Refrigerator Market Size

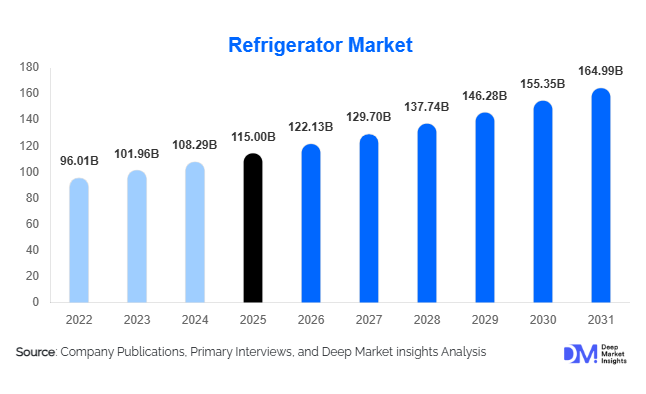

According to Deep Market Insights, the global refrigerator market size was valued at USD 115 billion in 2025 and is projected to grow from USD 122.13 billion in 2026 to reach USD 164.99 billion by 2031, expanding at a CAGR of 6.2% during the forecast period (2026–2031). The refrigerator market growth is primarily driven by rising urbanization, increasing household appliance penetration, and growing demand for energy-efficient and smart refrigeration solutions across both residential and commercial sectors.

Key Market Insights

- Energy-efficient refrigerators are witnessing strong demand, driven by regulatory standards and rising electricity costs globally.

- Smart refrigerators are gaining traction, particularly in developed markets, due to IoT integration and connected home ecosystems.

- Asia-Pacific dominates the market, supported by large population bases and increasing middle-class income levels.

- India and Southeast Asia are the fastest-growing markets, driven by rural electrification and rising appliance adoption.

- Commercial refrigeration demand is expanding, fueled by growth in organized retail, food service, and healthcare sectors.

- Technological advancements, such as inverter compressors and eco-friendly refrigerants, are reshaping product innovation.

What are the latest trends in the refrigerator market?

Smart and Connected Refrigerators

The adoption of smart refrigerators is rapidly increasing, especially in North America and Europe. These appliances integrate IoT features such as remote monitoring, inventory tracking, and voice assistant compatibility. Consumers are increasingly attracted to connected ecosystems that enhance convenience and energy management. Manufacturers are also incorporating AI-driven cooling optimization and predictive maintenance features, improving efficiency and extending product lifespan. This trend is expected to accelerate as smart home adoption expands globally.

Sustainability and Energy Efficiency Focus

Sustainability has become a central theme in product development. Manufacturers are focusing on energy-efficient compressors, low-global-warming-potential refrigerants, and recyclable materials. Regulatory frameworks across regions are mandating higher energy ratings, pushing companies to innovate continuously. Consumers are also showing a strong preference for appliances that reduce energy consumption and environmental impact, making sustainability a key differentiator in purchasing decisions.

What are the key drivers in the refrigerator market?

Rising Urbanization and Household Formation

Rapid urbanization and increasing nuclear family structures are significantly boosting demand for refrigerators. Emerging economies such as India and Indonesia are witnessing strong first-time purchases, while developed markets are driven by replacement demand. Increasing disposable income further supports the adoption of premium and high-capacity models.

Expansion of Food Retail and Cold Chain Infrastructure

The growth of supermarkets, hypermarkets, and food delivery services is driving demand for commercial refrigeration. Cold chain infrastructure expansion, particularly in developing regions, is also contributing to market growth. The healthcare sector, including vaccine storage and pharmaceuticals, adds another layer of demand for specialized refrigeration systems.

What are the restraints for the global market?

High Cost of Advanced Refrigerators

Premium refrigerators with smart features and multi-door configurations remain expensive, limiting adoption in price-sensitive markets. While long-term energy savings are attractive, the initial investment continues to be a barrier for many consumers.

Raw Material Price Volatility

Fluctuations in raw material costs, including steel and electronic components, impact production expenses and pricing. Supply chain disruptions and semiconductor shortages further challenge manufacturers, potentially slowing market growth.

What are the key opportunities in the refrigerator industry?

Emerging Market Penetration

Low penetration rates in regions such as Africa and parts of Asia present significant growth opportunities. Government electrification programs and rising income levels are enabling first-time purchases, particularly for entry-level and mid-range refrigerators.

Smart Appliance Ecosystem Expansion

The growing adoption of smart homes presents opportunities for manufacturers to integrate refrigerators into connected ecosystems. Advanced features such as AI-based food management and remote diagnostics can enhance user experience and create new revenue streams.

Product Type Insights

Top-freezer refrigerators continue to dominate the global market, accounting for approximately 32% of total market share in 2025. Their leadership is primarily driven by affordability, energy efficiency, and strong penetration in emerging economies such as India, Indonesia, and parts of Africa, where first-time buyers prioritize cost-effective solutions. Additionally, their simpler design and lower maintenance requirements make them highly suitable for price-sensitive consumers. Bottom-freezer and side-by-side refrigerators are gaining traction in developed markets such as North America and Europe, where consumers prioritize convenience, ergonomic access, and modern kitchen aesthetics. French door refrigerators represent a rapidly expanding premium segment, driven by increasing demand for large-capacity storage, smart features, and modular shelving systems. These models are particularly popular among urban households with higher disposable incomes.

Compact refrigerators are witnessing rising demand in urban apartments, student housing, and commercial applications such as offices and hospitality. Meanwhile, built-in and integrated refrigerators are expanding within the luxury housing segment, supported by growth in modular kitchens and high-end real estate developments. The overall product landscape is increasingly influenced by consumer preference for convenience, space optimization, and energy efficiency.

Application Insights

The residential segment remains the dominant application area, contributing nearly 72% of total market demand in 2025. This dominance is driven by increasing urbanization, rising disposable incomes, and growing household formation across emerging markets. Replacement demand in developed regions further strengthens this segment, as consumers upgrade to energy-efficient and smart refrigerators.

The commercial segment is growing at a faster pace, supported by the expansion of organized retail, food service chains, and cold storage infrastructure. Supermarkets, hypermarkets, and quick-service restaurants are key contributors to demand. Additionally, the healthcare sector is emerging as a critical growth area, with increasing requirements for pharmaceutical storage, vaccine preservation, and laboratory refrigeration. The diversification of applications across industries is strengthening overall market resilience.

Distribution Channel Insights

Offline retail channels continue to dominate the refrigerator market, accounting for approximately 65% of total sales in 2025. The leading position of offline channels is driven by consumer preference for physical product inspection, brand comparison, and immediate purchase decisions. Retail showrooms and specialty appliance stores play a crucial role in influencing buying behavior, especially in emerging markets.

However, online distribution channels are witnessing rapid growth, supported by increasing digital adoption, competitive pricing, and the availability of flexible financing options such as EMIs and buy-now-pay-later schemes. E-commerce platforms are enhancing customer experience by offering installation services, extended warranties, and easy return policies. The growing trust in online platforms, combined with convenience and wider product selection, is expected to significantly increase their market share over the forecast period.

End-Use Insights

Residential end-use remains the primary demand driver, supported by increasing household formation, urban migration, and rising living standards. Replacement cycles in mature markets and first-time purchases in developing regions continue to sustain demand. The growing preference for smart and energy-efficient appliances is further boosting residential adoption.

The commercial segment is expected to grow at a faster rate, driven by expansion in food service, hospitality, and retail sectors. Increasing investments in cold chain logistics, particularly in developing economies, are significantly contributing to commercial refrigeration demand. Healthcare infrastructure development is also playing a critical role, with rising demand for specialized refrigeration systems for medical and pharmaceutical applications. Export-driven demand from manufacturing hubs such as China and Thailand further supports global market growth.

| By Product Type | By Application | By Distribution Channel | By Technology | By Capacity |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

Asia-Pacific

Asia-Pacific leads the global refrigerator market, accounting for approximately 45% of the total market share in 2025. China dominates the region due to its strong manufacturing base, great domestic demand, and export capabilities. India is the fastest-growing market, supported by rising disposable incomes, government-led rural electrification programs, and increasing penetration of household appliances. Southeast Asian countries such as Indonesia, Vietnam, and Thailand are also witnessing robust growth due to rapid urbanization, expanding middle-class populations, and improving retail infrastructure. Additionally, favorable government initiatives promoting domestic manufacturing and energy-efficient appliances are accelerating regional growth.

North America

North America accounts for around 20% of the global market, with the United States representing the largest share. Growth in this region is primarily driven by high product penetration, strong replacement demand, and increasing adoption of premium and smart refrigerators. Consumers in North America show a strong preference for technologically advanced appliances, including IoT-enabled and energy-efficient models. The presence of established manufacturers, advanced retail networks, and high consumer purchasing power further supports market stability and growth.

Europe

Europe holds approximately 18% market share, with key markets including Germany, the United Kingdom, and France. The region’s growth is largely driven by stringent environmental regulations and strong consumer awareness regarding energy efficiency. Demand for eco-friendly appliances with low energy consumption and sustainable refrigerants is particularly high. Additionally, the trend toward compact living spaces in urban areas is driving demand for space-efficient and integrated refrigerator solutions. Government incentives promoting energy-efficient appliances further contribute to market expansion.

Latin America

Latin America contributes around 8% of the global market, with Brazil and Mexico leading demand. Growth in the region is supported by improving economic conditions, increasing urbanization, and the expansion of the middle-class population. The rising penetration of organized retail and the availability of consumer financing options are also driving refrigerator adoption. Additionally, climatic conditions in many parts of the region necessitate refrigeration for food preservation, further supporting demand growth.

Middle East & Africa

The Middle East & Africa region accounts for approximately 9% of the global market. Growth is driven by rapid urbanization, infrastructure development, and increasing demand for modern household appliances. Countries such as the UAE and Saudi Arabia are key contributors, supported by high disposable incomes and strong demand for premium appliances. In Africa, rising electrification rates and improving living standards are enabling first-time purchases, particularly in urban and semi-urban areas. Additionally, extreme climatic conditions in the region create a strong need for reliable refrigeration solutions, further driving market expansion.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Refrigerator Market

- Whirlpool Corporation

- Samsung Electronics

- LG Electronics

- Haier Smart Home

- Electrolux AB

- Panasonic Corporation

- Hitachi Appliances

- Bosch (BSH Hausgeräte)

- Sharp Corporation

- Toshiba Lifestyle Products

- Midea Group

- Hisense Group

- GE Appliances

- Godrej Appliances

- Liebherr Group