Rugged Computing Device Market Size

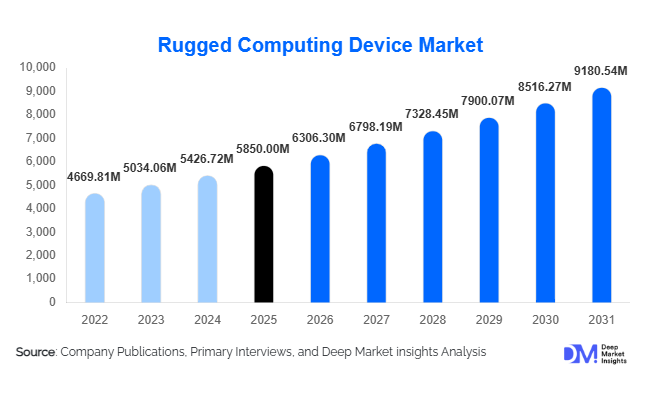

According to Deep Market Insights, the global rugged computing device market size was valued at USD 5,850 million in 2025 and is projected to grow from USD 6,306.30 million in 2026 to reach USD 9,180.54 million by 2031, expanding at a CAGR of 7.8% during the forecast period (2026–2031). The market growth is primarily driven by increasing demand for durable computing solutions in extreme environments, rapid industrial automation, and rising adoption of rugged devices across defense, logistics, and energy sectors.

Key Market Insights

- Rugged computing devices are increasingly integrated with advanced technologies such as 5G, AI, and IoT, enabling real-time data processing and enhanced operational efficiency in harsh industrial and field conditions.

- Emerging markets in Asia-Pacific and Latin America are witnessing accelerated adoption due to infrastructure development, energy sector expansion, and government-led digitalization initiatives.

- Defense & military applications dominate the market, accounting for high-value demand driven by modernization programs and mission-critical operations.

- Industrial automation and logistics sectors are the fastest-growing end-users, as rugged devices support predictive maintenance, inventory management, and real-time monitoring in challenging environments.

- North America maintains a leading market share, fueled by high defense spending, mature industrial infrastructure, and rapid adoption of connected rugged devices.

- Technological adoption is reshaping the market, with IoT-enabled rugged tablets, wearable devices, and ultra-rugged laptops improving connectivity and data-driven operations.

What are the latest trends in the rugged computing device market?

Integration of 5G and Edge Computing

Rugged computing devices are increasingly being equipped with 5G and edge computing capabilities. This allows real-time processing of critical data in remote locations such as oil rigs, mining sites, and battlefield operations. Edge computing reduces dependency on centralized servers, providing faster analytics, enhanced security, and low-latency communication. Industries including defense, energy, and transportation are leveraging these capabilities to improve operational efficiency, predictive maintenance, and situational awareness, positioning rugged devices as a cornerstone of digital transformation in mission-critical applications.

Lightweight, Portable, and Modular Designs

Manufacturers are focusing on reducing device weight while maintaining durability. Fully rugged and semi-rugged tablets and handheld devices now combine portability with robust MIL-STD-810G and IP certifications. Modular designs allow end-users to customize devices with additional modules such as barcode scanners, thermal cameras, or satellite connectivity. These innovations cater to field service teams, emergency responders, and industrial personnel who require versatile, adaptable devices for a variety of operational scenarios.

Expansion into Non-Traditional Industries

Beyond defense and industrial applications, rugged devices are gaining traction in healthcare, agriculture, and e-commerce logistics. Telemedicine and mobile diagnostic applications leverage rugged tablets for remote data capture. Precision agriculture uses handheld and wearable devices for real-time monitoring of crops and livestock. Logistics providers adopt rugged devices for last-mile delivery, inventory tracking, and fleet management. These emerging sectors expand the addressable market, creating opportunities for new entrants and product diversification.

What are the key drivers in the rugged computing device market?

Rising Defense and Military Spending

Global defense modernization programs are fueling demand for rugged computing devices. Militaries in the U.S., China, and Europe deploy these devices for navigation, communication, surveillance, and mission-critical operations. Fully rugged and ultra-rugged devices provide reliable performance in extreme environmental conditions, making them indispensable in defense applications. Rising geopolitical tensions and ongoing modernization programs are expected to sustain demand for high-performance rugged systems.

Industrial Automation and Industry 4.0 Adoption

The adoption of smart manufacturing and Industry 4.0 technologies is increasing the demand for rugged computing devices. These devices enable real-time monitoring, predictive maintenance, and automation control in manufacturing facilities. Rugged tablets and handhelds operate efficiently in environments with dust, moisture, vibrations, and high temperatures, supporting factories, warehouses, and logistics centers with uninterrupted workflow and data reliability.

Growth of Logistics and E-Commerce

The global e-commerce boom is driving demand for rugged handheld devices, tablets, and scanners in warehouses and last-mile delivery operations. Real-time inventory management, route optimization, and barcode scanning require durable devices capable of withstanding heavy usage. Logistics and supply chain operators increasingly rely on rugged devices for operational efficiency, accuracy, and reduced downtime, positioning this sector as a key market growth driver.

What are the restraints for the global market?

High Initial Cost of Rugged Devices

Rugged devices are significantly more expensive than consumer-grade devices due to specialized materials, engineering, and certifications such as MIL-STD-810 and IP ratings. This high upfront cost can deter small and medium enterprises from adopting rugged devices despite their operational advantages.

Limited Customization and Bulky Designs

Some rugged devices remain bulky, affecting portability and user comfort. Limited customization for specific industry applications can restrict adoption, especially in sectors that require lightweight or highly specialized equipment for field operations.

What are the key opportunities in the rugged computing device industry?

Emerging Markets and Infrastructure Development

Emerging economies such as India, Brazil, and Indonesia are experiencing rapid industrialization and infrastructure expansion. Public investment in smart city projects, digitalization of public safety, and utility management drives demand for rugged computing devices. Manufacturers entering these markets can capitalize on cost-sensitive yet high-growth opportunities through localized production and strategic partnerships with government agencies and private enterprises.

Technological Advancements and IoT Integration

Integration of IoT, AI, and 5G into rugged computing devices creates new opportunities for product differentiation. Devices with advanced sensors, cloud connectivity, and predictive analytics enable industries to optimize workflows, reduce operational downtime, and improve safety. Early adoption of these technologies can provide a competitive edge and expand the addressable market in both traditional and emerging sectors.

Expansion into Non-Traditional End-Use Industries

Rugged devices are being increasingly adopted in healthcare, agriculture, retail, and e-commerce logistics. Mobile diagnostics, precision farming, and last-mile delivery applications are rapidly increasing. These sectors not only provide new revenue streams but also enhance device utilization rates, enabling manufacturers to diversify portfolios and target previously untapped industries.

Product Type Insights

Rugged tablets dominate the global rugged computing device market, accounting for approximately 32% of the total market share in 2025. Their leadership is primarily driven by their optimal balance between portability, performance, and durability. Unlike traditional rugged laptops, tablets offer lightweight form factors combined with touchscreen functionality, making them highly suitable for field-based operations such as logistics tracking, utility inspections, and defense mobility. The increasing integration of 5G connectivity, GPS, and IoT-enabled sensors into rugged tablets further enhances their real-time data processing capabilities, making them indispensable in digital field operations.

Rugged laptops and notebooks continue to hold a significant share, particularly in industries requiring high computing power, such as defense command systems, industrial diagnostics, and engineering applications. Meanwhile, rugged handheld devices are widely used in logistics and warehouse management for barcode scanning and inventory tracking. Wearable rugged devices, including smart glasses and wrist-mounted computers, represent a smaller but rapidly expanding segment, driven by hands-free operations, augmented reality (AR) integration, and increasing adoption in field services and remote assistance applications.

Application Insights

Defense and military applications remain the largest segment, contributing approximately 28% of the market share in 2025. This dominance is driven by the critical need for highly reliable computing devices capable of operating in extreme environmental conditions, including combat zones, high-altitude terrains, and marine environments. Continuous modernization programs, increased deployment of connected battlefield systems, and rising geopolitical tensions are further strengthening demand. Industrial automation and manufacturing represent one of the fastest-growing application areas, supported by the global shift toward Industry 4.0. Rugged devices enable real-time monitoring of machinery, predictive maintenance, and seamless communication across production lines. In the logistics and transportation sector, rugged handhelds and tablets are essential for warehouse automation, fleet management, and last-mile delivery optimization, especially with the rapid expansion of e-commerce.

The energy & utilities sector is also witnessing significant adoption, particularly in remote asset monitoring and maintenance of power grids and oil & gas infrastructure. Additionally, emerging applications in healthcare (mobile diagnostics), agriculture (precision farming), and retail logistics are expanding the market’s scope, creating new revenue streams and diversifying demand across industries.

Distribution Channel Insights

Direct sales dominate the rugged computing device market, accounting for approximately 60% of total revenue in 2025. This dominance is largely due to large-scale procurement by government agencies, defense organizations, and enterprise clients, which prefer direct engagement with manufacturers for customized solutions, long-term contracts, and after-sales support. Direct channels also enable better integration of hardware with enterprise systems and ensure compliance with stringent operational standards. System integrators play a critical role in deploying rugged devices within complex industrial and defense ecosystems. They provide tailored solutions, combining hardware, software, and connectivity to meet specific operational requirements. Value-added resellers further enhance market penetration by offering bundled solutions, maintenance services, and localized support.

Online and digital sales channels are gradually gaining traction, particularly in commercial sectors such as logistics, field services, and small enterprises. These platforms offer pricing transparency, product comparison, and faster procurement cycles, making them attractive for non-government buyers. The rise of e-commerce and digital procurement platforms is expected to further strengthen this channel over the forecast period.

End-User Insights

The defense and military sector continues to be the largest end-user of rugged computing devices, driven by high capital expenditure on advanced communication systems, battlefield management solutions, and mission-critical computing infrastructure. However, the fastest-growing end-user segments are logistics and industrial automation, supported by the rapid expansion of global supply chains and increasing adoption of smart manufacturing technologies. The logistics sector, in particular, is experiencing strong growth due to the rise of e-commerce and the need for real-time tracking, route optimization, and warehouse automation. Industrial automation is benefiting from the increasing implementation of IoT-enabled systems, where rugged devices act as key interfaces for monitoring and controlling operations in harsh environments.

Emerging end-user industries such as healthcare, agriculture, and retail are also contributing to market expansion. In healthcare, rugged tablets are used for mobile diagnostics and patient data management. In agriculture, they support precision farming and equipment monitoring. Export-driven demand is especially strong in the Asia-Pacific region, where manufacturing hubs rely on rugged devices to maintain operational efficiency and meet global supply chain requirements.

| By Product Type | By Application | By Distribution Channel |

|---|---|---|

|

|

|

Regional Insights

North America

North America holds the largest share of the rugged computing device market, accounting for approximately 35% of global revenue in 2025, with the United States leading regional demand. Growth in this region is primarily driven by high defense spending, continuous military modernization programs, and strong adoption of advanced technologies such as IoT, AI, and 5G. The presence of major industry players and a well-established industrial base further supports market expansion.

Additionally, the region’s advanced logistics infrastructure and rapid adoption of warehouse automation are fueling demand for rugged handheld devices and tablets. Government contracts, particularly in defense and public safety sectors, provide long-term revenue stability. Increasing investments in smart manufacturing and energy infrastructure are also contributing to sustained growth.

Europe

Europe accounts for approximately 25% of the global market, with Germany, the United Kingdom, and France serving as key contributors. The region’s growth is largely driven by strong industrial automation in Germany, ongoing defense modernization in the UK and France, and increasing adoption of rugged devices in transportation and logistics. Stringent regulatory standards related to worker safety and equipment reliability are encouraging the adoption of rugged devices across industries. Additionally, Europe’s focus on sustainability and energy efficiency is driving demand for eco-friendly rugged devices in utilities and renewable energy sectors. The expansion of smart factories and digital supply chains is further accelerating market growth.

Asia-Pacific

Asia-Pacific is the fastest-growing region in the rugged computing device market, with a projected CAGR of approximately 9.5% during the forecast period. The region accounts for around 28% of the global market share in 2025, led by China, India, Japan, and South Korea. Growth is primarily driven by rapid industrialization, expanding manufacturing activities, and large-scale infrastructure projects. China dominates due to its strong manufacturing ecosystem and export-oriented production, while India is witnessing accelerated demand supported by government initiatives such as “Make in India” and increasing investments in defense and infrastructure.

The expansion of e-commerce and logistics networks across the region is also driving the adoption of rugged handheld devices. Additionally, rising investments in mining, energy, and telecommunications infrastructure are creating strong demand for rugged computing solutions in remote and challenging environments.

Middle East & Africa

The Middle East & Africa region accounts for approximately 7% of the global market, with demand primarily concentrated in countries such as Saudi Arabia, the UAE, and South Africa. The region’s growth is driven by extensive oil & gas exploration activities, mining operations, and large-scale infrastructure development projects. Rugged computing devices are essential for field operations in extreme environmental conditions, including high temperatures and desert terrains. Government-led diversification initiatives, such as Saudi Arabia’s Vision 2031, are also promoting industrial and technological development, thereby increasing demand for rugged devices. Additionally, investments in smart cities and utilities infrastructure are expected to further boost market growth.

Latin America

Latin America holds approximately 5% of the global market share, with Brazil and Mexico emerging as key markets. Growth in the region is driven by mining, oil & gas, and logistics sectors, which require durable computing solutions for field operations. The expansion of industrial activities and the increasing adoption of digital technologies in supply chain management are supporting market growth. Additionally, the rise of export-oriented manufacturing and infrastructure development projects is creating new opportunities for rugged device adoption. While the market is still in a developing stage, improving economic conditions and foreign investments are expected to drive steady growth over the forecast period.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Rugged Computing Device Market

- Panasonic Corporation

- Zebra Technologies Corporation

- Getac Technology Corporation

- Dell Technologies Inc.

- Honeywell International Inc.

- Trimble Inc.

- Advantech Co., Ltd.

- Winmate Inc.

- MilDef Group AB

- DT Research Inc.

- Estone Technology

- Juniper Systems Inc.

- Handheld Group AB

- Kontron AG

- Xplore Technologies Inc.