Roller Shutter Market Size

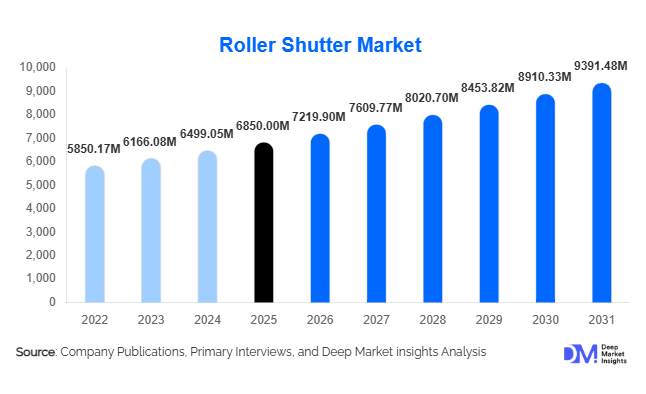

According to Deep Market Insights, the global roller shutter market size was valued at USD 6,850 million in 2025 and is projected to grow from USD 7,219.90 million in 2026 to reach USD 9,391.48 million by 2031, expanding at a CAGR of 5.4% during the forecast period (2026–2031). The roller shutter market growth is primarily driven by increasing infrastructure development, rising demand for commercial and industrial security solutions, and the growing adoption of automated and insulated shutter systems across residential and warehouse applications.

Key Market Insights

- Motorized and smart roller shutters are gaining significant traction, driven by automation trends and integration with building management systems.

- Steel roller shutters dominate material demand, accounting for nearly half of total installations due to durability and cost-efficiency.

- Asia-Pacific leads the global market, supported by rapid industrialization and urban construction growth in China and India.

- Industrial and logistics infrastructure expansion is the fastest-growing end-use segment globally.

- Energy-efficient insulated shutters are witnessing rising demand, particularly in Europe and North America, due to regulatory compliance.

- Direct sales and project-based procurement dominate distribution, especially in large commercial and industrial installations.

What are the latest trends in the roller shutter market?

Automation and Smart Integration

The integration of roller shutters with IoT-enabled building automation systems is accelerating. Smart shutters with remote access, programmable scheduling, weather sensors, and security alerts are increasingly preferred in commercial offices, retail spaces, and premium residential properties. Mobile app-controlled shutters and voice-enabled systems are enhancing user convenience. Manufacturers are incorporating tubular motor technologies with centralized control capabilities, enabling energy management and real-time monitoring across multiple installations.

Rising Demand for Insulated and Energy-Efficient Shutters

Energy efficiency regulations are pushing demand for insulated composite roller shutters, especially in Europe and North America. Foam-filled aluminum shutters are helping reduce HVAC energy consumption in warehouses, cold storage units, and residential properties. Industrial users are adopting high-speed insulated shutters for temperature-sensitive environments, reinforcing their role in operational efficiency and sustainability initiatives.

What are the key drivers in the roller shutter market?

Expansion of Warehousing and Logistics Infrastructure

The rapid growth of e-commerce has led to a surge in warehouse and distribution center construction globally. Industrial-grade steel roller shutters are essential for loading docks, storage facilities, and logistics hubs. This structural shift toward large-scale distribution infrastructure is significantly contributing to sustained market demand.

Growing Security Concerns Across Commercial Establishments

Retail stores, banks, malls, and commercial properties increasingly rely on roller shutters to prevent vandalism and unauthorized access. Transparent polycarbonate shutters are gaining popularity in retail spaces as they combine security with visibility, maintaining storefront display aesthetics while enhancing protection.

What are the restraints for the global market?

Raw Material Price Volatility

Fluctuations in steel and aluminum prices significantly affect manufacturing costs and profit margins. Global supply chain disruptions and geopolitical tensions further amplify pricing uncertainties, creating procurement and planning challenges for manufacturers.

High Cost of Advanced Automated Systems

Motorized and smart roller shutters can cost 30–50% more than manual systems, limiting penetration in price-sensitive regions. Initial installation and maintenance expenses may slow adoption in emerging economies.

What are the key opportunities in the roller shutter industry?

Smart Cities and Infrastructure Modernization

Government-led smart city initiatives and urban modernization programs are creating demand for automated security systems, including integrated roller shutters. Infrastructure expansion in the Asia-Pacific and the Middle East presents substantial opportunities for suppliers capable of delivering large-scale project solutions.

Retrofit and Energy-Efficiency Upgrades

Retrofitting older commercial and residential buildings with insulated and automated shutters offers long-term growth opportunities. Energy savings and enhanced building performance are encouraging property owners to upgrade legacy systems, particularly in Europe.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 6850 Million |

| Market Size in 2026 | USD 7219.90 Million |

| Market Size in 2031 | USD 9391.48 Million |

| CAGR | 5.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Electric (motorized) roller shutters lead the global market, accounting for approximately 42% of total revenue in 2025. The primary driver behind this dominance is the accelerating shift toward automation across commercial, industrial, and high-end residential infrastructure. Growing adoption of building management systems (BMS), smart warehouses, and automated retail outlets has significantly increased demand for tubular motor-driven shutters. In logistics hubs and high-frequency operational environments, motorized shutters improve efficiency, reduce manual labor dependency, and enhance safety compliance, making them the preferred choice. Furthermore, integration with remote controls, centralized monitoring, and IoT-based platforms strengthens their value proposition.

Manual shutters continue to maintain relevance in cost-sensitive markets across parts of Asia, Africa, and Latin America, particularly in small retail shops and standalone establishments. However, the fastest-growing sub-segment is smart/IoT-integrated shutters, driven by smart home adoption, energy management systems, and increasing demand for connected security infrastructure. As automation costs gradually decline, motorized shutters are expected to widen their market lead.

Material Insights

Steel roller shutters dominate the material segment, holding nearly 48% of the global market in 2025. Their leadership is driven by high structural strength, impact resistance, and suitability for heavy-duty industrial and warehouse applications. The global expansion of logistics parks, manufacturing units, and export-processing zones has reinforced demand for galvanized and stainless steel shutters capable of withstanding high operational cycles and harsh environmental conditions. Additionally, steel remains cost-competitive for large industrial door installations, further supporting its widespread adoption.

Aluminum shutters are particularly strong in residential and commercial window applications due to their corrosion resistance and lightweight properties. Insulated composite shutters are witnessing rising demand in Europe and North America, supported by energy-efficiency regulations and climate control requirements in cold storage and temperature-sensitive facilities. Thermal insulation performance and noise reduction capabilities are key growth enablers in this sub-segment.

Application Insights

Door applications represent the largest application segment, accounting for approximately 63% of overall demand in 2025. The leading driver for this dominance is the surge in warehouse construction, organized retail expansion, and industrial unit development globally. Warehouse doors, shopfront shutters, garage doors, and distribution center entrances require high-durability security solutions, making roller shutters a standard installation component. Rapid e-commerce penetration and last-mile delivery infrastructure development are further amplifying demand for high-speed industrial doors.

Industrial openings, including loading bays, aircraft hangars, and cold storage facilities, are the fastest-growing application areas. The growth of temperature-controlled logistics and food processing industries is significantly driving adoption in these specialized environments.

End-Use Industry Insights

The commercial segment leads the market with approximately 36% share in 2025. The primary driver for this leadership is the expansion of organized retail chains, shopping malls, hospitality establishments, and office complexes requiring standardized security installations. Retail security concerns and storefront protection continue to generate stable demand across developed and emerging markets.

The industrial segment is the fastest-growing end-use category, expanding at over 6% annually. Growth is driven by export-oriented manufacturing, factory automation, and logistics infrastructure investments across Asia-Pacific and North America. Increasing foreign direct investments (FDI) into manufacturing hubs are directly translating into shutter installations for new facilities. Residential demand is steadily increasing, particularly in premium housing and gated communities where automated shutters are adopted for enhanced safety and energy efficiency.

Distribution Channel Insights

Direct sales dominate the distribution landscape, accounting for approximately 44% of total revenue. This leadership is primarily driven by large-scale commercial and industrial projects that require customized, bulk procurement directly from manufacturers. Direct engagement allows for technical customization, installation support, and compliance with regional building standards. OEM supply plays a critical role in integrated construction and prefabricated building systems. Meanwhile, dealer and distributor networks remain essential for residential and small commercial sales, particularly in fragmented regional markets. E-commerce platforms are gradually emerging as a niche channel for standardized residential shutter systems.

Explore more data points, trends and opportunities Download Free Sample Report

Roller Shutter Market Segmentations

By Product Type

- Manual Roller Shutters

- Electric (Motorized) Roller Shutters

- Smart/Automated Roller Shutters

By Material Type

- Steel Roller Shutters

- Aluminum Roller Shutters

- Polycarbonate Roller Shutters

- Insulated Composite Roller Shutters

By Application

- Doors

- Windows

- Industrial Openings

By End-Use Industry

- Residential

- Commercial

- Industrial

- Institutional

By Distribution Channel

- Direct Sales

- OEM Supply

- Dealer/Distributor Network

- E-commerce Platforms

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global roller shutter market with approximately 38% share in 2025, making it the largest regional contributor. The region’s growth is primarily driven by rapid industrialization, urban housing expansion, and strong government-led infrastructure investments. China leads regional demand due to large-scale manufacturing capacity and logistics infrastructure development. India is the fastest-growing country in the region, expanding at over 7% CAGR, fueled by industrial corridor projects, warehousing expansion, and smart city initiatives. Southeast Asian nations such as Vietnam and Indonesia are witnessing rising adoption due to increasing FDI inflows and retail modernization. Lower manufacturing costs in the region also support strong domestic production and exports.

Europe

Europe accounts for nearly 27% of global revenue, driven by stringent building energy-efficiency regulations and strong retrofit demand. Countries such as Germany, France, Italy, and the UK lead regional consumption. Germany alone contributes nearly 23% of Europe’s market due to its robust industrial base and high adoption of insulated and automated shutter systems. The primary growth driver in Europe is regulatory compliance related to energy conservation and building performance standards. Retrofitting aging commercial and residential infrastructure further sustains steady demand.

North America

North America holds approximately 21% of the global market, led predominantly by the United States. The region’s growth is supported by rapid warehouse construction linked to e-commerce growth, rising security investments in retail properties, and increasing automation adoption across industrial facilities. Demand for high-speed insulated shutters in cold storage and pharmaceutical logistics is also strengthening. Canada contributes steady growth driven by commercial property upgrades and energy-efficiency initiatives.

Middle East & Africa

The Middle East & Africa region represents around 8% of global demand. Growth is driven by large-scale infrastructure projects, commercial real estate expansion, and industrial diversification programs in countries such as Saudi Arabia and the UAE. Mega construction projects, logistics hubs, and retail complexes are key demand generators. In Africa, urbanization and retail modernization in countries like South Africa and Nigeria are gradually increasing adoption.

Latin America

Latin America accounts for approximately 6% of global revenue, with Brazil and Mexico leading regional demand. Growth is supported by retail sector modernization, expanding industrial production, and infrastructure upgrades. Increasing investments in logistics and cross-border trade facilities are further driving installations in warehouses and distribution centers. However, economic volatility remains a moderate growth constraint in the region.

Key Players in the Roller Shutter Market

- ASSA ABLOY

- Hörmann Group

- Alutech Group

- Sanwa Holdings Corporation

- Janus International Group

- Heroal

- CornellCookson

- Novoferm

- Somfy

- Rite-Hite

- Gliderol Garage Doors

- B&D Australia

- TNR Doors

- Chase Doors

- SKB Shutters