Residential Cooking Grill Market Size

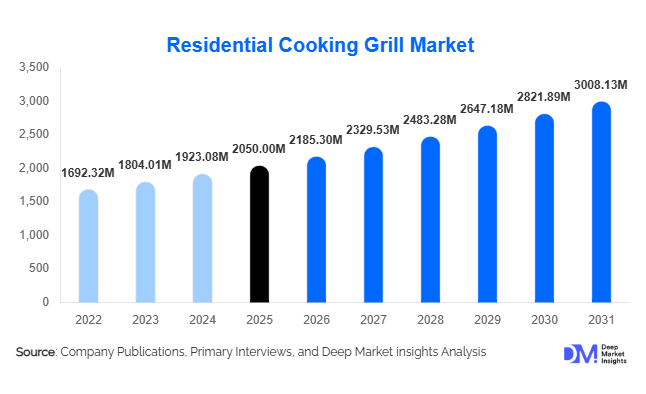

According to Deep Market Insights, the global residential cooking grill market size was valued at USD 2,050 million in 2025 and is projected to grow from USD 2185.30 million in 2026 to reach USD 3008.13 million by 2031, expanding at a CAGR of 6.6% during the forecast period (2026–2031). The market growth is primarily driven by increasing adoption of outdoor cooking appliances, rising consumer interest in smart and connected grilling technologies, and the expansion of outdoor kitchen trends across developed and emerging economies.

Key Market Insights

- Gas grills dominate the product landscape, offering convenience, quick ignition, and precise temperature control, making them the most preferred choice for residential users globally.

- Outdoor kitchen and freestanding grill installations are expanding, particularly in North America and Europe, as consumers invest in backyard entertainment and modular outdoor cooking solutions.

- Asia-Pacific is the fastest-growing region, led by rising middle-class disposable income, urbanization, and growing exposure to Western cooking lifestyles.

- Technological integration in smart grills, including Wi-Fi connectivity, app-based temperature control, and automated pellet feeding systems, is reshaping consumer preferences in premium segments.

- Mid-range grills (USD 200–800) dominate global sales, offering a balance of affordability and performance for the largest consumer base.

- Electric and compact grills are gaining traction, particularly among urban households in densely populated areas with limited outdoor space.

What are the latest trends in the residential cooking grill market?

Smart and Connected Grills

Manufacturers are increasingly integrating smart technologies into residential grills, including Wi-Fi-enabled temperature monitoring, remote control via mobile apps, and automated fuel systems. Smart grills allow users to track cooking progress, adjust temperatures, and receive alerts, enhancing convenience and cooking precision. This trend is strongest among premium buyers and tech-savvy consumers in North America and Europe. IoT-enabled grills are also being integrated into connected home ecosystems, with compatibility for voice assistants and smart appliances.

Outdoor Kitchen Integration

Outdoor kitchens are emerging as a significant driver of demand for built-in and freestanding grills. These setups often include countertops, refrigeration units, and multi-burner grills, enabling complete backyard cooking experiences. The trend is fueled by growing consumer interest in home improvement, social gatherings, and entertainment-oriented lifestyles. Premium installations enhance property value and appeal to affluent homeowners seeking multifunctional outdoor spaces.

What are the key drivers in the residential cooking grill market?

Increasing Outdoor Cooking Culture

Backyard barbecues and family gatherings have transformed outdoor cooking into a lifestyle trend. Consumers are investing in larger, feature-rich grills to host events and prepare diverse cuisines. This cultural shift is particularly strong in North America and Europe, where grilling is a traditional social activity.

Rising Disposable Income and Premium Appliance Adoption

Household income growth in both developed and emerging markets is driving the adoption of premium grills. High-end grills with stainless steel construction, multiple burners, and smart controls are increasingly popular, offering long-term durability and convenience. Consumers are willing to invest in quality and advanced features for home entertainment and culinary versatility.

Product Innovation and Technological Advancement

Innovations such as infrared burners, pellet grills, multi-fuel options, and app-controlled systems are expanding the market by attracting tech-savvy and convenience-oriented consumers. The integration of smart technologies is enhancing user experience and driving adoption across premium and mid-range segments.

What are the restraints for the global market?

High Cost of Premium Grills

The high upfront cost of built-in and premium outdoor grills limits accessibility in price-sensitive markets. Premium systems, including multi-burner setups and smart grills, can range from several hundred to several thousand dollars, reducing penetration in emerging economies.

Space Constraints in Urban Areas

Urban households with limited balcony or yard space face challenges in installing large grills, constraining market adoption in dense metropolitan areas, particularly in the Asia-Pacific and Europe. Compact or electric grills address some limitations, but larger traditional grills remain restricted to suburban or low-density housing.

What are the key opportunities in the residential cooking grill market?

Smart Grill Technology Expansion

Connected and IoT-enabled grills represent a high-growth opportunity. Manufacturers can capitalize on consumer demand for smart appliances that offer remote control, automated cooking, and app-based guidance. Integration with smart home ecosystems allows differentiation and enhances brand loyalty.

Outdoor Kitchen and Home Improvement Trends

Investment in backyard entertainment spaces and modular outdoor kitchens offers significant growth potential. Built-in grills, multi-functional cooking stations, and premium outdoor appliances allow manufacturers to target high-margin, affluent households seeking lifestyle-oriented products.

Emerging Market Penetration

Asia-Pacific and Latin America represent untapped growth regions. Rising disposable incomes, urban lifestyle shifts, and exposure to Western culinary habits are expanding the demand for residential grills. Portable, electric, and mid-range grills are particularly suited for urban apartments and smaller homes in these regions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2050 Million |

| Market Size in 2026 | USD 2185.30 Million |

| Market Size in 2031 | USD 3008.13 Million |

| CAGR | 6.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Gas grills dominate the global residential cooking grill market, accounting for approximately 48% of total revenue in 2025. The segment’s leadership is primarily driven by its convenience, quick ignition systems, and superior temperature control compared to traditional grilling options. Gas grills, particularly propane and natural gas models, enable consistent heat distribution and faster cooking times, making them the preferred choice among households that prioritize convenience and efficiency. Their popularity is especially pronounced in North America and Europe, where consumers frequently host outdoor gatherings and prefer easy-to-operate cooking appliances. Another key factor driving the dominance of gas grills is their compatibility with modern outdoor kitchen installations. Built-in gas grills are widely integrated into premium backyard cooking setups that include modular countertops, refrigeration units, and smoker attachments. The availability of advanced features such as multiple burners, infrared heating zones, rotisserie systems, and digital temperature controls further strengthens demand for gas grills in the premium appliance segment.

Charcoal grills continue to appeal to traditional barbecue enthusiasts who prefer the distinctive smoky flavor produced by charcoal cooking. These grills remain particularly popular in regions with strong barbecue traditions, including Latin America and parts of Europe. Electric grills are witnessing rising adoption in urban areas where regulations limit charcoal or gas usage in apartment buildings. Pellet grills, which use wood pellets as fuel, are gaining traction among cooking enthusiasts seeking a balance between traditional smoky flavor and modern temperature control. Hybrid and multi-fuel grills represent an emerging niche segment, allowing consumers to switch between gas, charcoal, and pellet fuel systems. These versatile appliances are particularly attractive to consumers seeking flexibility in cooking techniques and flavor profiles.

Installation Type Insights

Portable and freestanding grills represent the largest installation segment in the residential cooking grill market, accounting for approximately 64% of global demand in 2025. The popularity of this segment is primarily driven by affordability, portability, and ease of installation. Freestanding grills can be easily moved within outdoor spaces and require minimal setup, making them highly attractive to homeowners with patios, balconies, or small backyard areas. The segment is particularly popular among younger households, renters, and outdoor recreation enthusiasts who prefer flexible cooking appliances that can be used for camping, tailgating, or beach gatherings. Manufacturers are increasingly introducing lightweight, compact grill designs with foldable stands and travel-friendly features to capture demand from the outdoor recreation market.

Built-in grills are gaining significant traction in the premium segment, particularly in developed markets such as the United States, Canada, Germany, and Australia. These grills are typically integrated into permanent outdoor kitchen installations that form part of broader home improvement and landscaping projects. Rising consumer spending on backyard entertainment spaces, patios, and modular outdoor kitchens is driving strong growth for built-in grill installations. High-end built-in grills are often constructed with stainless steel materials and incorporate advanced features such as multiple cooking zones, rotisserie attachments, and smart temperature control systems. These products cater to affluent homeowners seeking restaurant-quality cooking experiences in residential settings.

Distribution Channel Insights

Offline retail channels dominate the global residential cooking grill market, accounting for approximately 70% of total sales in 2025. Physical retail outlets, including home improvement stores, specialty outdoor cooking appliance retailers, and department stores, continue to play a crucial role in the purchasing process. Consumers often prefer to evaluate grill size, construction quality, and material durability in person before making a purchase decision, particularly for mid-range and premium products. Large home improvement retail chains and specialty outdoor cooking stores also offer installation services, warranty support, and product demonstrations, which enhance the overall consumer purchasing experience. In addition, seasonal promotional campaigns during summer and holiday periods significantly boost grill sales through offline channels.

Online retail platforms are witnessing rapid growth, particularly in Asia-Pacific and emerging markets where e-commerce penetration is expanding rapidly. Online channels allow consumers to access a wider variety of grill models, compare prices, and benefit from direct-to-consumer offerings from manufacturers. Many grill manufacturers are strengthening their digital presence by launching dedicated brand websites, offering customization options, and integrating augmented reality tools that allow customers to visualize grills in their outdoor spaces. The growing influence of online product reviews, influencer marketing, and digital advertising is also encouraging consumers to research and purchase grilling appliances through e-commerce platforms.

End-Use Insights

Residential households represent the primary end-use segment for cooking grills, accounting for the vast majority of global demand. The increasing popularity of home-based cooking, backyard entertainment, and family gatherings is driving strong adoption of residential grill appliances across developed and emerging economies. In markets such as the United States and Canada, grilling is deeply embedded in household culture, with a significant portion of homes owning at least one outdoor grill. Secondary demand segments are emerging from outdoor recreation activities such as camping, tailgating, and beach cooking events. Portable grills designed specifically for travel and outdoor activities are gaining popularity among younger consumers and adventure enthusiasts. These compact appliances offer lightweight designs and quick setup features that make them ideal for recreational use.

Urban apartment dwellers represent another growing consumer segment, particularly in Asia-Pacific and European cities where outdoor space is limited. Manufacturers are addressing this demand by introducing compact electric grills and smokeless indoor grilling appliances suitable for balconies and small kitchens. Export-driven manufacturing also plays a significant role in the market, with China serving as one of the largest production hubs for residential grills globally. A large proportion of grills manufactured in China are exported to North America and Europe, supporting global supply chains and enabling cost-efficient production for international brands.

Explore more data points, trends and opportunities Download Free Sample Report

Residential Cooking Grill Market Segmentations

By Product Type

- Gas Grills

- Charcoal Grills

- Electric Grills

- Pellet Grills

- Hybrid / Multi-Fuel Grills

By Installation Type

- Portable / Freestanding Grills

- Built-in Grills

By Distribution Channel

- Offline Retail

- Online Retail

By End-Use

- Residential Households

- Outdoor Recreation and Camping

- Urban Apartments and Compact Living Spaces

- Vacation Homes and Secondary Residences

Regional Insights

North America

North America holds the largest share of the global residential cooking grill market, accounting for approximately 38% of global demand in 2025. The United States represents the dominant market within the region, followed by Canada. The strong cultural tradition of outdoor barbecuing and backyard gatherings is a major driver of grill adoption across North American households. High disposable income levels and widespread suburban housing with large backyard spaces create favorable conditions for grill ownership. In addition, consumers in the region are highly receptive to premium appliances and technological innovations, including smart grills equipped with Wi-Fi connectivity and app-based cooking controls.

Another key growth driver in North America is the booming home improvement and outdoor living market. Homeowners are increasingly investing in patios, decks, and fully equipped outdoor kitchens, which often feature built-in gas grills as centerpiece appliances. Seasonal grilling events, sporting gatherings, and holiday celebrations further sustain strong demand for residential grills in this region.

Europe

Europe accounts for approximately 27% of the global residential cooking grill market, with major demand centers in Germany, the United Kingdom, France, and Italy. European consumers are increasingly adopting grilling appliances as part of outdoor leisure activities and summer gatherings. Urbanization and environmental regulations in several European cities are encouraging the adoption of electric grills, which produce fewer emissions and are more suitable for apartment balconies and indoor spaces. Additionally, strong consumer awareness regarding sustainability and energy efficiency is driving demand for modern electric and pellet grill technologies. The region’s growing interest in outdoor lifestyle trends, including garden parties and recreational cooking, is also boosting grill sales. Premium grill brands are expanding their presence across Europe by introducing compact models tailored to smaller outdoor spaces commonly found in urban European homes.

Asia-Pacific

Asia-Pacific represents approximately 24% of the global residential cooking grill market and is the fastest-growing regional market. Rapid urbanization, rising disposable incomes, and the growing influence of Western food culture are key factors driving demand across the region. China plays a dual role in the market as both a major manufacturing hub and a rapidly growing consumer market. The expansion of middle-class households and increasing popularity of home-based cooking appliances are contributing to rising grill adoption in Chinese cities.

India is emerging as a promising market due to increasing urban middle-class populations, rising e-commerce penetration, and growing consumer exposure to international culinary trends. In developed Asia-Pacific markets such as Japan, South Korea, and Australia, demand for premium grills and outdoor cooking appliances is supported by strong outdoor leisure cultures.Compact electric grills and portable models are particularly popular in the region due to limited living space in urban environments and regulatory restrictions on charcoal grilling in residential areas.

Latin America

Latin America accounts for approximately 6% of the global residential cooking grill market, with Brazil and Mexico representing the largest regional markets. Barbecue culture is deeply embedded in Latin American cuisine, particularly in Brazil, where traditional grilling methods such as churrasco are widely practiced. Rising disposable income levels and expanding urban middle-class populations are driving greater adoption of modern grilling appliances in the region. Portable charcoal grills remain popular due to their affordability and ability to replicate traditional cooking methods. Growing tourism, outdoor recreational activities, and increasing exposure to international culinary trends are also contributing to steady growth in residential grill demand across Latin American countries.

Middle East & Africa

The Middle East and Africa region accounts for approximately 5% of global demand for residential cooking grills. Demand is primarily concentrated in Gulf Cooperation Council (GCC) countries such as the United Arab Emirates and Saudi Arabia, where luxury villas and large residential properties often include outdoor entertainment areas. Affluent households in these markets are increasingly adopting premium built-in grills and outdoor kitchen systems as part of high-end residential developments. The region’s warm climate and strong culture of outdoor social gatherings also support year-round grill usage. In Africa, the market is supported by increasing local manufacturing and regional export activity. South Africa represents the largest grill market on the continent, driven by strong barbecue traditions and growing consumer demand for modern cooking appliances.

Key Players in the Residential Cooking Grill Market

- Weber Inc.

- Traeger Inc.

- Napoleon

- Char-Broil

- Middleby Corporation

- Landmann

- Blackstone Products

- Broil King

- Dyna-Glo

- Masterbuilt Manufacturing

- Char-Griller

- Nexgrill Industries

- Bull Outdoor Products

- Fire Magic Grills

- Coleman Company