Salad Container Market Size

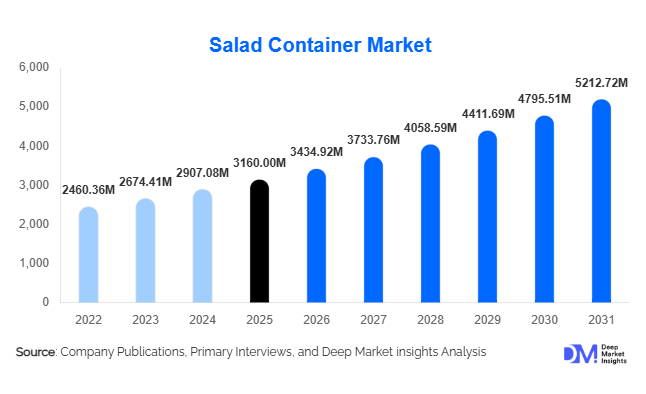

According to Deep Market Insights, the global salad container market size was valued at USD 3,160 million in 2025 and is projected to grow from USD 3,434.92 million in 2026 to reach USD 5,212.72 million by 2031, expanding at a CAGR of 8.7% during the forecast period (2026–2031). The salad container market growth is primarily driven by rising consumption of ready-to-eat meals, expanding food delivery ecosystems, and increasing adoption of sustainable food packaging solutions across retail and foodservice industries worldwide.

Key Market Insights

- Health-conscious eating trends are accelerating packaged salad consumption, directly increasing demand for convenient and durable salad containers.

- Sustainability regulations are reshaping material innovation, encouraging adoption of recyclable PET, molded fiber, and compostable packaging formats.

- Food delivery and cloud kitchen expansion is significantly increasing demand for leak-proof and transport-safe containers.

- North America dominates global demand due to high ready-to-eat food consumption and advanced cold-chain infrastructure.

- Asia-Pacific is the fastest-growing region, supported by urbanization and rapid expansion of organized retail and QSR chains.

- Technological advancements such as anti-fog lids, lightweight thermoforming, and tamper-evident packaging are improving functionality and shelf appeal.

What are the latest trends in the salad container market?

Sustainable and Compostable Packaging Adoption

Environmental regulations and corporate sustainability commitments are transforming the salad container market. Foodservice brands and retailers are transitioning toward biodegradable and recyclable materials such as molded fiber, bagasse, and recycled PET (rPET). Governments across Europe and North America are imposing restrictions on single-use plastics, encouraging manufacturers to innovate eco-friendly alternatives. Packaging companies are investing heavily in circular economy models, including closed-loop recycling systems and reduced-resin manufacturing processes. Premium sustainable containers are increasingly commanding higher price points while improving brand perception among environmentally conscious consumers.

Delivery-Optimized Packaging Design

The rapid expansion of online food delivery has changed packaging performance expectations. Salad containers must now maintain structural integrity during transport while preserving freshness and preventing leakage. Stackable designs, tamper-evident seals, and compartmental packaging for dressings are becoming standard features. Cloud kitchens and quick-service restaurants increasingly require standardized packaging formats compatible with automated fulfillment systems. Lightweight yet durable containers are reducing logistics costs while enhancing operational efficiency for large foodservice operators.

What are the key drivers in the salad container market?

Growth of Ready-to-Eat and Packaged Food Consumption

Urban lifestyles and increasing workforce participation are driving demand for convenient meal options. Packaged salads have emerged as a fast-growing category within refrigerated foods, requiring specialized containers that maintain freshness and visual appeal. Supermarkets and meal subscription providers continue expanding private-label healthy meal offerings, creating recurring packaging demand globally.

Expansion of Organized Food Retail and QSR Chains

Global expansion of supermarkets, hypermarkets, and quick-service restaurant chains is supporting standardized packaging procurement. Retailers prioritize transparent containers that enhance product visibility and reduce food waste through improved shelf-life management. Large-scale procurement contracts between packaging manufacturers and food chains are strengthening market stability and long-term revenue visibility.

What are the restraints for the global market?

Raw Material Price Volatility

Fluctuating prices of plastic resins and pulp materials significantly affect production costs. Packaging manufacturers operating under long-term supply contracts often face margin pressures when raw material prices rise sharply, limiting pricing flexibility in competitive markets.

Recycling Infrastructure Limitations

Despite increasing adoption of compostable materials, many regions lack industrial composting infrastructure. This limits effective waste processing and slows widespread adoption of biodegradable salad containers, particularly in emerging economies.

What are the key opportunities in the salad container industry?

Sustainable Packaging Innovation

Manufacturers investing in compostable materials and recyclable mono-material designs are gaining competitive advantages. Regulatory compliance and ESG commitments from global food brands are creating long-term demand for environmentally responsible packaging solutions. Companies capable of scaling sustainable production while maintaining cost competitiveness are positioned for accelerated growth.

Cloud Kitchen and Food Delivery Expansion

Cloud kitchens represent one of the fastest-growing foodservice models globally, requiring standardized and high-volume packaging supply. Salad containers designed for delivery durability and portion control are becoming essential operational components. Emerging markets across Asia-Pacific and Latin America offer strong expansion potential as online food delivery adoption rises.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3160 Million |

| Market Size in 2026 | USD 3434.92 Million |

| Market Size in 2031 | USD 5212.72 Million |

| CAGR | 8.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The product type landscape of the salad container market is strongly influenced by evolving retail merchandising strategies, convenience-oriented consumption patterns, and growing demand for freshness preservation. Clamshell salad containers continue to dominate the global market, accounting for nearly 34% of total demand. Their integrated hinged design enables secure closure, minimizes product contamination, and enhances shelf visibility through transparent construction. Retailers increasingly favor clamshell formats due to their superior stackability, optimized shelf utilization, and reduced handling time across supermarket distribution systems. The leading position of this segment is further reinforced by rising sales of ready-to-eat salads and grab-and-go meals, where packaging durability and visual product appeal play a critical role in purchase decisions.Bowl-type containers with detachable lids are witnessing steady adoption, particularly within food delivery and takeaway applications where portion customization and easy consumption are essential. The growth of digital food ordering platforms and urban lifestyles has strengthened demand for packaging formats that maintain product integrity during transportation. Compartmental containers featuring separate dressing or topping sections are expanding rapidly as consumers increasingly prioritize freshness, ingredient separation, and enhanced eating experiences. These designs help extend shelf life while supporting premium positioning for packaged salads.Reusable meal-prep containers represent an emerging growth category driven by sustainability awareness and changing dietary habits among health-conscious consumers. Subscription-based meal services, fitness-oriented food brands, and corporate meal programs are increasingly adopting durable reusable formats to reduce packaging waste and improve brand sustainability credentials. Continuous innovation in leak-resistant sealing, lightweight construction, and recyclable designs is expected to further diversify product offerings across all container formats.

Material Type Insights

Material selection plays a critical role in determining container performance, regulatory compliance, and environmental impact. Plastic containers remain the dominant material segment, accounting for approximately 58% market share in 2025, primarily due to their cost efficiency, lightweight structure, durability, and excellent transparency that enhances product visibility in retail environments. PET-based containers lead supermarket applications because they provide strong moisture barriers and extended product freshness, making them highly suitable for cold-chain distribution systems. The leading position of plastic materials is further supported by established manufacturing infrastructure and scalability advantages.At the same time, the rapid expansion of recycled PET (rPET) usage reflects increasing regulatory pressure and corporate sustainability commitments aimed at reducing virgin plastic consumption. Food brands and retailers are investing heavily in circular packaging solutions, encouraging suppliers to integrate recycled content while maintaining food safety standards.Paperboard and molded fiber containers are emerging as the fastest-growing material categories as governments and consumers push for compostable and biodegradable packaging alternatives. These materials are gaining traction particularly in regions with strict single-use plastic regulations and strong environmental awareness. Technological improvements in moisture resistance coatings and structural strength are enabling paper-based solutions to compete with conventional plastic containers.Aluminum and glass containers occupy niche yet strategically important segments focused on premium presentation, reusability, and specialty applications. These materials are commonly adopted by gourmet salad brands, high-end catering services, and eco-conscious consumers seeking long-term reusable packaging solutions, contributing to product differentiation within the market.

End-Use Insights

The end-use landscape of the salad container market is largely shaped by the rapid evolution of food consumption channels and the growing popularity of convenience-oriented dining formats. Foodservice operators and quick-service restaurants represent the largest end-use segment, contributing nearly 38% of global market demand. The leading position of this segment is primarily driven by the continued expansion of takeaway and delivery services, which require reliable, lightweight, and leak-resistant packaging capable of preserving freshness during transportation.Packaged salad manufacturers and supermarket private labels are expanding significantly as retailers strengthen their ready-meal portfolios to attract health-conscious consumers. Increasing consumer preference for fresh, minimally processed foods has encouraged supermarkets to introduce diversified salad offerings, thereby increasing demand for retail-ready containers that support extended shelf life and visual merchandising.Cloud kitchens and meal subscription services are among the fastest-growing end-use segments, supported by digital ordering ecosystems, changing urban lifestyles, and rising demand for portion-controlled healthy meals. These operators rely heavily on standardized packaging formats that ensure consistency, branding visibility, and operational efficiency. Institutional catering, corporate cafeterias, and airline food services also contribute steadily to market growth as large-scale food preparation continues to require hygienic and scalable packaging solutions.

Distribution Channel Insights

Distribution dynamics within the salad container market are characterized by strong supplier–buyer relationships and evolving procurement models. Direct B2B supply channels dominate the market with approximately 61% share, as large food processors, restaurant chains, and retail food manufacturers typically engage in long-term procurement agreements with packaging suppliers. This model ensures supply reliability, customized product specifications, and cost optimization through bulk purchasing arrangements. The leadership of this segment is primarily driven by the operational scale of multinational foodservice brands and packaged food companies that require consistent packaging quality across multiple locations.Packaging distributors play a vital role in regional supply ecosystems by serving small and medium-sized foodservice operators that lack direct sourcing capabilities. These intermediaries provide flexible order quantities, localized logistics support, and diversified product portfolios tailored to regional demand patterns.E-commerce platforms supplying packaging materials are emerging as a rapidly expanding distribution channel, particularly among startups, independent restaurants, and cloud kitchens. Online procurement enables businesses to compare specifications, manage inventory efficiently, and access standardized packaging solutions without complex supplier negotiations. The increasing digitization of procurement processes is expected to reshape distribution structures over the forecast period.

Explore more data points, trends and opportunities Download Free Sample Report

Salad Container Market Segmentations

By Material Type

- Plastic Containers

- Paper & Paperboard Containers

- Biodegradable & Compostable Containers

- Aluminum Containers

- Glass Containers

By Product Type

- Clamshell Salad Containers

- Bowl-Type Containers with Lid

- Compartmental Salad Containers

- Salad Containers with Dressing Compartments

- Reusable Meal-Prep Salad Containers

By End User

- Foodservice & QSR Chains

- Packaged Salad Manufacturers

- Retail & Supermarkets

- Cloud Kitchens & Online Food Delivery

- Household & Meal Prep Consumers

By Distribution Channel

- Direct B2B Supply

- Packaging Distributors

- E-commerce Packaging Suppliers

- Retail Consumer Sales

Regional Insights

North America

North America accounts for approximately 32% of the global salad container market, supported by mature foodservice infrastructure and high consumer adoption of ready-to-eat meals. The United States leads regional demand due to strong packaged salad consumption, widespread supermarket penetration, and one of the highest food delivery adoption rates globally. Advanced cold-chain logistics systems enable efficient distribution of fresh products, increasing reliance on high-performance packaging solutions. Sustainability initiatives from major retailers and food brands are accelerating adoption of recyclable and recycled-content containers. In Canada, regulatory efforts promoting waste reduction and compostable packaging adoption are driving innovation in molded fiber and paper-based containers. Rising health awareness and demand for fresh convenience foods continue to strengthen long-term regional growth.

Europe

Europe represents nearly 27% of global market share, with Germany, the United Kingdom, France, and the Netherlands serving as key demand centers. Regional growth is strongly driven by stringent environmental regulations targeting plastic reduction and circular economy implementation. Government policies encouraging reusable and compostable packaging are accelerating the transition toward fiber-based and recyclable container solutions. European retailers emphasize retail-ready packaging aesthetics, portion control, and sustainability labeling, which encourages continuous product innovation. Additionally, strong consumer awareness regarding environmental impact and food waste reduction supports adoption of advanced packaging formats designed to extend product shelf life.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, expanding at an estimated CAGR exceeding 10%, driven by rapid urbanization, rising disposable income levels, and evolving dietary preferences. China, India, Japan, and Australia are key contributors to regional expansion. Growth is fueled by the rapid proliferation of food delivery platforms, increasing penetration of organized retail, and expanding middle-class populations seeking convenient yet healthy meal options. India is emerging as one of the fastest-growing markets due to the rapid expansion of cloud kitchens, growth of modern supermarket chains, and increasing adoption of packaged fresh foods among urban consumers. Investments in cold-chain infrastructure and domestic packaging manufacturing capabilities further support regional market acceleration.

Latin America

Latin America demonstrates steady growth potential, led primarily by Brazil and Mexico. Regional expansion is supported by modernization of retail infrastructure, increasing supermarket penetration, and growing consumer acceptance of takeaway dining formats. Urban population growth and rising middle-class purchasing power are encouraging demand for affordable packaged food solutions, indirectly supporting salad container consumption. Improvements in logistics networks and expansion of international foodservice chains are also contributing to increasing packaging standardization across the region.

Middle East & Africa

The Middle East & Africa region is witnessing gradual but consistent market expansion, driven by economic diversification and rapid development of hospitality and tourism sectors. The UAE and Saudi Arabia serve as primary growth hubs due to expanding premium foodservice establishments, quick-service restaurant chains, and large-scale tourism initiatives. Rising expatriate populations and increasing adoption of Western-style convenience foods are strengthening demand for packaged salads and associated containers. Growth in modern retail formats, coupled with investments in food safety standards and cold storage infrastructure, continues to support long-term adoption of advanced food packaging solutions across the region.

Key Players in the Salad Container Market

- Amcor plc

- Berry Global Inc.

- Sonoco Products Company

- Genpak LLC

- Sabert Corporation

- Pactiv Evergreen Inc.

- Huhtamaki Oyj

- Dart Container Corporation

- Novolex Holdings LLC

- Greiner Packaging International

- Faerch Group

- Anchor Packaging LLC

- Reynolds Consumer Products

- WestRock Company

- Sealed Air Corporation