in public education systems due to its ability to withstand heavy daily use and minimal replacement requirements.

Wood-based furniture maintains strong demand in premium educational institutions where aesthetics, comfort, and traditional classroom design remain important. Plastic and composite materials are gaining momentum due to affordability, lightweight properties, and ease of mobility, especially in early education environments. Hybrid materials combining metal, wood, and recycled plastics are increasingly being adopted as institutions move toward sustainable and cost-optimized procurement strategies.

Educational Institution Insights

Primary and secondary schools account for the largest share of demand, driven by large student populations, compulsory education systems, and continuous government investments in school infrastructure development. This segment benefits from recurring procurement cycles and large-scale classroom furniture deployment programs across emerging economies.

Preschool institutions are witnessing rising demand for child-safe, colorful, and ergonomically designed furniture tailored to early learning environments. Higher education institutions are driving demand for collaborative seating systems, library infrastructure, and digitally enabled learning furniture. Vocational and technical institutes represent one of the fastest-growing segments due to increasing global investments in skill development, STEM education, and workforce training programs aligned with industrial modernization needs.

Functionality Insights

Traditional classroom furniture continues to hold a significant share; however, modular and flexible furniture systems are experiencing rapid growth due to the global shift toward interactive and student-centric learning models. Schools are increasingly redesigning classrooms to support dynamic seating arrangements and multi-purpose usage environments. Mobile and foldable furniture is gaining strong traction in urban educational institutions where space optimization is a key requirement. Inclusive furniture designed for differently-abled students is also expanding steadily, supported by regulatory frameworks and rising emphasis on accessible education infrastructure globally.

Procurement Channel Insights

Government tenders remain the dominant procurement channel, accounting for the majority of global demand, particularly across Asia-Pacific, Latin America, and Africa. Large-scale public education infrastructure programs continue to drive bulk procurement of classroom furniture.

Direct institutional procurement is significant in private schools and higher education institutions, where customization, quality differentiation, and branding play a greater role in purchasing decisions. Dealer and distributor networks remain critical in fragmented regional markets where localized supply chains dominate distribution structures. Online B2B procurement platforms are emerging rapidly due to increased transparency, competitive pricing, and simplified procurement workflows. Project-based procurement through construction contractors is also expanding, particularly in large-scale educational infrastructure development projects and smart campus initiatives.

| By Product Type | By Material Type | By Educational Institution | By Functionality | By Procurement Channel |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America accounts for approximately 31% of the global market, led by the United States and Canada. Market growth in this region is primarily driven by strong replacement demand, modernization of aging classroom infrastructure, and rapid adoption of smart classroom furniture systems. The region benefits from high education spending, advanced institutional infrastructure, and strong focus on ergonomic and sustainability-led procurement policies. Rising integration of digital learning technologies is further driving demand for technology-enabled furniture systems. Additionally, schools and universities are increasingly prioritizing flexible learning environments that support collaborative teaching models, reinforcing steady demand growth.

Asia-Pacific

Asia-Pacific dominates the global market with approximately 36% share in 2025, supported by rapid expansion of educational infrastructure across China, India, Indonesia, Vietnam, and Southeast Asia. The region is witnessing large-scale school construction projects driven by rising population, government literacy programs, and urbanization trends. Strong public investment in education infrastructure, coupled with rapid growth of private schooling systems, is a major demand driver. Asia-Pacific also serves as a global manufacturing hub, enabling cost-efficient production and large-scale exports to other regions. Increasing adoption of modern learning environments, including smart classrooms and modular learning spaces, further accelerates market expansion.

Europe

Europe accounts for approximately 22% of the global market, with strong demand from Germany, the United Kingdom, France, and Nordic countries. Growth in this region is strongly driven by strict sustainability regulations, green procurement policies, and high ergonomic standards in educational institutions. European schools are increasingly prioritizing recyclable materials, low-carbon manufacturing, and long-life furniture solutions aligned with ESG goals. Additionally, modernization of educational infrastructure and emphasis on student well-being are driving steady replacement demand. The shift toward collaborative and flexible classroom layouts is further supporting market growth across the region.

Latin America

Latin America is experiencing steady growth, led primarily by Brazil, Mexico, Chile, and Argentina. Market expansion is driven by public education modernization programs, increasing private school penetration, and rising government investments in educational infrastructure. Cost-effective and durable furniture solutions dominate procurement preferences due to budget constraints in public education systems. However, increasing awareness of ergonomic learning environments is gradually driving demand for improved classroom designs. Expansion of urban education infrastructure and international funding programs is further supporting regional market growth.

Middle East & Africa

The Middle East & Africa region is witnessing strong growth supported by large-scale education infrastructure investments in Saudi Arabia, the UAE, Qatar, and African countries such as Nigeria, Kenya, Egypt, and South Africa. Government-led education reforms and national development strategies are key growth enablers. In the Middle East, smart city initiatives and modern educational campuses are driving demand for advanced, technology-integrated furniture systems. In Africa, rising literacy programs, international funding support, and rapid school construction projects are fueling demand for basic and mid-range furniture solutions. Overall, the region is expected to remain one of the fastest-growing markets globally due to sustained infrastructure expansion and demographic growth.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the School Furniture Market

- KI (Krueger International)

- Steelcase Inc.

- MillerKnoll Inc.

- HNI Corporation

- Haworth Inc.

- Virco Manufacturing Corporation

- VS America Inc.

- Smith System Manufacturing

- Artcobell Corporation

- Fleetwood Group

- KOKUYO Co., Ltd.

- Okamura Corporation

- Godrej Interio

- Paragon Furniture Inc.

- Hertz Furniture