Retail Furniture Market Size

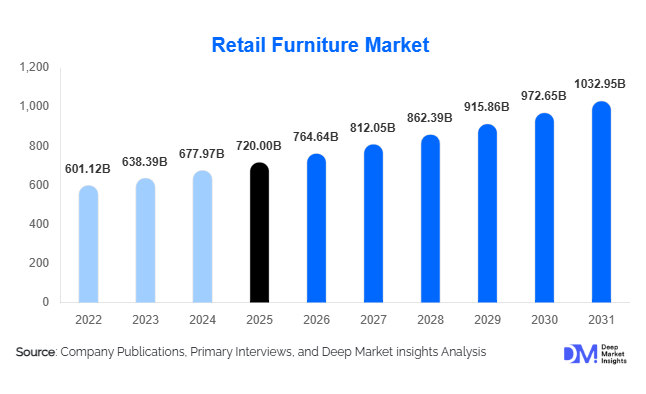

According to Deep Market Insights, the global retail furniture market size was valued at USD 720 billion in 2025 and is projected to grow from USD 764.64 billion in 2026 to reach USD 1,032.95 billion by 2031, expanding at a CAGR of 6.2% during the forecast period (2026–2031). The retail furniture market growth is primarily driven by rapid urbanization, increasing residential construction, and rising consumer preference for aesthetically appealing and multifunctional furniture. The expansion of e-commerce platforms and omnichannel retail strategies is further accelerating market penetration globally.

Key Market Insights

- Residential furniture dominates global demand, accounting for nearly 70% of total market share due to increasing housing and renovation activities.

- Asia-Pacific leads the global market, supported by strong manufacturing capabilities and rising middle-class consumption in China and India.

- Online furniture retail is rapidly expanding, expected to exceed 30% market share by 2031, with growing digital adoption.

- Sustainable and eco-friendly furniture is gaining traction, driven by regulatory frameworks and consumer awareness.

- The mid-range furniture segment dominates pricing categories, capturing nearly 50% of total demand globally.

- Technological integration, including AR-based visualization and smart furniture, is transforming customer experience and purchase behavior.

What are the latest trends in the retail furniture market?

Shift Toward Modular and Space-Saving Furniture

Urban living spaces are shrinking, particularly in densely populated cities across Asia and Europe, leading to increased demand for modular and multifunctional furniture. Consumers are prioritizing space efficiency, driving the adoption of foldable beds, extendable tables, and storage-integrated sofas. Ready-to-assemble (RTA) furniture has gained significant traction due to affordability, ease of transport, and customization flexibility. This trend is particularly strong among younger demographics and urban renters who seek flexible living solutions.

Digital Transformation and Omnichannel Retail

The integration of digital tools is reshaping the furniture-buying journey. Augmented reality (AR) applications allow customers to visualize furniture within their homes before purchase, reducing return rates and improving satisfaction. E-commerce platforms are offering detailed product comparisons, customer reviews, and competitive pricing. Traditional retailers are adopting omnichannel strategies, blending physical showrooms with online experiences to enhance customer engagement and expand reach.

What are the key drivers in the retail furniture market?

Rising Urbanization and Housing Development

Rapid urbanization, especially in emerging economies, is fueling demand for new housing units, directly boosting furniture consumption. Government housing initiatives and infrastructure development projects are further supporting this growth. Increasing urban population density is also driving demand for compact and multifunctional furniture solutions.

Growing Disposable Income and Lifestyle Upgrades

Rising income levels across developing regions are encouraging consumers to invest in premium and designer furniture. Lifestyle-driven purchasing behavior, influenced by social media and interior design trends, is boosting demand for aesthetically appealing and customized furniture products.

What are the restraints for the global market?

Volatility in Raw Material Prices

Fluctuations in the prices of wood, metal, and upholstery materials significantly impact manufacturing costs and profit margins. This volatility often leads to price increases, affecting consumer affordability and demand stability.

Supply Chain Disruptions

Global logistics challenges, including shipping delays and increased freight costs, have disrupted supply chains. These issues lead to longer delivery timelines and higher operational costs, particularly for imported furniture products.

What are the key opportunities in the retail furniture industry?

Expansion in Emerging Markets

Emerging economies such as India, Vietnam, and Indonesia present strong growth opportunities due to rising urbanization and expanding middle-class populations. These regions are expected to grow at rates significantly higher than the global average, supported by increasing housing demand and retail infrastructure development.

Sustainable Furniture and Circular Economy

The growing emphasis on sustainability is creating opportunities for manufacturers to innovate with eco-friendly materials such as recycled wood, bamboo, and low-emission finishes. Companies adopting circular economy practices, including furniture recycling and refurbishment, can gain competitive advantages and appeal to environmentally conscious consumers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 720 Billion |

| Market Size in 2026 | USD 764.64 Billion |

| Market Size in 2031 | USD 1032.95 Billion |

| CAGR | 6.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Living room furniture continues to hold the largest share of the global retail furniture market, accounting for approximately 32% of total demand in 2025. This segment’s leadership is primarily driven by its central role in household functionality and aesthetics, as living spaces serve as the focal point for social interaction and entertainment. Additionally, higher replacement frequency, compared to other furniture categories, combined with increasing consumer spending on interior décor and comfort-driven products such as recliners and modular sofas, is reinforcing its dominance. The growing popularity of open-plan living spaces and premiumization trends further support demand in this category.

Bedroom furniture represents the second-largest segment, supported by consistent demand from new residential construction and renovation cycles. Rising urban housing development and increased consumer focus on comfort and storage optimization, especially in compact apartments, are key growth drivers. The dining and kitchen furniture segments are expanding steadily, particularly due to the rapid adoption of modular kitchens and integrated dining solutions in urban households. Meanwhile, office furniture is witnessing accelerated growth due to hybrid and remote work trends, which have structurally increased demand for ergonomic chairs and compact workstations. Outdoor furniture is emerging as a high-growth niche, especially in developed markets, driven by increasing consumer interest in outdoor living, home aesthetics, and lifestyle upgrades.

Material Insights

Wood remains the dominant material segment, accounting for nearly 45% of the global market share in 2025, owing to its superior durability, aesthetic appeal, and strong consumer preference for natural materials. The segment’s leadership is further reinforced by its widespread application across all major furniture categories, particularly in premium and mid-range segments. Additionally, rising demand for sustainable and certified wood products is supporting long-term growth.

Engineered wood is gaining significant traction as a cost-effective and versatile alternative to solid wood, particularly in price-sensitive markets. Its ease of manufacturing, lower cost, and compatibility with modular furniture designs are key drivers of adoption. Upholstered furniture, including fabric and leather-based products, is witnessing strong demand growth, particularly in urban markets where comfort and design are key purchasing factors. Metal and plastic materials, while holding smaller shares, play a critical role in office and outdoor furniture segments due to their durability, lightweight properties, and cost efficiency. Increasing innovation in composite and hybrid materials is also expanding design possibilities and improving product performance.

Distribution Channel Insights

Offline retail channels continue to dominate the market, accounting for approximately 60% of total sales in 2025, as consumers prefer physical inspection of furniture before making purchase decisions. The ability to assess comfort, material quality, and dimensions in-store remains a key driver for offline sales. Specialty furniture stores and brand-exclusive showrooms are particularly influential in premium and customized segments.

However, online retail is the fastest-growing distribution channel, driven by increasing internet penetration, improved last-mile delivery infrastructure, and competitive pricing. E-commerce platforms are leveraging technologies such as augmented reality (AR) and virtual room planning tools to enhance customer confidence and reduce purchase hesitation. Direct-to-consumer (D2C) models are gaining traction as they allow manufacturers to bypass intermediaries, offer customized solutions, and improve margins. The integration of omnichannel strategies, combining physical stores with digital interfaces, is becoming a critical success factor for market participants.

End-Use Insights

The residential segment dominates the retail furniture market, contributing approximately 70% of total demand in 2025. This dominance is driven by strong global housing demand, increasing home ownership rates, and rising renovation activities. The trend toward personalized and aesthetically designed living spaces, supported by social media influence and interior design awareness, is further boosting residential furniture consumption.

The commercial segment, including offices, hospitality, retail, and institutional spaces, is growing at a steady CAGR of 7–8%. Demand in this segment is supported by the expansion of co-working spaces, corporate office upgrades, and growth in the global tourism and hospitality industry. The rise of co-living spaces, serviced apartments, and short-term rental platforms is also creating new demand avenues, particularly for modular, durable, and cost-efficient furniture solutions. Additionally, increasing investments in healthcare and educational infrastructure are contributing to demand for specialized institutional furniture.

Explore more data points, trends and opportunities Download Free Sample Report

Retail Furniture Market Segmentations

By Product Type

- Living Room Furniture

- Bedroom Furniture

- Dining Room Furniture

- Kitchen Furniture

- Office Furniture

- Outdoor & Garden Furniture

- Others

By Material Type

- Wood

- Metal

- Plastic & Polymer

- Glass

- Upholstered

- Hybrid/Composite Materials

By Distribution Channel

- Offline Retail

- Online Retail

By End-Use

- Residential

- Commercial

By Furniture Type

- Ready-to-Assemble (RTA)

- Fully Assembled

- Customized/Modular Furniture

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global retail furniture market, accounting for approximately 42% of the total market share in 2025. China leads the region with nearly 25% global contribution, driven by its large-scale manufacturing base, strong export capabilities, and robust domestic demand. India is the fastest-growing market in the region, expanding at a 9–10% CAGR, supported by rapid urbanization, rising disposable incomes, and government-led housing initiatives. Key regional growth drivers include an increasing middle-class population, rapid urban housing development, expansion of organized retail, and rising penetration of e-commerce platforms. Additionally, low-cost manufacturing advantages and strong supply chain ecosystems position the Asia-Pacific as both a production and consumption hub for furniture globally.

North America

North America holds around 25% of the global market share, led by the United States. The region’s growth is driven by high consumer spending power, strong housing renovation trends, and increasing demand for premium and customized furniture. Replacement demand plays a significant role, as consumers frequently upgrade furniture based on design trends and lifestyle changes. Other key drivers include the rapid adoption of online furniture retail, widespread availability of financing options, and strong demand for home office furniture driven by hybrid work models. Technological integration and sustainability initiatives are also shaping purchasing behavior in this region.

Europe

Europe accounts for approximately 20% of the global market, with Germany, France, and Italy as major contributors. The region is characterized by strong demand for high-quality, design-oriented, and sustainable furniture products. Growth drivers include stringent environmental regulations promoting eco-friendly materials, increasing consumer preference for premium and customized furniture, and a well-established housing market. Additionally, the presence of globally recognized furniture brands and design heritage in countries such as Italy supports innovation and export growth.

Latin America

Latin America is witnessing moderate growth, led by Brazil and Mexico. The region’s expansion is supported by increasing urbanization, rising middle-class income levels, and gradual growth in organized retail infrastructure. Key drivers include expanding real estate development, improving economic conditions, and growing consumer awareness of modern furniture designs. However, market growth is somewhat constrained by economic volatility and price sensitivity among consumers.

Middle East & Africa

The Middle East & Africa region is experiencing steady growth, driven by infrastructure development and rising demand for luxury furniture, particularly in the UAE and Saudi Arabia. High-income consumer segments and strong preference for premium and imported furniture are key demand drivers. Additional growth factors include large-scale real estate and hospitality projects, government investments in tourism infrastructure, and increasing urbanization in African economies. The region also benefits from rising demand for customized and high-end furniture solutions in commercial and residential sectors, particularly in metropolitan cities.

Key Players in the Retail Furniture Market

- IKEA

- Ashley Furniture Industries

- Steelcase

- Herman Miller

- HNI Corporation

- Okamura Corporation

- Williams-Sonoma

- La-Z-Boy

- Natuzzi

- Roche Bobois

- Wayfair

- DFS Furniture

- Haverty Furniture

- Godrej Interio

- Nitori Holdings