Ruby Market Size

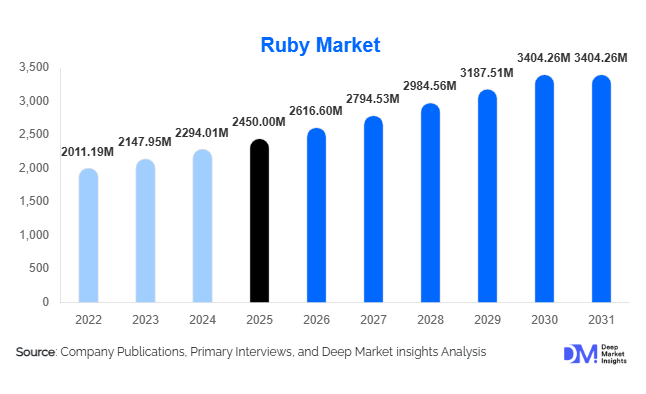

According to Deep Market Insights, the global ruby market size was valued at USD 2,450 million in 2025 and is projected to grow from USD 2,616.60 million in 2026 to reach USD 3,635.75 million by 2031, expanding at a CAGR of 6.8% during the forecast period (2026–2031). The ruby market growth is primarily driven by increasing demand for luxury jewelry, rising investment interest in high-value gemstones, and expanding applications of synthetic rubies in industrial and technological sectors.

Key Market Insights

- Jewelry remains the dominant application, accounting for nearly 68% of total market revenue, driven by luxury consumption and cultural significance.

- Natural, untreated rubies command premium pricing, contributing significantly to market value despite limited supply.

- Asia-Pacific dominates the global market, holding approximately 48% share, led by China, India, and Thailand.

- Lab-grown rubies are rapidly gaining traction, offering cost-effective and ethically sourced alternatives.

- Offline retail channels continue to lead, contributing around 60% of sales due to trust and physical verification needs.

- Industrial applications are emerging steadily, particularly in lasers, electronics, and aerospace technologies.

What are the latest trends in the ruby market?

Growing Adoption of Lab-Grown Rubies

The increasing adoption of lab-grown rubies is one of the most significant trends shaping the market. These stones offer consistent quality, lower pricing, and ethical sourcing advantages, making them highly appealing to younger consumers and mid-range jewelry buyers. Technological advancements in crystal growth methods have enabled manufacturers to produce high-quality synthetic rubies suitable not only for jewelry but also for industrial applications such as lasers and optical instruments. This trend is also helping stabilize supply constraints associated with natural rubies, thereby expanding overall market accessibility.

Rising Demand for Investment-Grade Gemstones

Rubies are increasingly being viewed as alternative investment assets, particularly untreated, high-quality stones with verified origin. High-net-worth individuals and collectors are allocating capital toward gemstones as a hedge against inflation and market volatility. Auction houses and private dealers are witnessing increased participation, with record-breaking prices for rare rubies reinforcing their investment appeal. This trend is expected to strengthen as global wealth increases and diversification strategies evolve.

What are the key drivers in the Ruby market?

Expanding Luxury Jewelry Demand

The growth of the global luxury goods market is a primary driver of ruby demand. Consumers are increasingly shifting toward colored gemstones as a means of personalization and exclusivity. Rubies, known for their rarity and symbolism, are particularly favored in high-end jewelry collections. Markets in Asia-Pacific and the Middle East are witnessing strong growth due to rising disposable incomes and cultural affinity for gemstones.

Technological Advancements in Synthetic Ruby Production

Advancements in lab-grown ruby production technologies have significantly improved quality while reducing manufacturing costs. This has enabled broader adoption across both jewelry and industrial sectors. Synthetic rubies are now widely used in lasers, electronics, and precision instruments, driving incremental demand beyond traditional applications.

What are the restraints for the global market?

Supply Constraints of Natural Rubies

The supply of natural rubies is highly concentrated in regions such as Myanmar, Mozambique, and Madagascar. Political instability, mining restrictions, and limited reserves create supply volatility, which impacts pricing and availability. These challenges restrict consistent market growth and create dependency on a few geographic sources.

Lack of Standardization and Certification

The ruby market suffers from inconsistent grading and certification standards across regions. Variations in quality assessment, treatment disclosure, and origin verification reduce transparency and can affect consumer confidence. This lack of uniformity poses challenges for global trade and pricing consistency.

What are the key opportunities in the Ruby market?

Expansion in Emerging Luxury Markets

Emerging economies such as India, China, Vietnam, and the UAE present significant growth opportunities due to rising disposable incomes and increasing luxury consumption. Cultural significance attached to gemstones, particularly in Asia, enhances demand for rubies in jewelry and investment segments. Market participants can leverage localized designs and digital retail strategies to capture this growing demand.

Integration into High-Tech Industrial Applications

Rubies are gaining importance in advanced industrial applications, including lasers, medical devices, and aerospace technologies. Their hardness, thermal stability, and optical properties make them ideal for precision instruments. Increased R&D investments in synthetic ruby applications are expected to unlock new high-margin opportunities in these sectors.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2450 Million |

| Market Size in 2026 | USD 2616.60 Million |

| Market Size in 2031 | USD 3635.75 Million |

| CAGR | 6.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Natural, untreated rubies continue to dominate the product type segment, accounting for approximately 38% of the global market share in 2025. This leadership is primarily driven by their rarity, superior color saturation (often referred to as “pigeon blood red”), and strong investment appeal among high-net-worth individuals. The limited supply from key mining regions such as Myanmar and Mozambique further strengthens their premium positioning, leading to sustained price appreciation and demand in auctions and luxury retail. In contrast, heat-treated and fracture-filled rubies serve the mid-tier segment by enhancing clarity and visual appeal at relatively accessible price points, making them popular among aspirational buyers. Meanwhile, synthetic (lab-grown) rubies are emerging as the fastest-growing sub-segment due to their scalability, cost efficiency, and ethical sourcing advantages. Their adoption is particularly strong in industrial applications and entry-level jewelry, where affordability and consistency are critical. Over the forecast period, synthetic rubies are expected to gain incremental share as technology improves and consumer acceptance rises.

Application Insights

The jewelry segment dominates the application landscape, contributing nearly 68% of total market revenue in 2025. This dominance is driven by strong global demand for luxury adornments, especially in Asia-Pacific and the Middle East, where rubies hold deep cultural and symbolic significance associated with prosperity and power. High-end jewelry brands continue to prioritize natural rubies for flagship collections, reinforcing this segment’s leadership. The watchmaking segment remains a stable contributor, particularly in Switzerland, where rubies are used as bearings in luxury mechanical watches due to their durability and low-friction properties. Industrial applications, including lasers, optical instruments, and electronic substrates, are gaining traction as synthetic ruby production becomes more advanced and cost-effective. Additionally, the investment and collectibles segment, although niche, commands high value, driven by increasing interest in alternative assets and record-breaking auction sales of rare stones. The growing diversification of applications is enhancing overall market resilience.

Distribution Channel Insights

Offline retail channels lead the ruby market, accounting for approximately 60% of global sales in 2025. The dominance of this segment is largely attributed to the high-value nature of ruby purchases, where consumers prefer physical verification, certification checks, and personalized consultation before making a purchase. Established jewelry stores, auction houses, and trade exhibitions continue to serve as primary sales channels, particularly for premium and investment-grade stones. However, online channels are witnessing rapid growth, driven by increasing digitalization, improved transparency in gemstone certification, and the expansion of direct-to-consumer (D2C) business models. E-commerce platforms are leveraging advanced visualization tools, blockchain-based traceability, and competitive pricing to attract younger, tech-savvy consumers. Over time, the integration of omnichannel strategies is expected to redefine distribution dynamics, with online platforms gradually capturing a larger share of mid-range and standardized ruby sales.

End-Use Industry Insights

The luxury and fashion industry dominates end-use demand, contributing approximately 70% of the global ruby market in 2025. This leadership is driven by rising global affluence, evolving fashion preferences, and increasing demand for high-value, statement jewelry pieces. Premium brands are continuously innovating designs and incorporating rare gemstones to differentiate their offerings. The electronics and semiconductor industry is emerging as the fastest-growing end-use segment, fueled by the use of synthetic rubies in laser technologies, LED substrates, and precision instruments. This segment is benefiting from advancements in material science and increasing demand for high-performance components. Aerospace and defense applications are also expanding, leveraging ruby’s hardness and thermal stability in specialized equipment. Additionally, export-driven demand plays a critical role, with countries such as Thailand and India acting as global processing and re-export hubs. Their strong cutting, polishing, and trading ecosystems enable efficient global distribution, further supporting market growth.

Explore more data points, trends and opportunities Download Free Sample Report

Ruby Market Segmentations

By Product Type

- Natural Ruby

- Heat-Treated Ruby

- Fracture-Filled Ruby

- Synthetic Ruby

By Application

- Jewelry

- Watchmaking

- Industrial Applications

- Investment & Collectibles

By Distribution Channel

- Offline Retail

- Online Retail

By End-Use Industry

- Luxury & Fashion Industry

- Electronics & Semiconductor Industry

- Aerospace & Defense

- Investment/Wealth Management

Regional Insights

Asia-Pacific

Asia-Pacific leads the global ruby market with approximately 48% market share in 2025, making it the largest and fastest-growing regional market with a CAGR of around 7.5%. Growth in this region is primarily driven by strong cultural affinity for gemstones, particularly in China and India, where rubies symbolize wealth, prosperity, and status. Rising disposable incomes, expanding middle-class populations, and increasing penetration of luxury retail are further accelerating demand. Thailand plays a strategic role as a global trading and processing hub, supported by its well-established gemstone cutting and export infrastructure. Additionally, growing digital adoption and e-commerce penetration are enhancing accessibility, further boosting regional growth.

North America

North America accounts for approximately 20% of the global ruby market, led by the United States. The region’s growth is driven by strong demand for luxury goods, increasing interest in alternative investments, and a mature retail ecosystem. High-net-worth individuals are increasingly investing in rare gemstones as part of diversified portfolios, while auction houses and premium jewelry brands continue to drive high-value transactions. Furthermore, the presence of well-established certification bodies and transparent trade practices enhances consumer confidence, supporting steady market expansion.

Europe

Europe holds around 18% market share, with key markets including Switzerland, France, the UK, and Italy. The region’s demand is strongly supported by its globally renowned luxury watchmaking and jewelry industries. Switzerland, in particular, drives demand through its high-end watch sector, where rubies are used as functional components. Additionally, European consumers exhibit a strong preference for certified, ethically sourced gemstones, aligning with the region’s stringent regulatory standards. The growing focus on sustainability and traceability is further shaping purchasing decisions and driving premiumization in the market.

Middle East & Africa

The Middle East & Africa region accounts for approximately 8% of the global market. Demand in the Middle East, particularly in the UAE and Saudi Arabia, is driven by high luxury spending, strong cultural inclination toward precious gemstones, and a thriving retail sector catering to affluent consumers and tourists. Africa, on the other hand, plays a dual role as both a supply and demand center. Countries such as Mozambique and Madagascar are key sources of ruby mining, contributing significantly to the global supply. Increasing investments in mining infrastructure and government efforts to formalize gemstone trade are supporting regional growth.

Latin America

Latin America represents approximately 6% of the global ruby market, with Brazil being a key contributor. Market growth in this region is driven by rising interest in luxury goods, gradual expansion of the affluent consumer base, and increasing awareness of gemstones as investment assets. While still an emerging market, improving retail infrastructure and growing participation in the global gemstone trade are expected to support steady demand growth. Additionally, regional players are increasingly engaging in export activities, contributing to broader market integration.

Key Players in the Ruby Market

- Gemfields Group

- Fura Gems

- Greenland Ruby

- True North Gems

- Bangkok Ruby Co.

- Chatham Created Gems

- Swarovski Gemstones

- KGK Group

- Titan Company

- Chow Tai Fook Jewellery

- Luk Fook Holdings

- Richemont Group

- Tiffany & Co.

- Harry Winston

- Bvlgari