Reusable Water Bottles Market Size

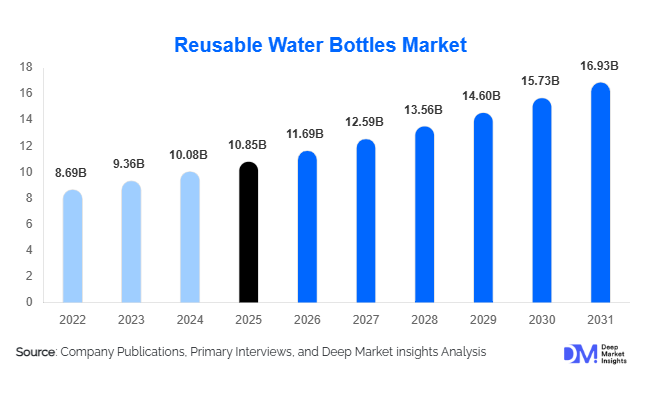

According to Deep Market Insights, the global reusable water bottles market was valued at approximately USD 10.85 billion in 2025 and is projected to grow from USD 11.69 billion in 2026 to reach nearly USD 16.93 billion by 2031, expanding at a CAGR of 7.7% during the forecast period (2026–2031). The market growth is primarily driven by rising environmental concerns regarding single-use plastics, increasing consumer adoption of sustainable lifestyle products, and the rapid expansion of fitness, wellness, and outdoor recreational activities globally. Growing corporate ESG initiatives and government-led plastic reduction regulations are further accelerating demand for reusable hydration solutions across both developed and emerging economies.

Key Market Insights

- Stainless steel insulated bottles dominate premium demand due to durability, thermal retention, and strong lifestyle branding appeal among urban consumers.

- Sustainability regulations and plastic bans are accelerating adoption, particularly across Europe and North America where institutional usage is rising.

- Asia-Pacific is the fastest-growing regional market, driven by urbanization, rising middle-class income, and e-commerce expansion in China and India.

- Online retail channels are rapidly expanding, enabling global D2C brands and niche manufacturers to scale internationally.

- Smart water bottles are emerging as a high-growth niche, integrating hydration tracking, UV sterilization, and app-based wellness monitoring.

- Corporate and institutional procurement is increasing as organizations adopt reusable bottles to support ESG and zero-waste initiatives.

- Fitness, wellness, and outdoor activity trends are driving everyday consumption, making reusable bottles a mainstream lifestyle product rather than a niche accessory.

Reusable Water Bottles Market Trends

Premiumization and Lifestyle Branding of Bottles

The reusable water bottles market is witnessing strong premiumization, with stainless steel insulated bottles evolving into lifestyle accessories. Consumers increasingly associate brands with fitness identity, sustainability values, and personal aesthetics. High-end products featuring advanced insulation, matte finishes, customizable designs, and leak-proof technology are gaining traction. Brands are investing heavily in influencer marketing and social media positioning, particularly on wellness and fitness platforms. This shift has increased average selling prices and strengthened brand loyalty, especially in North America and Europe where consumers prioritize design and performance over cost.

Technology Integration and Smart Hydration Ecosystems

Smart hydration technology is emerging as a transformative trend in the reusable water bottles market. Products equipped with hydration tracking sensors, UV-C sterilization, temperature displays, and mobile app connectivity are gaining popularity among tech-savvy consumers. These innovations are increasingly integrated with wearable health ecosystems, enabling users to monitor daily hydration levels. AI-based reminders and personalized hydration recommendations are also being developed. While currently a niche segment, smart bottles are expected to grow rapidly as wellness technology adoption expands globally, particularly among urban professionals and fitness enthusiasts.

Reusable Water Bottles Market Drivers

Rising Environmental Awareness and Plastic Reduction Policies

One of the strongest drivers of market growth is increasing global awareness of plastic pollution and environmental sustainability. Governments are actively implementing bans and taxes on single-use plastics, pushing both consumers and businesses toward reusable alternatives. Educational campaigns and corporate sustainability commitments are reinforcing behavioral change. Public infrastructure investments in water refill stations are also supporting adoption. As environmental responsibility becomes a core purchasing factor, reusable water bottles are increasingly viewed as essential daily-use products rather than optional accessories.

Expanding Fitness, Wellness, and Outdoor Lifestyle Culture

The global rise in fitness participation, gym memberships, and outdoor recreational activities is significantly driving demand for reusable water bottles. Consumers engaged in sports, travel, hiking, and wellness activities prefer durable, insulated hydration solutions. The wellness movement, supported by social media influencers and health-conscious branding, has further normalized regular hydration habits. This has expanded demand across all age groups, particularly among millennials and Gen Z consumers who prioritize health-oriented lifestyles.

Reusable Water Bottles Market Restraints

Price Sensitivity in Developing Markets

Despite strong global demand, price sensitivity remains a key barrier in developing economies. Premium stainless steel and smart bottles are significantly more expensive than disposable or low-cost plastic alternatives. This limits adoption in lower-income consumer segments, particularly in rural and semi-urban regions. Although awareness is increasing, affordability constraints continue to slow penetration rates in emerging markets across Asia, Africa, and Latin America.

Intense Market Competition and Product Commoditization

The market is highly fragmented with numerous global and regional players offering similar product designs and features. This has led to strong price competition, particularly in mid-range and basic plastic bottle segments. Low differentiation among standard products puts pressure on margins and increases reliance on branding and marketing. Additionally, counterfeit products and low-quality imitations in online marketplaces negatively impact brand trust and pricing stability.

Reusable Water Bottles Market Opportunities

Expansion in Emerging Economies and Urban Consumption Growth

Rapid urbanization and rising disposable income in emerging economies such as India, Indonesia, Vietnam, Brazil, and parts of Africa present a significant growth opportunity. Expanding e-commerce penetration and modern retail infrastructure are improving product accessibility. Increasing awareness of health and environmental issues is driving adoption of reusable bottles in schools, offices, and households. Companies that offer affordable, durable, and locally adapted designs are well-positioned to capture large untapped demand.

Corporate Sustainability and Institutional Procurement Demand

Corporate ESG initiatives and institutional sustainability programs are creating strong B2B opportunities. Companies are increasingly distributing branded reusable bottles to employees as part of zero-waste policies. Educational institutions, hospitality chains, airlines, and event organizers are also shifting away from disposable bottles. This large-scale institutional adoption creates stable, recurring demand and long-term procurement contracts for manufacturers, significantly expanding market potential beyond individual consumers.

Product Type Insights

Insulated water bottles dominate the global reusable water bottles market due to their superior thermal performance and widespread use across fitness, travel, and workplace applications. Stainless steel insulated bottles alone account for nearly 48% of the total market, driven by premium consumer demand and long product lifecycle. Smart bottles are the fastest-growing category, supported by rising wellness technology integration and digital health monitoring trends. Sports and squeeze bottles remain popular among athletes and fitness users due to convenience and portability. Collapsible and travel bottles are gaining traction in outdoor and tourism segments, particularly among frequent travelers and hikers. Meanwhile, filtered and infuser bottles are expanding within health-conscious consumer groups seeking enhanced hydration experiences.

Application Insights

Daily hydration remains the largest application segment, accounting for nearly half of global demand as reusable bottles become a standard household and workplace essential. Sports and fitness applications are growing rapidly due to increasing gym participation and outdoor activities. Corporate gifting and branding applications are also expanding as companies use reusable bottles in sustainability campaigns. Travel and tourism represent a growing niche, with demand for lightweight and durable bottles suitable for long journeys. Educational institutions are increasingly adopting reusable bottles to reduce plastic usage among students, further expanding the application base globally.

Distribution Channel Insights

Online retail is the fastest-growing distribution channel, contributing a significant share of global revenue due to the expansion of e-commerce platforms and direct-to-consumer brands. Consumers increasingly prefer online channels for product variety, customization options, and competitive pricing. Offline retail, including supermarkets, specialty stores, and sporting goods outlets, continues to play a major role in product discovery and impulse purchases. Institutional procurement channels are growing steadily as organizations implement sustainability policies. Brand-owned websites and subscription models are also gaining traction, enabling stronger customer engagement and repeat purchases.

End-User Insights

Individual consumers represent the largest end-user segment, driven by widespread adoption across fitness, education, commuting, and travel lifestyles. Corporate and institutional users are emerging as a fast-growing segment due to ESG commitments and sustainability initiatives. Hospitality and tourism industries are increasingly adopting reusable bottles to replace disposable alternatives in hotels, resorts, and airlines. Industrial and outdoor workforce users also contribute to demand, particularly in construction, logistics, and mining sectors where durable hydration solutions are essential for field operations.

| By Material Type | By Product Type | By Distribution Channel | By End User | By Application |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America holds approximately 32% of the global reusable water bottles market in 2025, making it the largest regional market. The United States dominates demand due to strong sustainability awareness, high disposable income, and a mature fitness culture. Canada is also experiencing steady growth, supported by government initiatives promoting plastic reduction. Premium insulated bottles and branded lifestyle products are particularly popular across the region, with strong adoption in workplaces, gyms, and outdoor recreation activities.

Europe

Europe accounts for nearly 28% of global market share, driven by strict environmental regulations and circular economy initiatives. Countries such as Germany, the UK, France, and the Netherlands lead demand due to strong consumer preference for sustainable products. European consumers show high acceptance of eco-friendly and reusable alternatives, supported by widespread plastic bans and recycling policies. Premium and design-oriented bottles are particularly popular in urban centers across Western Europe.

Asia-Pacific

Asia-Pacific is the fastest-growing region, accounting for approximately 27% of the global market. China dominates both production and consumption, while India is experiencing rapid growth driven by urbanization and e-commerce expansion. Japan and South Korea contribute to premium and technology-enabled bottle demand. Southeast Asian countries are witnessing rising adoption due to environmental awareness campaigns and tourism-driven demand. Increasing middle-class income levels and rapid retail expansion are key growth drivers in the region.

Latin America

Latin America is an emerging market led by Brazil and Mexico. Growing health awareness and expanding retail infrastructure are driving gradual adoption of reusable bottles. Although still smaller in size compared to other regions, increasing urbanization and sustainability awareness are expected to support long-term growth. Adventure and sports-related applications are particularly popular in this region.

Middle East & Africa

The Middle East & Africa region is witnessing steady growth led by the UAE, Saudi Arabia, and South Africa. High temperatures, increasing tourism, and sustainability initiatives are driving demand for reusable hydration products. The UAE is emerging as a premium market for lifestyle and branded bottles, while African countries are gradually adopting reusable solutions through government-led environmental programs and institutional adoption.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Reusable Water Bottles Market

- Hydro Flask

- YETI Holdings

- CamelBak

- SIGG

- Thermos

- Klean Kanteen

- S'well

- Contigo