Residential Carpet Roll Market Size

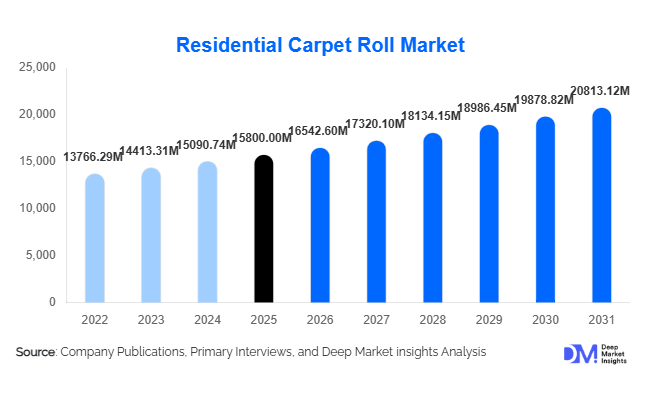

According to Deep Market Insights, the global residential carpet roll market size was valued at USD 15,800 million in 2025 and is projected to grow from USD 16,542.60 million in 2026 to reach USD 20,813.12 million by 2031, expanding at a CAGR of 4.7% during the forecast period (2026–2031). The residential carpet roll market growth is primarily driven by increasing residential construction activities, rising renovation spending in developed economies, and growing consumer preference for comfort-oriented flooring solutions. Additionally, technological advancements in stain-resistant fibers, eco-friendly materials, and improved durability are enhancing product appeal across mid-range and premium segments.

Key Market Insights

- Mid-range carpet rolls dominate the market, accounting for nearly 50% share due to affordability and balanced performance characteristics.

- Tufted carpet rolls lead the construction type, contributing approximately 70% of total market demand owing to cost efficiency and scalability.

- North America dominates the global market, holding around 35% share, driven by strong renovation demand and high carpet adoption rates.

- Asia-Pacific is the fastest-growing region, supported by rapid urbanization and expanding residential housing projects.

- Sustainability trends are reshaping product development, with increased demand for recyclable and low-VOC carpet materials.

- Offline retail remains the dominant distribution channel, contributing about 65% of total sales due to consumer preference for physical inspection.

What are the latest trends in the residential carpet roll market?

Sustainable and Eco-Friendly Carpets Gaining Momentum

The residential carpet roll market is witnessing a strong shift toward sustainable materials and manufacturing processes. Consumers are increasingly opting for carpets made from recycled fibers, bio-based materials, and low-emission compounds. Regulatory frameworks in regions such as Europe and North America are encouraging manufacturers to adopt eco-friendly practices, including recyclable backing systems and reduced chemical usage. This trend is also driving innovation in circular economy models, where companies offer take-back and recycling programs. Sustainable certifications are becoming a key differentiator, influencing purchasing decisions among environmentally conscious buyers.

Digitalization and E-Commerce Expansion

The rise of digital platforms is transforming how consumers purchase carpet rolls. Online channels are growing at a rapid pace, supported by visualization tools, augmented reality applications, and virtual room planners. These technologies allow customers to simulate carpet installations before purchase, enhancing decision-making. Direct-to-consumer models are also gaining traction, enabling manufacturers to bypass intermediaries and improve margins. Additionally, digital platforms are facilitating price transparency, product comparisons, and access to global brands, making them an increasingly important sales channel in urban markets.

What are the key drivers in the residential carpet roll market?

Growth in Residential Construction and Renovation

Rising residential construction activities globally are a major driver of carpet roll demand. Emerging economies are witnessing large-scale housing developments, while developed markets are experiencing strong renovation cycles. Carpet rolls are widely preferred in renovation projects due to their cost-effectiveness, ease of installation, and aesthetic versatility. Replacement cycles of 7–10 years further contribute to sustained demand, particularly in North America and Europe.

Increasing Preference for Comfort and Insulation

Carpet rolls offer superior thermal insulation and noise reduction, making them highly desirable in residential settings such as bedrooms and living rooms. This is particularly relevant in colder climates, where energy efficiency and indoor comfort are critical considerations. The growing focus on home comfort and interior aesthetics is further boosting adoption, especially in mid-range and premium housing segments.

What are the restraints for the global market?

Competition from Hard Flooring Alternatives

The increasing popularity of hard flooring options such as luxury vinyl tiles, hardwood, and ceramic tiles is a significant restraint for the market. These alternatives are often perceived as more durable, easier to maintain, and more suitable for households with pets or allergies. This shift in consumer preference is gradually limiting carpet adoption in certain regions.

Raw Material Price Volatility

Fluctuations in the prices of synthetic fibers such as nylon and polyester pose challenges for manufacturers. These materials are derived from petrochemicals, making them sensitive to crude oil price changes. Variability in input costs affects profit margins and pricing strategies, creating uncertainty in the market.

What are the key opportunities in the residential carpet roll industry?

Expansion in Emerging Housing Markets

Rapid urbanization and population growth in emerging economies present significant opportunities for market expansion. Countries such as India, China, and Indonesia are witnessing increased demand for affordable housing, driving the need for cost-effective flooring solutions. Manufacturers can capitalize on this trend by establishing localized production and distribution networks to improve accessibility and reduce costs.

Technological Innovation in Carpet Manufacturing

Advancements in fiber technology, including stain-resistant coatings, antimicrobial treatments, and enhanced durability, are creating new growth opportunities. Smart carpets with embedded sensors and digital customization options are also emerging, offering added value to consumers. These innovations are particularly appealing in premium segments and can help companies differentiate their offerings in a competitive market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 15800 Million |

| Market Size in 2026 | USD 16542.60 Million |

| Market Size in 2031 | USD 20813.12 Million |

| CAGR | 4.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Nylon carpet rolls dominate the global residential carpet roll market with approximately 32% share in 2025, primarily driven by their superior durability, resilience under heavy foot traffic, and strong stain resistance properties. These characteristics make nylon the preferred choice for high-usage residential areas such as living rooms, hallways, and multi-family housing units. Additionally, continuous innovation in solution-dyed nylon and advanced fiber treatments has enhanced color retention and lifecycle performance, further strengthening its leading position. Polyester and polypropylene (olefin) carpet rolls are widely adopted in cost-sensitive applications due to their affordability and ease of maintenance. Polyester carpets, in particular, are gaining traction due to their soft texture and improved eco-profile, as many variants are manufactured using recycled PET fibers. Polypropylene carpets, while less durable than nylon, offer excellent moisture resistance, making them suitable for basements and low-traffic areas.

Wool carpet rolls, although accounting for a smaller share, are witnessing increased demand in premium and luxury segments due to their natural composition, biodegradability, and superior comfort. The segment is particularly strong in Europe and high-income households globally. Blended fiber carpets are emerging as a balanced solution, combining the durability of synthetic fibers with the aesthetic and tactile advantages of natural materials, thereby addressing both performance and cost considerations.

Application Insights

Living rooms and bedrooms collectively represent the largest application segment, accounting for approximately 55% of total market demand. This dominance is driven by the increasing consumer preference for comfort, warmth, and noise insulation in primary living spaces. Carpet rolls provide a softer underfoot experience compared to hard flooring, making them particularly desirable in family-centric environments and colder climates. The growth of this segment is further supported by interior design trends that emphasize cozy and aesthetically appealing home environments. Neutral tones, textured finishes, and plush pile carpets are increasingly favored in these spaces. Additionally, rising disposable incomes and increased spending on home décor are reinforcing demand in this segment.

Staircases and hallways require highly durable and wear-resistant carpets, often utilizing loop pile or low-pile constructions to withstand heavy foot traffic. Basements represent a niche but growing application, particularly in North America, where moisture-resistant carpets are preferred. Home offices have emerged as a fast-growing sub-segment, driven by the rise of remote and hybrid work models. Carpets in these spaces are valued for their acoustic insulation properties, enhancing productivity by reducing noise levels.

Distribution Channel Insights

Offline retail channels dominate the residential carpet roll market, accounting for approximately 65% of total sales in 2025. This leadership is primarily driven by consumer preference for physically evaluating carpet texture, thickness, and color before purchase. Specialty flooring stores, home improvement retailers, and dealer networks play a critical role in influencing purchasing decisions, particularly for mid-range and premium products. The dominance of offline channels is also supported by value-added services such as in-store consultation, measurement, customization, and installation support. These services are particularly important for large-area installations, where accuracy and professional guidance are essential.

However, online retail channels are experiencing rapid growth, with a CAGR exceeding 8%, fueled by digital transformation and evolving consumer behavior. E-commerce platforms are enabling wider product accessibility, competitive pricing, and convenient home delivery. The integration of augmented reality (AR) tools and virtual room visualization technologies is helping bridge the gap between online and offline experiences, particularly among younger, urban consumers. Direct-to-consumer (D2C) strategies adopted by manufacturers are further accelerating online channel growth.

Price Range Insights

The mid-range segment leads the market, accounting for approximately 50% of total market share in 2025. This segment’s dominance is driven by its ability to offer a balanced combination of affordability, durability, and aesthetic appeal, making it highly attractive to middle-income households globally. The expansion of the middle class, particularly in emerging economies, is a key driver supporting this segment. Economy carpets cater to budget-conscious consumers and are widely used in rental properties, low-cost housing, and high-turnover residential units. This segment is particularly prominent in Asia-Pacific and Latin America, where affordability remains a key purchasing criterion.

Premium and luxury carpet rolls are gaining traction in high-end residential projects and renovation activities in developed markets. These carpets often feature high-quality materials such as wool, intricate designs, and advanced manufacturing techniques. Increasing consumer focus on interior aesthetics and lifestyle enhancement is driving growth in this segment, although it represents a smaller share compared to mid-range products.

Explore more data points, trends and opportunities Download Free Sample Report

Residential Carpet Roll Market Segmentations

By Material Type

- Nylon Carpet Rolls

- Polyester Carpet Rolls

- Polypropylene (Olefin) Carpet Rolls

- Wool Carpet Rolls

- Blended Fiber Carpet Rolls

By Construction Type

- Tufted Carpet Rolls

- Woven Carpet Rolls

- Needle-Punched Carpet Rolls

- Knotted Carpet Rolls

By Application

- Living Rooms & Bedrooms

- Staircases & Hallways

- Basements

- Home Offices

By Distribution Channel

- Offline Retail

- Online Retail

- Contractor/Builder Sales

By Price Range

- Economy Segment

- Mid-Range Segment

- Premium/Luxury Segment

Regional Insights

North America

North America remains the largest regional market, accounting for approximately 35% of global demand in 2025, with the United States contributing nearly 75% of the regional share. The region’s dominance is driven by strong residential renovation activity, high disposable income levels, and a long-standing cultural preference for carpeted interiors, particularly in suburban housing. Key growth drivers include the large aging housing stock requiring periodic flooring replacement, high consumer spending on home improvement, and widespread adoption of wall-to-wall carpeting in bedrooms and living spaces. Additionally, advanced distribution networks and the presence of leading manufacturers contribute to market maturity. The increasing demand for sustainable and hypoallergenic carpets is also shaping product innovation in this region.

Europe

Europe accounts for approximately 25% of the global market, with major contributions from countries such as the UK, Germany, and France. The region is characterized by a strong emphasis on sustainability, quality, and design innovation. Growth in Europe is driven by stringent environmental regulations, which are encouraging the adoption of eco-friendly and recyclable carpet materials. Consumer preference for premium and certified products is significantly higher compared to other regions. Additionally, renovation activities in older residential buildings and increasing demand for energy-efficient insulation solutions are supporting market growth. The presence of established carpet manufacturing hubs in countries like Belgium and the Netherlands further strengthens regional supply capabilities.

Asia-Pacific

Asia-Pacific is the fastest-growing region, registering a CAGR of over 6% during the forecast period. China dominates the regional market with approximately 40% share, while India is emerging as the fastest-growing country due to rapid urbanization and large-scale housing development initiatives. Key growth drivers include expanding middle-class populations, rising disposable incomes, and increasing demand for affordable housing. Government initiatives promoting residential construction, such as affordable housing schemes in India and urban redevelopment projects in China, are significantly boosting demand for carpet rolls. Additionally, changing lifestyle preferences and growing awareness of interior design are contributing to increased adoption, particularly in urban areas.

Latin America

Latin America is experiencing gradual market expansion, with Brazil and Mexico serving as the primary growth markets. The region’s growth is driven by improving housing infrastructure, urbanization, and rising middle-class income levels. Demand in this region is largely concentrated in the mid-range and economy segments, reflecting price sensitivity among consumers. Increasing investments in residential construction and government housing programs are supporting market growth. However, economic volatility and currency fluctuations may pose challenges to sustained expansion.

Middle East & Africa

The Middle East & Africa region is witnessing steady growth, supported by increasing residential construction and urban development in countries such as Saudi Arabia and the UAE. The region benefits from strong demand for premium and luxury carpet rolls, particularly in high-end housing projects and villas. Key growth drivers include government-led infrastructure development programs, rising expatriate populations, and increasing investment in real estate. In Africa, urbanization and improving housing conditions are gradually boosting demand for affordable carpet solutions. Additionally, the region’s preference for aesthetic and luxury interiors is supporting the growth of high-value carpet segments.

Key Players in the Residential Carpet Roll Market

- Shaw Industries Group

- Mohawk Industries

- Interface Inc.

- Tarkett S.A.

- Beaulieu International Group

- Balta Group

- Milliken & Company

- Victoria PLC

- Oriental Weavers Group

- Dixie Group Inc.

- Engineered Floors LLC

- Phenix Flooring

- Godfrey Hirst

- Welspun Flooring

- Tai Ping Carpets International