Rose Wine Market Size

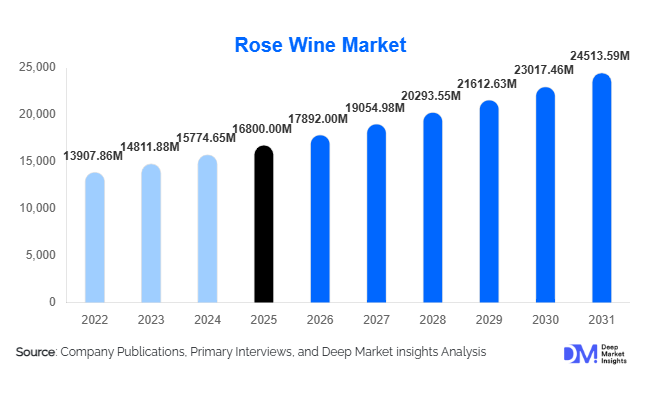

According to Deep Market Insights, the global rose wine market size was valued at USD 16,800 million in 2025 and is projected to grow from USD 17,892.00 million in 2026 to reach USD 24,513.59 million by 2031, expanding at a CAGR of 6.5% during the forecast period (2026–2031). The rose wine market growth is primarily driven by increasing consumer preference for lighter alcoholic beverages, rising demand for aesthetically appealing and versatile wines, and the growing influence of lifestyle-driven consumption trends across both developed and emerging markets.

Key Market Insights

- Rose wine consumption is shifting toward premium and lifestyle-driven categories, with strong appeal among millennials and Gen Z consumers globally.

- Europe dominates global production and consumption, particularly led by France, which sets quality and branding benchmarks.

- Off-trade distribution channels lead the market, driven by supermarket penetration and rapid growth in e-commerce wine sales.

- Asia-Pacific is the fastest-growing region, supported by rising disposable incomes and increasing adoption of wine culture.

- Innovative packaging formats, such as canned rose and bag-in-box solutions, are gaining traction among younger and convenience-driven consumers.

- Sustainability and organic wine production are emerging as key differentiators, influencing purchasing decisions globally.

What are the latest trends in the rose wine market?

Premiumization and Craft Rose Expansion

The rose wine market is witnessing a strong shift toward premiumization, with consumers increasingly opting for high-quality, region-specific, and limited-edition rose wines. Producers are focusing on vineyard-specific expressions, organic cultivation, and artisanal production methods to cater to evolving consumer preferences. This trend is particularly prominent in North America and Europe, where consumers are willing to pay premium prices for authenticity and superior taste profiles. Boutique wineries and heritage brands are leveraging storytelling and terroir-driven marketing to differentiate their offerings. Additionally, premium rose wines are increasingly featured in fine dining establishments and luxury hospitality settings, further enhancing their aspirational value and market positioning.

Rise of Alternative Packaging Formats

Innovative packaging formats are transforming the rose wine market, with canned rose, bag-in-box solutions, and lightweight bottles gaining popularity. These formats cater to convenience-oriented consumers and outdoor consumption occasions such as picnics, festivals, and travel. Canned rose, in particular, is resonating with younger demographics due to its portability and modern branding. At the same time, sustainability concerns are driving the adoption of recyclable and eco-friendly packaging materials. Producers are investing in packaging innovations that reduce carbon footprint while maintaining product quality, aligning with global sustainability trends and regulatory expectations.

What are the key drivers in the rose wine market?

Shift Toward Light and Low-Alcohol Beverages

Changing consumer preferences toward lighter and lower-alcohol beverages are significantly driving the rose wine market. Rose wines typically offer moderate alcohol content and a refreshing taste profile, making them an attractive alternative to heavier red wines and high-alcohol spirits. Health-conscious consumers are increasingly moderating alcohol consumption, favoring beverages that align with balanced lifestyles. This trend is particularly strong among younger demographics, who prioritize wellness and moderation without compromising on social experiences. The growing availability of low-alcohol and alcohol-free rose variants is further expanding the consumer base.

Expansion of E-commerce and Direct-to-Consumer Channels

The rapid growth of online retail and direct-to-consumer (D2C) channels has enhanced accessibility to rose wines globally. Consumers can now explore a wide range of brands, compare prices, and access detailed product information through digital platforms. Subscription-based wine services and curated online marketplaces are further driving engagement and repeat purchases. This digital transformation has enabled smaller producers to reach international markets without relying heavily on traditional distribution networks. The convenience of home delivery and increasing digital adoption are expected to sustain this growth momentum.

What are the restraints for the global market?

Seasonal Demand Fluctuations

The rose wine market is characterized by strong seasonality, with peak consumption during summer months and outdoor social events. This seasonal demand pattern creates challenges in inventory management, production planning, and revenue consistency for producers and distributors. Off-season demand tends to decline, particularly in colder regions, limiting year-round growth potential. While marketing strategies and product diversification are helping to mitigate this issue, seasonality remains a structural constraint affecting overall market stability.

Price Sensitivity in Emerging Markets

Price sensitivity among consumers in emerging markets poses a restraint to the growth of premium rose wine segments. While demand is increasing in regions such as Asia-Pacific and Latin America, many consumers prefer lower-priced alcoholic beverages due to income constraints. This limits the adoption of high-margin premium products and creates competitive pressure on pricing strategies. Producers must balance affordability with quality to penetrate these markets effectively, often requiring localized production and pricing models.

What are the key opportunities in the rose wine industry?

Expansion into Emerging Markets

Emerging economies such as China, India, and Brazil present significant growth opportunities for the rose wine market. Rising disposable incomes, urbanization, and increasing exposure to global consumption trends are driving demand for wine in these regions. Rose wine, with its approachable taste and visual appeal, is particularly well-suited for first-time wine consumers. Companies investing in localized marketing, distribution networks, and consumer education are likely to gain a competitive advantage in these high-growth markets.

Sustainable and Eco-Friendly Production

Sustainability is becoming a critical factor influencing purchasing decisions in the rose wine market. Consumers are increasingly seeking environmentally responsible products, prompting producers to adopt organic farming practices, reduce carbon emissions, and implement sustainable packaging solutions. Certifications and eco-labels are gaining importance, helping brands build trust and differentiate themselves in a competitive market. Investments in sustainable production not only enhance brand reputation but also align with regulatory requirements and long-term industry goals.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 16800 Million |

| Market Size in 2026 | USD 17892 Million |

| Market Size in 2031 | USD 24513.59 Million |

| CAGR | 6.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Direct press rose dominates the global market, accounting for approximately 48% of the total market share in 2025. This segment leads primarily due to its lighter hue, crisp acidity, and delicate flavor profile, which aligns strongly with evolving global consumer preferences for refreshing and easy-to-drink wines. The production method allows for better control over color and aroma, making it highly preferred by premium producers, particularly in regions such as France and the United States. Additionally, the strong association of direct press rose with premium appellations like Provence has elevated its global positioning. The segment’s growth is further driven by rising demand for visually appealing wines that perform well in social settings and digital marketing platforms. Saignee rose, while holding a comparatively smaller share, benefits from its richer structure and is often positioned within premium and artisanal categories. Blended rose continues to gain traction in cost-sensitive and emerging markets due to its flexibility in production and pricing, making it accessible to entry-level consumers. However, the dominance of direct press rose reflects a broader industry shift toward quality-driven, premium, and lifestyle-oriented wine consumption.

Application Insights

Dry rose wines lead the global market, contributing approximately 55% of total revenue in 2025. This dominance is driven by a significant global shift toward low-sugar and health-conscious beverage consumption. Consumers, particularly in Europe and North America, increasingly prefer dry wines due to their perceived health benefits, balanced taste, and compatibility with a wide range of cuisines. The segment is further supported by strong institutional demand from restaurants and fine dining establishments, where dry rose is favored for its versatility in food pairing. Additionally, regulatory and labeling trends emphasizing reduced sugar content have indirectly supported the growth of this segment. Semi-dry and sweet rose wines continue to cater to niche consumer bases, particularly in Asia-Pacific and Latin America, where sweeter flavor profiles are traditionally more accepted. However, the overall trend indicates a gradual shift toward drier variants globally, reinforcing the leadership of this segment.

Distribution Channel Insights

Off-trade channels dominate the rose wine market, accounting for nearly 65% of global sales. This segment’s leadership is driven by the increasing preference for at-home consumption, supported by the widespread availability of rose wines across supermarkets, hypermarkets, and online retail platforms. Competitive pricing, product variety, and promotional strategies further enhance the attractiveness of off-trade channels. The rapid expansion of e-commerce and direct-to-consumer (D2C) models has been a critical growth driver, enabling producers to bypass intermediaries and engage directly with consumers. Subscription-based wine services and digital marketing campaigns have also contributed to higher customer retention and repeat purchases. On-trade channels, including restaurants, bars, and hotels, remain essential for premium brand positioning and experiential consumption. These channels play a crucial role in introducing new products and influencing consumer preferences through curated wine lists and sommelier recommendations. However, the structural shift toward convenience and digital purchasing continues to favor off-trade dominance.

Packaging Format Insights

Glass bottles remain the dominant packaging format, representing approximately 70% of the market share in 2025. This dominance is driven by their strong association with quality, heritage, and premium positioning, as well as their ability to preserve the integrity and aging potential of wine. Glass packaging is particularly preferred in high-end retail and hospitality channels, where presentation and brand perception are critical. However, alternative packaging formats such as cans and bag-in-box solutions are witnessing rapid growth, driven by changing consumer lifestyles and sustainability concerns. Canned rose is gaining popularity among younger consumers due to its portability, single-serve convenience, and suitability for outdoor and casual consumption occasions. Bag-in-box formats are also expanding in off-trade channels due to their cost efficiency and reduced environmental impact. These emerging formats are expected to gradually capture a larger share, particularly in developed markets focused on sustainability and convenience.

End-Use Insights

Household consumption remains a primary driver of rose wine demand, supported by the increasing trend of at-home drinking and the growing accessibility of wines through online platforms. Consumers are increasingly incorporating rose wine into everyday occasions, including casual meals and social gatherings. The hospitality sector continues to play a significant role, particularly in urban centers and tourist destinations, where rose wine is widely featured in restaurants, bars, and hotels. Notably, casual dining and social events represent the fastest-growing end-use segment, driven by the beverage’s versatility, visual appeal, and alignment with lifestyle trends. Additionally, the emergence of wine-based cocktails and ready-to-drink (RTD) rose beverages is expanding the application scope of rose wine. These innovations are attracting younger consumers and creating new consumption occasions, further accelerating market growth.

Explore more data points, trends and opportunities Download Free Sample Report

Rose Wine Market Segmentations

By Product Type

- Direct Press Rose

- Saignee Rose

- Blended Rose

By Sweetness Level

- Dry Rose

- Semi-Dry Rose

- Sweet Rose

By Price Range

- Economy (Below USD 10)

- Mid-Range (USD 10–25)

- Premium (USD 25–50)

- Luxury (Above USD 50)

By Distribution Channel

- On-Trade

- Off-Trade

By Packaging Format

- Glass Bottles

- Cans

- Bag-in-Box

- Tetra Packs

Regional Insights

Europe

Europe dominates the global rose wine market, accounting for approximately 45% of total revenue in 2025, with France, Spain, and Italy leading production and consumption. France alone represents a significant portion of global rose output, particularly from the Provence region, which sets international quality benchmarks. The region’s growth is driven by deeply rooted wine culture, high per capita consumption, and strong domestic demand. Additionally, well-established vineyard infrastructure, favorable climatic conditions, and government support for wine exports contribute to sustained market leadership. Increasing demand for premium and organic rose wines, along with strong tourism-driven consumption, further strengthens Europe’s position.

North America

North America accounts for around 25% of the global market share, led by the United States. The region’s growth is fueled by evolving lifestyle trends, strong consumer inclination toward premium and imported wines, and the influence of social media-driven branding. Rose wine has become a popular seasonal and lifestyle beverage, particularly among millennials. The expansion of domestic wineries, especially in California, and the rapid growth of e-commerce platforms have significantly improved product accessibility. Additionally, the rise of wine tourism and experiential consumption in the U.S. continues to drive demand across both on-trade and off-trade channels.

Asia-Pacific

Asia-Pacific is the fastest-growing region, with a projected CAGR exceeding 8% during the forecast period. Countries such as China, India, Japan, and Australia are witnessing increasing demand due to rising disposable incomes, urbanization, and growing exposure to Western consumption patterns. The expanding middle-class population and increasing adoption of wine as a social and aspirational beverage are key growth drivers. Additionally, government initiatives supporting domestic wine production in countries like China and India, along with the expansion of modern retail and e-commerce channels, are accelerating market penetration. The region’s relatively low base consumption also provides significant headroom for growth.

Latin America

Latin America is experiencing steady growth, led by Brazil, Argentina, and Chile. The region’s expansion is driven by improving economic conditions, rising consumer awareness, and increasing interest in wine consumption among younger demographics. The growth of organized retail and the availability of imported rose wines are enhancing market accessibility. Additionally, domestic wine production in countries like Argentina and Chile supports regional supply, while tourism and hospitality sectors contribute to on-trade demand. The gradual shift from traditional alcoholic beverages to wine is expected to sustain long-term growth in this region.

Middle East & Africa

The Middle East & Africa region represents an emerging market for rose wine, with growth concentrated in urban and tourism-driven economies such as the UAE and South Africa. Increasing investments in hospitality and tourism infrastructure, particularly in the UAE, are driving demand for premium alcoholic beverages. South Africa, as a major wine producer, contributes both to domestic consumption and exports. Additionally, rising expatriate populations, changing lifestyle preferences, and the expansion of luxury dining establishments are supporting market growth. However, regulatory restrictions on alcohol consumption in certain countries remain a limiting factor, influencing the pace of market expansion.

Key Players in the Rose Wine Market

- E. & J. Gallo Winery

- Constellation Brands

- The Wine Group

- Pernod Ricard

- Treasury Wine Estates

- Castel Group

- Jackson Family Wines

- Trinchero Family Estates

- Accolade Wines

- Baron Philippe de Rothschild

- Domaines Ott

- Château d'Esclans

- Familia Torres

- Masi Agricola

- Banfi Vintners