Projector Market Size

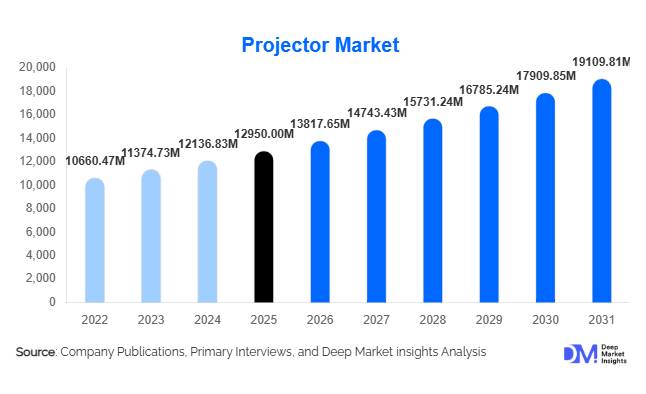

According to Deep Market Insights,the global projector market size was valued at USD 12,950 million in 2025 and is projected to grow from USD 13,817.65 million in 2026 to reach USD 19,109.81 million by 2031, expanding at a CAGR of 6.7% during the forecast period (2026–2031). The projector market growth is primarily driven by the rising demand for large-format visual display solutions across education, corporate collaboration, and entertainment environments. Increasing adoption of laser and LED projection technologies, coupled with the expansion of digital cinema infrastructure and home theater ecosystems, is strengthening long-term market growth.

Projectors continue to play a critical role in environments where large-scale displays are required, such as classrooms, conference halls, theaters, museums, and large venues. Advancements in high-brightness laser projectors, wireless connectivity, and smart projection systems have significantly improved image quality, operational efficiency, and ease of deployment. Additionally, growing demand for immersive gaming, projection mapping in entertainment venues, and hybrid work collaboration technologies is expanding the market’s application landscape. As organizations upgrade legacy lamp-based systems to energy-efficient laser projectors and consumers increasingly adopt compact smart projectors for home entertainment, the global projector market is expected to experience steady expansion over the coming years.

Key Market Insights

- Laser projection technology is rapidly replacing lamp-based projectors due to longer operational life, reduced maintenance costs, and superior brightness performance.

- Asia-Pacific dominates the global market, supported by strong electronics manufacturing ecosystems and large-scale demand from China, Japan, South Korea, and India.

- Education and corporate collaboration remain the largest application segments, collectively accounting for a significant portion of global projector installations.

- Ultra-short throw projectors are gaining traction in home entertainment and classroom environments due to their ability to produce large images from minimal distances.

- Home theater and gaming applications are expanding rapidly, fueled by streaming platforms and immersive content consumption trends.

- Technological integration including wireless connectivity and smart OS platforms is transforming projectors into standalone entertainment and collaboration devices.

What are the latest trends in the projector market?

Rapid Adoption of Laser Projection Systems

Laser-based projection systems are becoming the fastest-growing technology segment in the projector industry. Unlike traditional lamp-based systems that require periodic replacement and maintenance, laser projectors provide lifespans exceeding 20,000 hours while delivering higher brightness and superior color accuracy. These advantages have made them increasingly popular in cinemas, large venues, universities, and corporate environments. Declining costs of laser light modules are also enabling mid-range projector manufacturers to integrate laser technology into their product portfolios. As organizations seek lower total cost of ownership and improved operational reliability, laser projectors are expected to gradually replace conventional lamp-based systems across multiple application segments.

Rise of Smart and Portable Projectors

The increasing popularity of portable and smart projectors represents another key industry trend. Modern projectors now integrate operating systems, wireless connectivity, and streaming services, allowing users to access content without requiring additional hardware. Compact pico projectors and portable LED models are gaining traction among consumers seeking flexible entertainment solutions for small apartments, outdoor movie nights, and travel use. Manufacturers are focusing on improving battery performance, wireless casting capabilities, and smart assistant integration to enhance user experience. These advancements are transforming projectors from traditional presentation tools into versatile multimedia devices that support gaming, streaming, and collaborative work.

What are the key drivers in the projector market?

Growing Demand for Large-Screen Display Solutions

The increasing need for large-format displays across education, corporate collaboration, and entertainment environments is a major growth driver for the projector market. Projectors enable organizations to deliver visual content on large surfaces without requiring expensive large-format screens. Educational institutions rely heavily on projectors for multimedia learning, while corporations use them for presentations, training sessions, and conference room collaboration. Large venues such as auditoriums, museums, and event spaces also require high-lumen projectors capable of producing clear visuals over large projection areas. As digital communication and visual content consumption continue to grow globally, demand for projector technology is expected to remain strong.

Expansion of Digital Cinema Infrastructure

The global expansion of digital cinema infrastructure has significantly boosted demand for high-brightness projectors. Modern cinemas require advanced projection systems capable of delivering ultra-high-definition visuals and high dynamic range imaging. Laser projectors have become the preferred solution for cinema chains due to their brightness stability and lower operational costs compared with lamp-based models. Emerging markets in Asia-Pacific and the Middle East are investing heavily in multiplex cinema development, creating additional opportunities for projector manufacturers specializing in professional-grade projection equipment.

What are the restraints for the global market?

Competition from Large-Format LED Displays

One of the major restraints affecting the projector market is the rapid adoption of large-format LED and LCD displays. Declining prices of large display panels have made them a viable alternative for classrooms and corporate meeting rooms. Unlike projectors, LED displays offer consistent brightness in well-lit environments and require minimal setup. As a result, some organizations are transitioning toward flat-panel display solutions, especially for smaller rooms and collaborative workspaces.

Operational and Environmental Limitations

Traditional projectors, particularly lamp-based models, require periodic maintenance and lamp replacement, increasing operating costs. Additionally, projection quality may be affected by ambient lighting conditions, making them less effective in brightly lit environments. Although newer laser and LED projectors have improved performance, these limitations still influence purchasing decisions in certain applications where display panels may offer greater convenience.

What are the key opportunities in the projector industry?

Growth of Home Theater and Gaming Projection

The rising popularity of home entertainment ecosystems presents a major opportunity for projector manufacturers. Consumers increasingly seek cinematic viewing experiences within their homes, driven by streaming platforms and high-resolution content. Ultra-short throw projectors capable of delivering 100–150 inch displays in compact spaces are gaining strong traction among home theater enthusiasts. Gaming applications are also emerging as a promising growth area, as next-generation gaming consoles require high-resolution displays with minimal latency. Manufacturers that develop low-latency, high-refresh-rate projectors can capture growing demand from gaming communities worldwide.

Digital Transformation in Education

Governments and educational institutions around the world are investing heavily in digital classroom infrastructure, creating significant opportunities for projector manufacturers. Interactive projectors, wireless presentation tools, and hybrid learning technologies are becoming standard features in modern classrooms. Large-scale education modernization initiatives in Asia-Pacific and the Middle East are particularly driving demand for advanced projection systems. Companies that integrate interactive features, cloud connectivity, and collaboration software into projector systems are well positioned to benefit from this growing market segment.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 12950 Million |

| Market Size in 2026 | USD 13817.65 Million |

| Market Size in 2031 | USD 19109.81 Million |

| CAGR | 6.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Technology Insights

DLP (Digital Light Processing) projectors dominate the global projector market, accounting for approximately 42% of the total market share in 2025. The strong market position of DLP technology is largely driven by its ability to deliver high image sharpness, superior contrast ratios, and long operational durability compared with many alternative projection technologies. These advantages make DLP projectors particularly well suited for corporate presentation environments, digital cinema installations, and portable projection devices used in professional and educational settings. The use of micro-mirror semiconductor chips enables DLP systems to produce highly stable and consistent visuals, which has contributed to their widespread adoption in commercial audiovisual environments where reliability and performance are critical.

LCD projectors continue to maintain a significant presence across the market, particularly within the education sector where affordability and consistent color accuracy are important considerations. LCD projection technology is commonly used in classrooms, training centers, and conference rooms due to its ability to produce vibrant colors and clear images at relatively lower acquisition costs. In addition, LCD projectors are widely available across a broad range of brightness levels and form factors, enabling institutions with varying budgets to deploy large-scale projection systems across multiple facilities.

Meanwhile, LCoS (Liquid Crystal on Silicon) projection technology is gaining traction in premium home theater installations and high-end visualization applications. LCoS systems offer extremely high resolution and improved pixel density, resulting in smoother images and superior color reproduction that appeal to consumers seeking cinematic-quality home entertainment experiences. As home entertainment technology continues to evolve, demand for high-performance projection systems capable of delivering immersive visual experiences is increasing.

Another important technological development shaping the projector market is the increasing adoption of laser and LED light sources. These advanced illumination technologies are being integrated into both DLP and LCD platforms to enhance brightness performance, extend product lifecycles, and significantly reduce maintenance requirements associated with traditional lamp-based projectors. Laser projectors in particular offer longer operational lifespans and faster start-up times, which are highly valued in commercial installations such as digital cinema, museums, and event venues. As manufacturers continue to improve energy efficiency and performance capabilities, the integration of solid-state light sources is expected to further strengthen the competitiveness of modern projection systems.

Resolution Insights

Full HD projectors represent the largest resolution segment in the global projector market, accounting for nearly 34% of total market share in 2025. The leading position of this segment is primarily driven by the strong balance that Full HD resolution offers between cost efficiency and visual clarity. Organizations across corporate offices, educational institutions, and training facilities widely adopt Full HD projectors because they deliver sufficiently sharp image quality for presentations, instructional content, and multimedia demonstrations while remaining relatively affordable compared with ultra-high-definition alternatives.

The compatibility of Full HD resolution with most modern digital content formats further supports its widespread adoption across a wide range of applications. Businesses conducting video conferencing, product demonstrations, and corporate training sessions often prefer Full HD projection systems because they provide reliable image performance without requiring significant infrastructure upgrades or high equipment costs. Additionally, many home entertainment users continue to choose Full HD projectors for casual movie viewing and gaming experiences, reinforcing the segment’s strong market share.

Although Full HD remains the dominant resolution category, 4K projectors are experiencing the fastest growth across the industry. Increasing consumer expectations for ultra-high-definition visuals, combined with the expansion of digital cinema and advanced gaming platforms, are accelerating demand for 4K projection systems. The entertainment industry in particular is driving the transition toward higher-resolution projection technologies, as cinemas, simulation centers, and immersive entertainment venues seek to deliver more realistic and engaging visual experiences.

As component manufacturing costs gradually decline and display technologies continue to evolve, 4K projectors are becoming more accessible to a broader range of consumers and organizations. Over the coming years, the adoption of ultra-high-definition projection systems is expected to increase steadily, particularly in premium home theaters, professional visualization environments, and digital cinema applications.

Brightness Insights

Projectors with brightness levels between 3,000 and 4,999 lumens dominate the global market, representing approximately 31% of total demand in 2025. The leadership of this segment is largely driven by its suitability for a wide range of everyday projection environments such as classrooms, meeting rooms, training facilities, and small to medium-sized conference venues. These brightness levels provide sufficient illumination to ensure clear and readable visuals in moderately lit environments without requiring excessive power consumption or expensive hardware components.

The versatility of projectors within this brightness range has made them a preferred choice for educational institutions and corporate organizations seeking reliable presentation tools that can operate effectively in multipurpose environments. Institutions deploying projectors across large numbers of rooms often favor this brightness category because it delivers strong performance while maintaining manageable acquisition and operating costs.

Lower brightness projectors below 3,000 lumens are typically used in controlled lighting conditions such as home theaters or small office spaces where ambient light is limited. In contrast, high-brightness projectors exceeding 10,000 lumens are designed for large-scale venues including auditoriums, concert halls, outdoor events, and advanced projection mapping installations. These high-performance systems are capable of producing extremely bright visuals over large surfaces, making them essential for entertainment venues, public events, and large exhibition displays.

As immersive entertainment experiences and large-scale visual displays become more popular across industries such as tourism, advertising, and live events, demand for professional high-lumen projectors is expected to grow steadily in the coming years.

Application Insights

Education and corporate presentation applications collectively represent nearly 40% of total global projector demand, making them the leading application segment within the industry. The dominance of this segment is primarily driven by the critical role projection systems play in facilitating effective communication, training, and knowledge sharing across professional and academic environments. Classrooms, lecture halls, corporate meeting rooms, and training centers rely heavily on projection technology to deliver multimedia content, support collaborative discussions, and enhance audience engagement during presentations.

The continued digital transformation of education systems around the world is further strengthening demand for projection technologies. Governments and educational institutions are increasingly investing in smart classroom infrastructure that integrates projectors with interactive whiteboards, digital content platforms, and remote learning tools. These initiatives are significantly expanding the deployment of projection systems across primary schools, universities, and professional training facilities.

Digital cinema represents another major application segment within the projector market. As film production companies and theater operators transition toward advanced digital formats, cinemas are upgrading their projection infrastructure to laser-based systems capable of delivering ultra-high-definition visuals with improved brightness and color accuracy. These upgrades enhance the cinematic experience for audiences while also reducing operational maintenance requirements for theater operators.

In addition to these established applications, projector technologies are increasingly being used in emerging fields such as projection mapping, immersive retail displays, simulation training environments, and healthcare visualization. Museums, theme parks, and large event venues are adopting projection mapping techniques to create visually engaging experiences that combine architecture with dynamic digital content. Similarly, simulation training platforms used in aviation, defense, and medical education rely on high-performance projection systems to create realistic training environments.The expansion of these innovative applications is significantly increasing the overall addressable market for projector manufacturers and encouraging ongoing technological advancements across the industry.

Explore more data points, trends and opportunities Download Free Sample Report

Projector Market Segmentations

By Technology

- DLP (Digital Light Processing) Projectors

- LCD (Liquid Crystal Display) Projectors

- LCoS (Liquid Crystal on Silicon) Projectors

- LED Projectors

- Laser Projectors

- Hybrid Laser-LED Projectors

By Resolution

- SVGA

- XGA

- WXGA

- Full HD

- WUXGA

- 4K UHD

- 8K Projectors

By Brightness Level

- Below 1,000 Lumens

- 1,000 – 2,999 Lumens

- 3,000 – 4,999 Lumens

- 5,000 – 9,999 Lumens

- 10,000 Lumens and Above

By Projection Type

- Standard Throw Projectors

- Short Throw Projectors

- Ultra-Short Throw Projectors

By Application

- Business & Corporate Presentations

- Education & Classroom Learning

- Home Theater / Entertainment

- Gaming

- Digital Cinema

- Large Venue & Events

- Simulation & Visualization

- Healthcare Imaging

- Retail & Digital Signage

By Distribution Channel

- Online Retail

- Electronics and Specialty Stores

- Direct Sales / B2B Channels

- System Integrators & AV Solution Providers

Regional Insights

North America

North America accounts for approximately 26% of the global projector market, with the United States representing the largest national market in the region. Strong demand for home theater systems, corporate collaboration technologies, and digital cinema infrastructure continues to support market expansion. The region benefits from high consumer purchasing power and a mature entertainment industry that consistently adopts advanced audiovisual technologies.

Corporate organizations across North America are increasingly investing in modern collaboration environments that integrate projection systems with video conferencing platforms, wireless presentation technologies, and interactive display tools. These upgrades are driving steady demand for high-performance projectors across office spaces, conference centers, and training facilities.

The region also maintains a well-established digital cinema ecosystem, with theaters regularly upgrading projection systems to laser-based and ultra-high-definition formats. In addition, the growing popularity of home entertainment systems, gaming platforms, and streaming services is encouraging consumers to invest in premium home theater projectors. Canada further contributes to regional demand through educational institutions, professional audiovisual installations, and government investments in modern classroom technologies.

Europe

Europe represents nearly 21% of the global projector market, with major demand centers including Germany, the United Kingdom, France, and Italy. The region's strong corporate infrastructure and advanced audiovisual integration across business environments are key factors supporting steady market growth. Many European companies are upgrading traditional meeting rooms into smart collaboration spaces that incorporate high-quality projection systems, wireless connectivity, and integrated communication tools.

The cinema industry also plays an important role in supporting projector demand across Europe. Theater operators throughout the region are gradually replacing conventional lamp-based projectors with advanced laser projection systems to improve image quality, energy efficiency, and operational reliability. These upgrades are helping cinemas deliver enhanced viewing experiences while reducing long-term maintenance costs.

Consumer interest in premium home entertainment technologies further contributes to regional growth. Western European households increasingly adopt advanced audiovisual systems including large-screen projectors, surround sound systems, and smart home entertainment platforms. This trend is particularly strong in markets with high disposable incomes and strong digital content consumption.

Asia-Pacific

Asia-Pacific dominates the global projector market with approximately 41% share in 2025, making it the largest regional market worldwide. Rapid technological development, strong electronics manufacturing capabilities, and expanding demand across education, entertainment, and corporate sectors are key drivers of regional growth.

China represents the largest national market in the region, accounting for nearly 22% of global projector demand. The country's extensive consumer electronics manufacturing ecosystem allows domestic companies to produce projection technologies at competitive costs, while strong demand from educational institutions and cinema operators continues to support widespread adoption.

Japan and South Korea remain important innovation hubs for projection technologies, with leading electronics companies continuously developing advanced projection systems featuring improved resolution, brightness performance, and laser illumination technologies. These technological advancements often influence global industry standards and product development strategies.

India is emerging as one of the fastest-growing markets within the region. Government-led digital classroom initiatives, expanding educational infrastructure, and rising demand for home entertainment systems among urban consumers are accelerating projector adoption across the country. Additionally, the rapid expansion of multiplex cinema chains and entertainment venues across major Asian cities is further strengthening regional market growth.

Latin America

Latin America represents a smaller but steadily expanding projector market, with Brazil and Mexico serving as the primary demand centers. Economic development and increasing investments in education infrastructure are encouraging the adoption of projection technologies across schools, universities, and corporate training facilities.

The cinema industry is also expanding across the region as multiplex operators introduce new theater locations in growing urban areas. These venues require modern digital projection systems capable of delivering high-quality visual experiences to audiences. As a result, cinema expansion is contributing to rising demand for professional-grade projectors.

Additionally, corporate modernization initiatives across sectors such as finance, telecommunications, and technology are driving the adoption of audiovisual presentation equipment within offices and conference facilities. The growing middle-class population and rising interest in home entertainment technologies are also supporting the gradual adoption of home theater projectors across the region.

Middle East & Africa

The Middle East and Africa region is experiencing increasing demand for projection technologies as governments and private investors expand entertainment, tourism, and education infrastructure. Countries such as the United Arab Emirates and Saudi Arabia are undertaking large-scale entertainment and tourism development projects that incorporate advanced audiovisual installations, including high-brightness projection systems for events, exhibitions, and immersive experiences.

Major entertainment venues, museums, and cultural attractions in the region are increasingly utilizing projection mapping technologies to create engaging visual displays that attract both domestic and international visitors. These developments are creating new opportunities for projector manufacturers specializing in high-lumen and large-scale projection systems.

Government investments in digital education initiatives are also contributing to the adoption of classroom projection systems across schools and universities. In several African countries, modernization of educational infrastructure and the gradual expansion of cinema networks are supporting the growth of projector installations. While the region remains at an earlier stage of market development compared with other global regions, ongoing infrastructure investments and expanding entertainment industries are expected to drive steady growth in projector demand over the coming years.

Key Players in the Projector Market

- Seiko Epson Corporation

- BenQ Corporation

- Sony Corporation

- Panasonic Holdings Corporation

- NEC Corporation

- ViewSonic Corporation

- Optoma Corporation

- LG Electronics

- XGIMI Technology Co., Ltd.

- Casio Computer Co., Ltd.

- Acer Inc.

- Canon Inc.

- Sharp Corporation

- Christie Digital Systems

- Barco NV