Refurbished Computers & Laptops Market Size

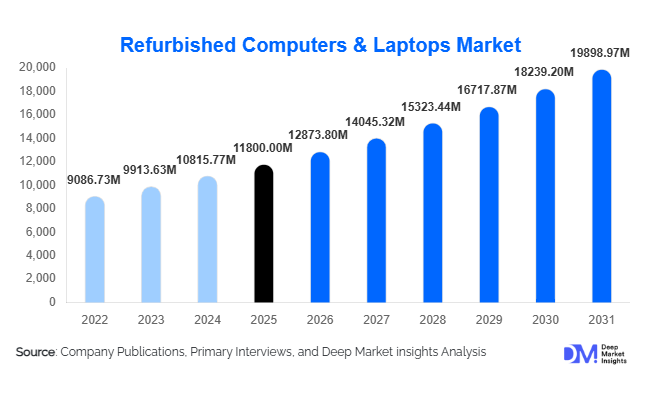

According to Deep Market Insights, the global refurbished computers & laptops market size was valued at USD 11,800 million in 2025 and is projected to grow from USD 12,873.80 million in 2026 to reach USD 19,898.97 million by 2031, expanding at a CAGR of 9.1% during the forecast period (2026–2031). The refurbished computers & laptops market growth is primarily driven by the rising demand for affordable computing devices, increasing focus on circular economy practices, and the growing adoption of IT asset disposition programs among enterprises.

Refurbished computers and laptops are previously owned devices that undergo diagnostic testing, hardware replacement, software upgrades, and quality certification before being resold. These devices offer performance comparable to new systems while costing 30–60% less, making them highly attractive for price-sensitive consumers, educational institutions, and small businesses. The market has evolved from an informal resale ecosystem into a structured industry supported by certified refurbishment programs operated by major OEMs and specialized refurbishing companies.

The rising cost of new hardware and the global push toward sustainable electronics consumption are accelerating adoption. Governments and enterprises are increasingly promoting device reuse to reduce electronic waste and carbon emissions associated with manufacturing new hardware. Additionally, improvements in refurbishment technology, including automated diagnostics and standardized grading systems, have increased reliability and consumer confidence in refurbished devices. With growing digitalization across emerging markets and expanding online distribution channels, refurbished computing devices are expected to play a critical role in improving digital accessibility worldwide.

Key Market Insights

- Refurbished laptops dominate the market, accounting for more than half of global demand due to strong adoption across education, remote work, and small business applications.

- North America leads the market, driven by large enterprise IT refresh cycles and strong corporate IT asset disposition programs.

- Asia-Pacific is the fastest-growing region, supported by rapid digitalization and demand for affordable computing devices in emerging economies.

- E-commerce platforms dominate distribution channels, enabling consumers to access certified refurbished products with warranty support and transparent pricing.

- Sustainability and circular economy initiatives are encouraging enterprises and governments to adopt refurbished IT equipment as part of ESG strategies.

- Technological innovations in refurbishment, including AI-driven diagnostics and automated component testing, are improving product reliability and scalability.

What are the latest trends in the refurbished computers & laptops market?

Growth of Certified Refurbishment Programs

Major computer manufacturers are expanding official refurbishment programs that allow previously owned devices to be restored and sold with manufacturer-backed warranties. Certified refurbished programs improve product reliability and increase consumer trust, addressing long-standing concerns regarding quality and durability. OEM-led refurbishment initiatives also help manufacturers extend the lifecycle of their products while strengthening customer loyalty and sustainability commitments. These programs are particularly popular among enterprises and educational institutions that prefer certified hardware for procurement compliance and warranty protection.

Expansion of E-Commerce Platforms for Refurbished Electronics

The rapid growth of online marketplaces has significantly increased accessibility to refurbished computers and laptops. E-commerce platforms provide consumers with transparent pricing, warranty coverage, and verified product grading systems. Digital marketplaces also allow refurbishers to reach global customers, particularly in emerging markets where traditional retail channels are limited. Many platforms now offer advanced search filters based on device specifications, condition grades, and price ranges, improving the customer purchasing experience and accelerating online adoption.

What are the key drivers in the refurbished computers & laptops market?

Increasing Demand for Affordable Computing Devices

The rising cost of new laptops and desktops has created strong demand for affordable alternatives. Refurbished computers provide cost savings of up to 60%, making them attractive for students, freelancers, startups, and small businesses. Educational institutions and nonprofit organizations often rely on refurbished systems to deploy large fleets of devices within limited budgets. This affordability advantage continues to drive strong adoption across both developed and emerging markets.

Growing Focus on Sustainability and E-Waste Reduction

The global increase in electronic waste has intensified the need for sustainable electronics lifecycle management. Refurbished devices extend product lifespans and significantly reduce the environmental impact associated with manufacturing new computers. Governments and corporations are increasingly incorporating refurbished IT equipment into procurement strategies as part of environmental, social, and governance (ESG) commitments. Circular economy initiatives that prioritize reuse, repair, and recycling are further strengthening the market outlook.

What are the restraints for the global market?

Consumer Perception and Reliability Concerns

Despite improvements in refurbishment processes, some consumers remain hesitant to purchase refurbished computers due to concerns regarding durability, battery life, and long-term reliability. Negative experiences with poorly refurbished devices in the past have created a perception gap that companies must address through warranty programs, certification standards, and transparent grading systems.

Regulatory Restrictions on Used Electronics Trade

Several countries impose strict regulations on the import and export of used electronics to prevent electronic waste dumping. These regulatory barriers can complicate cross-border trade of refurbished computers and increase compliance costs for refurbishment companies. Export restrictions in certain markets may also limit the ability of refurbishers to serve emerging economies where demand for affordable computing devices is high.

What are the key opportunities in the refurbished computers & laptops industry?

Digital Education and Government Device Programs

Governments worldwide are investing heavily in digital education initiatives that require affordable computing devices for students and teachers. Refurbished laptops provide a cost-efficient solution for deploying large-scale digital classrooms and distance learning programs. Public procurement programs and partnerships with refurbishers can significantly expand the market while improving digital inclusion in developing economies.

Integration of AI-Based Refurbishment Technologies

Technological advancements are transforming refurbishment operations. AI-driven diagnostic systems and automated testing platforms can quickly identify defective components and optimize repair processes. These technologies reduce refurbishment costs, improve quality consistency, and enable refurbishers to scale operations efficiently. Companies investing in automated refurbishment facilities are likely to gain competitive advantages through faster turnaround times and higher product reliability.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 11800 Million |

| Market Size in 2026 | USD 12873.80 Million |

| Market Size in 2031 | USD 19898.97 Million |

| CAGR | 9.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Refurbished laptops dominate the market with an estimated 55% share of global revenue in 2025. Their portability and widespread adoption across remote work and educational environments have made them the most sought-after refurbished computing devices. Refurbished desktop computers represent the second-largest segment, particularly used in enterprise back-office operations and call centers. Workstations and mini PCs are emerging niche segments, primarily serving professional workloads such as design, engineering, and data analytics. Improvements in hardware upgrades, including SSD installations and memory expansion, are enabling older systems to perform competitively with new entry-level devices, further strengthening demand for refurbished products.

Application Insights

Small and medium-sized enterprises (SMEs) represent the largest application segment for refurbished computers, accounting for approximately 32% of market demand. SMEs often prioritize cost-effective IT infrastructure solutions, making refurbished devices an attractive option. The education sector follows closely with around 28% market share, driven by digital learning initiatives and government-funded technology deployment programs. Large enterprises also contribute significantly through internal redeployment and lifecycle management strategies. Nonprofit organizations and government agencies are increasingly adopting refurbished computers to reduce procurement costs while maintaining operational efficiency.

Distribution Channel Insights

E-commerce platforms dominate the distribution of refurbished computers and laptops, accounting for approximately 46% of global sales. Online marketplaces provide easy access to certified refurbished devices, competitive pricing, and consumer protection policies such as return guarantees and warranties. Authorized refurbishment partners and OEM-operated online stores also represent important distribution channels, particularly for certified refurbished products. Corporate IT asset disposition providers serve as a major supply channel by collecting used enterprise devices and channeling them into refurbishment pipelines. Traditional electronics retailers remain relevant in certain markets but are gradually losing share to digital sales platforms.

Explore more data points, trends and opportunities Download Free Sample Report

Refurbished Computers & Laptops Market Segmentations

By Product Type

- Refurbished Laptops

- Refurbished Desktop Computers

- Refurbished Workstations

- Refurbished Mini PCs & Thin Clients

By Application

- Small & Medium Enterprises (SMEs)

- Large Enterprises

- Educational Institutions

- Government & Public Sector

- Non-Profit Organizations

- Individual Consumers

By Distribution Channel

- E-commerce Platforms & Online Marketplaces

- OEM Certified Refurbishment Stores

- Authorized Refurbishment Partners & Resellers

- IT Asset Disposition (ITAD) Providers

- Offline Electronics Retailers

Regional Insights

North America

North America holds the largest share of the refurbished computers & laptops market, accounting for approximately 38% of global revenue in 2025. The United States leads regional demand due to large-scale corporate IT refresh cycles and well-established IT asset disposition programs. Enterprises frequently replace computing devices every three to five years, generating a steady supply of high-quality used hardware for refurbishment. Strong consumer acceptance of refurbished electronics and advanced e-commerce infrastructure further support market growth.

Europe

Europe represents around 27% of the global market, supported by strong regulatory frameworks promoting electronic waste reduction and circular economy practices. Countries such as Germany, the United Kingdom, France, and the Netherlands have established refurbishment ecosystems and high consumer awareness of sustainable electronics consumption. European governments are also actively promoting reuse programs to reduce environmental impact, which is boosting demand for refurbished IT equipment.

Asia-Pacific

Asia-Pacific accounts for roughly 24% of global demand and is the fastest-growing regional market with a projected growth rate exceeding 10%. China, India, Japan, and Southeast Asian economies are experiencing rapid digitalization and increasing demand for affordable computing devices. In particular, India is emerging as a significant growth hub due to expanding startup ecosystems, rising student populations, and strong demand from SMEs.

Latin America

Latin America represents about 5% of global demand, with Brazil and Mexico serving as the region’s primary markets. Demand is largely driven by SMEs and educational institutions seeking cost-efficient computing solutions. The region also imports refurbished devices from North America and Europe to meet growing technology needs.

Middle East & Africa

The Middle East and Africa region accounts for approximately 6% of the global refurbished computers market. Countries such as the United Arab Emirates, Saudi Arabia, and South Africa are major importers of refurbished devices for education and government digitalization programs. Increasing internet penetration and digital transformation initiatives are expected to boost demand in the region over the coming years.

Key Players in the Refurbished Computers & Laptops Market

- Dell Technologies

- HP Inc.

- Lenovo Group Ltd.

- Apple Inc.

- Acer Inc.

- ASUSTeK Computer Inc.

- Microsoft Corporation

- Samsung Electronics

- IBM Corporation

- Best Buy Co. Inc.

- GigaRefurb

- Reboot Systems India Pvt Ltd

- OCM Business Systems Ltd

- RenewedTech

- InterConnection