Rubber Bands Market Size

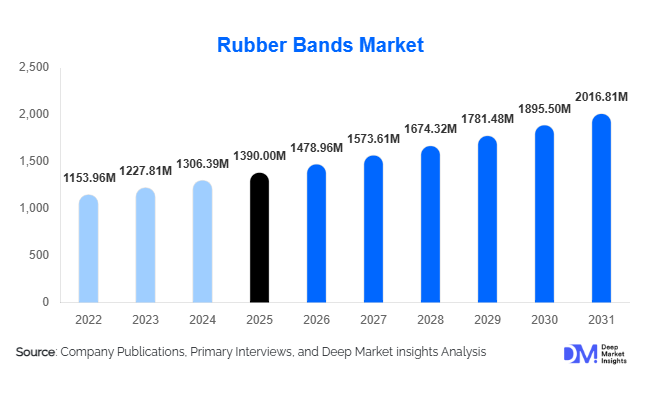

According to Deep Market Insights, the global rubber bands market size was valued at USD 1,390 million in 2025 and is projected to grow from USD 1,478.96 million in 2026 to reach USD 2,016.81 million by 2031, expanding at a CAGR of 6.4% during the forecast period (2026–2031). Market growth is primarily supported by expanding global logistics activities, rising agricultural exports, and increasing demand for cost-efficient bundling solutions across packaging, manufacturing, and retail sectors. Rubber bands continue to remain indispensable fastening products due to their flexibility, low cost, reusability, and compatibility across manual and semi-automated packaging environments.

Key Market Insights

- Packaging and logistics applications dominate global consumption, accounting for nearly half of total rubber band demand due to expanding e-commerce fulfillment operations.

- Natural rubber bands lead material adoption, driven by biodegradability advantages and sustainability-focused procurement policies.

- Asia-Pacific dominates global production and consumption, supported by large manufacturing bases and agriculture exports.

- Eco-friendly and recycled rubber bands are emerging premium segments as environmental regulations tighten worldwide.

- Direct B2B procurement channels are expanding, with logistics firms and agricultural exporters signing bulk supply contracts.

- Automation-compatible specialty rubber bands are gaining traction in warehouses and industrial assembly operations.

What are the latest trends in the rubber bands market?

Sustainability and Biodegradable Material Adoption

Manufacturers are increasingly transitioning toward environmentally sustainable rubber band production using certified natural rubber and recycled elastomers. Corporate sustainability mandates and regulatory pressure, particularly in Europe and North America, are encouraging adoption of biodegradable alternatives to synthetic fastening products. Companies are investing in low-emission manufacturing processes and recyclable packaging to align with ESG requirements. This shift allows suppliers to command premium pricing while improving brand positioning among environmentally conscious buyers, including food processors and retail chains.

Industrial Customization and Specialty Applications

Demand is shifting beyond standard office rubber bands toward specialty variants designed for industrial and agricultural uses. Heat-resistant, UV-stabilized, anti-static, and food-grade rubber bands are gaining popularity across manufacturing, floriculture, and food packaging industries. Custom sizing for automated sorting systems and warehouse bundling applications is becoming a major differentiator. Manufacturers are also offering color-coded bands for inventory management and logistics tracking, reflecting increasing operational sophistication among end users.

What are the key drivers in the rubber bands market?

Expansion of Global Logistics and E-commerce Infrastructure

The rapid expansion of global e-commerce has significantly increased secondary packaging and bundling requirements. Warehouses, courier hubs, and fulfillment centers rely heavily on flexible fastening solutions for organizing parcels and documentation. Rubber bands provide a reusable and low-cost alternative compared to adhesive tapes or plastic fasteners, ensuring sustained consumption growth aligned with logistics sector expansion.

Growth in Agricultural and Floriculture Exports

Rubber bands play a critical role in agriculture for plant grafting, produce bundling, and flower packaging. Rising exports of fruits, vegetables, and flowers from Asia-Pacific and Latin America are strengthening demand. Agricultural producers prefer rubber bands due to elasticity and minimal product damage compared with rigid fastening materials, reinforcing consistent seasonal consumption patterns.

What are the restraints for the global market?

Volatility in Natural Rubber Prices

Raw material cost fluctuations remain a major challenge for manufacturers. Weather disruptions, plantation output variability, and global commodity price swings directly influence production costs. Sudden price increases reduce margins for suppliers operating in highly price-sensitive markets.

Substitution by Automated Fastening Technologies

Highly automated manufacturing environments increasingly use cable ties, shrink wrapping, and adhesive systems. While rubber bands remain essential in flexible applications, automation-driven substitutions may limit adoption in certain advanced industrial facilities.

What are the key opportunities in the rubber bands industry?

Sustainable Product Innovation

The introduction of biodegradable and recycled rubber bands presents a major opportunity for manufacturers. Retailers and food companies increasingly prefer environmentally responsible packaging accessories. Companies investing in green product lines can benefit from long-term contracts and higher margins, particularly in developed markets where sustainability compliance is mandatory.

Emerging Market Logistics Expansion

Rapid urbanization and infrastructure development across India, Southeast Asia, and Latin America are creating new demand centers. Expanding warehouse networks and export-oriented manufacturing clusters require large volumes of low-cost bundling materials. New entrants targeting regional logistics hubs can secure scalable growth opportunities through bulk supply agreements.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1390 Million |

| Market Size in 2026 | USD 1478.96 Million |

| Market Size in 2031 | USD 2016.81 Million |

| CAGR | 6.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Standard office rubber bands continue to dominate the global market, accounting for nearly 34% of total demand, primarily due to their widespread and recurring usage across offices, banks, educational institutions, and government organizations. The leading position of this segment is driven by its cost efficiency, versatility, and compatibility with routine administrative and document management activities. Increasing institutional procurement contracts and the continued need for simple, reusable fastening solutions support stable long-term demand. Additionally, the transition toward organized documentation practices in emerging economies further reinforces adoption across administrative environments.Heavy-duty rubber bands are gaining significant traction in industrial and logistics applications where superior tensile strength and durability are essential. Growth in this category is largely supported by expanding e-commerce fulfillment operations and automated packaging facilities that require flexible yet reliable bundling solutions.

Specialty rubber bands, including UV-resistant, anti-static, and temperature-resistant variants, represent the fastest-growing product category as industries increasingly demand application-specific products capable of performing under specialized environmental conditions. The rising adoption of electronics manufacturing and outdoor storage applications continues to accelerate innovation in this segment.Food-grade rubber bands are witnessing expanding adoption within fresh produce packaging and food retail distribution, supported by tightening hygiene regulations and growing consumer awareness regarding food safety standards. Meanwhile, agricultural rubber bands are experiencing strong growth due to increasing use in floriculture, greenhouse cultivation, and crop management practices. Expansion of commercial farming and controlled-environment agriculture globally is strengthening demand for durable yet flexible plant-support solutions, positioning agricultural variants as an important future growth contributor.

Application Insights

Bundling and packaging applications represent the largest share of the rubber bands market, contributing approximately 46% of total consumption. The leadership of this segment is driven by rapid expansion of global logistics networks, rising parcel shipment volumes, and increasing reliance on low-cost reusable fastening solutions within warehouses and distribution centers. Rubber bands provide operational flexibility compared to adhesive-based packaging, enabling quick sorting, grouping, and repackaging activities across supply chains. Growth in last-mile delivery and cross-border trade continues to strengthen demand from logistics providers and packaging service companies.Industrial assembly applications are expanding steadily as manufacturers adopt temporary fastening solutions during component alignment, inspection, and staging processes. Rubber bands offer efficiency advantages in lean manufacturing environments where reusable materials help reduce operational waste. Agricultural applications, including crop tying, plant grafting, and nursery management, are growing rapidly alongside global horticulture exports and rising demand for high-value crops. Increasing adoption of greenhouse farming techniques further supports this application segment.Household and DIY applications remain stable contributors to market demand, supported by strong consumer familiarity, affordability, and multi-purpose usability. Growth in home organization trends and small-scale craft activities continues to sustain steady consumption levels, particularly through retail and online sales channels.

Distribution Channel Insights

Direct B2B sales dominate the distribution landscape, accounting for nearly 39% of global revenue, as industrial buyers and logistics companies typically procure rubber bands in bulk quantities through long-term supply agreements. The leading position of this channel is supported by predictable consumption patterns, cost advantages associated with bulk purchasing, and supplier customization capabilities tailored to industrial requirements. Large enterprises increasingly prioritize supplier reliability and standardized product quality, reinforcing direct procurement models.Industrial distributors and wholesale packaging suppliers continue to play a critical role in servicing small and medium-sized enterprises that require flexible order volumes and rapid delivery timelines. These intermediaries help bridge supply gaps by maintaining regional inventories and offering product variety. Meanwhile, e-commerce platforms are rapidly gaining importance by enabling small businesses and independent buyers to access industrial-grade rubber bands with improved pricing transparency and convenient delivery options.Office supply retailers maintain consistent demand through institutional procurement contracts and recurring purchases from educational and administrative organizations. Digital marketplaces are increasingly influencing purchasing decisions by enabling product comparison, customization selection, and subscription-based procurement models, which are gradually reshaping traditional distribution dynamics.

End-Use Industry Insights

The logistics and packaging industry represents the largest end-use segment, accounting for nearly 28% market share. Segment leadership is primarily driven by accelerating global parcel shipments, warehouse automation, and expanding e-commerce ecosystems that require efficient, reusable bundling solutions. Rubber bands provide operational convenience for sorting, labeling, and temporary packaging tasks, making them essential consumables within distribution centers and fulfillment hubs.Agriculture and horticulture are among the fastest-growing end-use industries, supported by rising fresh produce exports, expansion of greenhouse farming, and increasing adoption of modern cultivation practices. Rubber bands are widely utilized for plant support, crop organization, and harvesting operations, contributing to improved productivity and crop quality management.The food and beverage sector continues to expand its use of food-grade rubber bands for retail packaging and produce bundling applications, particularly as food safety regulations become more stringent across developed markets. Healthcare and pharmaceutical logistics are emerging as important application areas, where reusable bundling solutions improve inventory organization, streamline handling processes, and contribute to packaging waste reduction initiatives aligned with sustainability goals.

Explore more data points, trends and opportunities Download Free Sample Report

Rubber Bands Market Segmentations

By Material Type

- Natural Rubber Bands

- Synthetic Rubber Bands

- Recycled Rubber Bands

By Product Type

- Standard Office Rubber Bands

- Heavy-Duty Rubber Bands

- Specialty Rubber Bands

- Food-Grade Rubber Bands

- Agricultural Rubber Bands

By Application

- Bundling & Packaging

- Industrial Assembly & Manufacturing

- Agriculture & Floriculture

- Office & Stationery Use

- Logistics & Warehousing

- Food Processing & Retail Packaging

- Household & DIY Applications

By Distribution Channel

- Direct B2B Sales

- Industrial Distributors

- Office Supply Retailers

- E-commerce Platforms

- Wholesale Packaging Suppliers

By End-Use Industry

- Logistics & Packaging Industry

- Agriculture & Horticulture

- Manufacturing & Automotive

- Food & Beverage Industry

- Offices & Educational Institutions

- Retail & Consumer Goods

- Healthcare & Pharmaceuticals

Regional Insights

Asia-Pacific

Asia-Pacific leads the global rubber bands market with approximately 38% share in 2025, supported by strong manufacturing ecosystems, expanding export activities, and rapidly developing logistics infrastructure. China remains the largest producer and consumer due to its extensive industrial base and dominant role in global packaging supply chains. India is experiencing robust demand growth driven by rising agricultural exports, expanding organized retail networks, and significant investments in warehousing and transportation infrastructure. Southeast Asian countries such as Vietnam and Indonesia are emerging as manufacturing hubs benefiting from supply chain diversification, increasing regional production capacity and consumption simultaneously. The presence of cost-effective labor, growing SME manufacturing activity, and rising e-commerce penetration further strengthen regional market expansion.

North America

North America accounts for nearly 24% of global demand, led primarily by the United States, where advanced warehousing systems and highly organized procurement structures support consistent consumption. Growth in the region is driven by strong e-commerce penetration, automation within fulfillment centers, and increasing adoption of sustainable packaging materials. Corporations are increasingly prioritizing environmentally responsible procurement strategies, encouraging the use of recyclable and eco-friendly rubber bands. Additionally, stable institutional demand from offices, healthcare logistics, and educational sectors continues to provide market resilience.

Europe

Europe represents around 22% market share, with Germany, France, and the United Kingdom acting as major demand centers. Regional growth is strongly influenced by strict environmental regulations encouraging biodegradable and sustainably sourced rubber products. The presence of advanced packaging industries and structured recycling initiatives supports product innovation across the region. Agricultural exports from Spain and the Netherlands sustain consistent consumption, particularly in fresh produce packaging and greenhouse cultivation applications. Increasing focus on circular economy practices further drives adoption of reusable fastening solutions.

Latin America

Latin America demonstrates steady market growth led by Brazil and Mexico, where expanding agricultural exports and regional manufacturing activities are increasing demand for packaging and crop-management solutions. Growth in food processing industries and improvements in logistics infrastructure are supporting higher rubber band consumption across distribution networks. Rising participation in international trade and modernization of supply chains are gradually strengthening regional market opportunities.

Middle East & Africa

The Middle East and Africa market is expanding gradually, supported by growing agricultural exports in countries such as Kenya and South Africa and rapidly developing retail logistics sectors in the UAE and Saudi Arabia. Investments in infrastructure development, warehousing facilities, and trade corridors are improving packaging supply chains across the region. Increasing adoption of modern farming practices and rising import-export activities are further contributing to steady demand growth, while expanding retail distribution networks continue to create new consumption avenues.

Key Players in the Rubber Bands Market

- Alliance Rubber Company

- H.B. Fuller Company

- ACCO Brands Corporation

- Rainbow Rubber & Plastics

- Elastrator USA

- Yong Sheng Rubber Industrial

- Shree Rubber Works

- Anji Wande Rubber Products

- Suremark Industries

- Mid-West Rubber Products

- Hubei Xinbin Rubber

- Thai Rubber Latex Group

- British Elastic Bands Ltd.

- Staples Inc.

- Lee Rubber Company