Residential Interior Doors Market Size

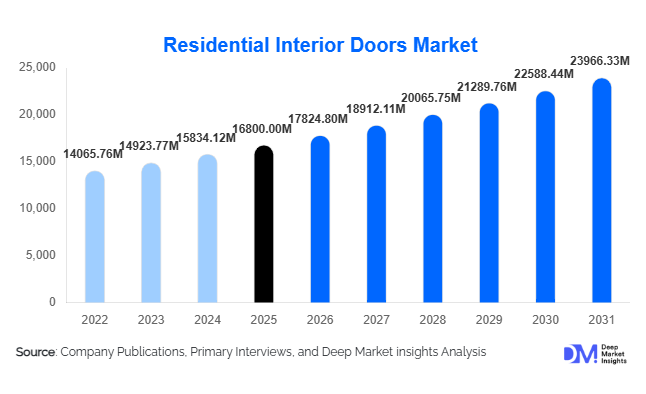

According to Deep Market Insights, the global residential interior doors market size was valued at USD 16,800 million in 2025 and is projected to grow from USD 17,824.80 million in 2026 to reach USD 23,966.33 million by 2031, expanding at a CAGR of 6.1% during the forecast period (2026–2031). The market growth is primarily driven by rising residential construction, increasing home renovation activities, and growing consumer preference for aesthetically appealing and durable interior solutions. The adoption of engineered wood and composite materials, coupled with demand for space-saving door designs, is further accelerating market expansion globally.

Key Market Insights

- Engineered wood doors dominate the market, driven by affordability, durability, and design flexibility.

- Panel doors account for the largest share, widely used across both new residential construction and renovation projects.

- Asia-Pacific leads the global market, supported by rapid urbanization and large-scale housing developments.

- The renovation and remodeling segment is the fastest-growing, especially in North America and Europe.

- Retail and e-commerce channels are expanding, enabling greater accessibility and customization options for consumers.

- Sustainability trends are influencing material choices, with increased adoption of eco-friendly and low-emission products.

What are the latest trends in the residential interior doors market?

Shift Toward Sustainable and Engineered Materials

The market is witnessing a strong transition toward environmentally sustainable materials such as engineered wood, MDF, and WPC composites. Consumers and builders are increasingly prioritizing low-emission, recyclable, and durable materials that comply with environmental standards. Manufacturers are investing in eco-friendly production processes and certifications to meet regulatory requirements and appeal to environmentally conscious buyers. This trend is particularly prominent in Europe and North America, where green building standards are widely adopted.

Growing Demand for Space-Saving and Modern Designs

Urban housing constraints are driving demand for space-efficient door solutions such as sliding, pocket, and bi-fold doors. These designs maximize usable space while enhancing interior aesthetics. Minimalist and modern interior trends are also influencing product development, with clean lines, neutral finishes, and glass integrations becoming increasingly popular. The rise of modular housing and compact apartments is further accelerating demand for innovative door mechanisms.

What are the key drivers in the residential interior doors market?

Expansion of Global Residential Construction

Rapid urbanization and population growth, particularly in the Asia-Pacific and emerging economies, are driving large-scale residential construction. Government-backed housing initiatives and infrastructure development projects are significantly increasing demand for interior doors. Countries such as China and India are leading this growth, contributing substantially to global market volume.

Rising Home Renovation and Remodeling Activities

In developed regions, aging housing stock and increasing disposable income are fueling renovation and remodeling activities. Homeowners are investing in interior upgrades to enhance property value and aesthetics, leading to consistent demand for replacement doors. The DIY home improvement trend, supported by retail and online distribution channels, is further boosting market growth.

What are the restraints for the global market?

Volatility in Raw Material Prices

Fluctuations in the prices of wood, MDF, and composite materials pose a significant challenge for manufacturers. Rising raw material costs can impact profit margins and lead to increased product pricing, potentially affecting demand in price-sensitive markets.

High Market Fragmentation and Price Competition

The presence of numerous regional and local manufacturers intensifies competition, resulting in pricing pressures. Low-cost imports and unorganized players further complicate the competitive landscape, making it difficult for established brands to maintain margins.

What are the key opportunities in the residential interior doors industry?

Growth in Emerging Housing Markets

Emerging economies present significant opportunities due to increasing urbanization and government-supported affordable housing programs. Manufacturers can capitalize on this demand by offering cost-effective and durable door solutions tailored to large-scale housing projects. Asia-Pacific and Africa are particularly promising regions for expansion.

Premiumization and Customization Trends

Consumers in developed markets are increasingly seeking customized and premium interior solutions. Demand for designer finishes, unique textures, and bespoke door sizes is rising, creating high-margin opportunities for manufacturers. The integration of glass elements and luxury finishes is gaining traction in this segment.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 16800 Million |

| Market Size in 2026 | USD 17824.80 Million |

| Market Size in 2031 | USD 23966.33 Million |

| CAGR | 6.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Panel doors dominate the residential interior doors market, accounting for approximately 42% of the global share in 2025. Their leadership is primarily driven by their structural versatility, cost efficiency, and ability to complement both traditional and contemporary interior designs. Panel doors are widely adopted across mass housing projects as well as premium residential spaces due to their availability in multiple configurations, such as flush, raised, and molded panels. Additionally, advancements in engineered wood and molded skin technologies have enhanced durability while reducing costs, further strengthening their adoption globally.

Meanwhile, sliding and bi-fold doors are emerging as high-growth segments, particularly in urban markets where space optimization is critical. The rise of compact apartments, modular housing, and open-plan living concepts is accelerating demand for these space-saving solutions. Their ability to improve spatial efficiency while enhancing aesthetic appeal makes them increasingly popular in metropolitan regions across the Asia-Pacific and Europe.

Application Insights

New residential construction remains the dominant application segment, contributing approximately 58% of total demand in 2025. This dominance is driven by rapid urbanization, population growth, and large-scale housing projects across emerging economies such as China, India, and Southeast Asia. Government-backed affordable housing initiatives and infrastructure development programs are significantly boosting demand for interior doors in newly constructed homes.

However, the renovation and remodeling segment is the fastest-growing, supported by rising consumer spending on home improvement in developed regions such as North America and Europe. Aging housing stock, coupled with increasing awareness of interior aesthetics and energy efficiency, is driving replacement demand. Homeowners are increasingly opting for modern, durable, and design-oriented doors, including those with enhanced insulation and acoustic properties. The growing DIY culture and availability of customizable products through retail and online channels are further accelerating growth in this segment.

Distribution Channel Insights

Retail stores lead the distribution channel segment, accounting for approximately 40% of the global market share in 2025. Their dominance is driven by strong consumer preference for physical product evaluation, immediate availability, and access to installation services. Large home improvement chains and specialty stores play a critical role in influencing purchase decisions, particularly for renovation projects.

At the same time, online and e-commerce channels are witnessing rapid expansion, driven by increasing digital adoption and the growing popularity of DIY home improvement. These platforms offer advantages such as price transparency, product customization, and doorstep delivery, making them particularly attractive to younger consumers. Manufacturers are increasingly adopting omnichannel strategies, integrating digital platforms with traditional retail to enhance customer reach and engagement.

End-User Insights

The residential segment remains the core end-user base for interior doors, with demand primarily driven by new housing developments. Large-scale residential construction projects continue to generate substantial volume demand, particularly in emerging markets.

However, renovation-focused end users are becoming a key growth driver, especially in developed economies where homeowners prioritize upgrading interior aesthetics, functionality, and property value. The increasing adoption of smart home technologies is also influencing door design, with features such as noise insulation, modular installation, and compatibility with automated systems gaining traction. Additionally, rising consumer preference for personalized and premium interior solutions is encouraging manufacturers to offer customized door designs, finishes, and materials.

Explore more data points, trends and opportunities Download Free Sample Report

Residential Interior Doors Market Segmentations

By Product Type

- Panel Doors

- Sliding Doors

- Bi-fold Doors

- French Doors

- Barn Doors

- Others

By Application

- New Residential Construction

- Residential Renovation & Remodeling

By Distribution Channel

- Retail Stores

- Online/E-commerce

- Direct Sales

- Specialty Stores

By Material Type

- Wood

- Glass

- Metal

- Composite

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global residential interior doors market, accounting for approximately 45% of the total market share in 2025. The region’s leadership is primarily driven by rapid urbanization, population growth, and extensive residential construction activities in countries such as China, India, Indonesia, and Vietnam. China alone contributes nearly 25% of global demand, supported by large-scale urban housing developments and government infrastructure investments.

India is emerging as one of the fastest-growing markets, driven by government initiatives such as affordable housing programs, increasing middle-class income, and rising homeownership rates. Southeast Asian countries are also witnessing strong growth due to expanding urban populations and foreign investments in real estate. Additionally, the availability of low-cost raw materials and manufacturing capabilities in the region supports large-scale production, further strengthening the Asia-Pacific’s market dominance.

North America

North America holds approximately 22% of the global market share, with the United States being the primary contributor. The region’s growth is largely driven by robust renovation and remodeling activities, supported by high disposable income and strong consumer spending on home improvement. Aging housing infrastructure is a key factor driving replacement demand for interior doors.

Another important growth driver is the increasing demand for premium, customized, and energy-efficient door solutions. Consumers in North America are willing to invest in high-quality materials, designer finishes, and smart home-compatible products. The presence of well-established distribution networks and advanced manufacturing technologies further supports market growth in this region.

Europe

Europe accounts for approximately 20% of the global market, with key contributors including Germany, the United Kingdom, and France. The region’s growth is strongly influenced by stringent environmental regulations and increasing demand for sustainable building materials. Manufacturers are focusing on eco-friendly production processes and certified wood products to comply with regulatory standards.

The renovation segment is a major growth driver in Europe due to aging housing stock and government incentives for energy-efficient home upgrades. Additionally, consumer preference for premium and customized interior solutions is driving demand for high-quality doors with advanced finishes and insulation properties.

Latin America

Latin America represents approximately 8% of the global market, with Brazil and Mexico leading regional demand. Market growth is supported by increasing urbanization, improving economic conditions, and the gradual expansion of the residential construction sector.

Government initiatives aimed at improving housing infrastructure and rising middle-class income levels are key drivers in the region. Additionally, growing investments in real estate development and urban housing projects are contributing to steady demand for interior doors. However, price sensitivity remains a key factor, leading to higher demand for cost-effective products such as hollow core and engineered wood doors.

Middle East & Africa

The Middle East and Africa region is experiencing steady growth in the residential interior doors market, driven by increasing investments in housing and urban development. Countries such as the UAE and Saudi Arabia are leading demand due to large-scale residential and mixed-use development projects.

Government initiatives focused on infrastructure development and economic diversification are key growth drivers in this region. In addition, rising expatriate populations and increasing demand for modern housing are contributing to market expansion. Africa is also witnessing gradual growth, supported by urbanization and improving housing conditions, although infrastructure challenges and economic constraints may limit rapid adoption in certain areas.

Key Players in the Residential Interior Doors Market

- Masonite International Corporation

- JELD-WEN Holding Inc.

- ASSA ABLOY

- Andersen Corporation

- Pella Corporation

- Simpson Door Company

- Marvin Windows & Doors

- Steves & Sons Inc.

- TruStile Doors LLC

- LIXIL Group Corporation

- VKR Holding (VELUX Group)

- Hormann Group

- Sanwa Holdings Corporation

- Godrej Interio

- DCM Shriram (Fenesta)