Professional Golf Market Size

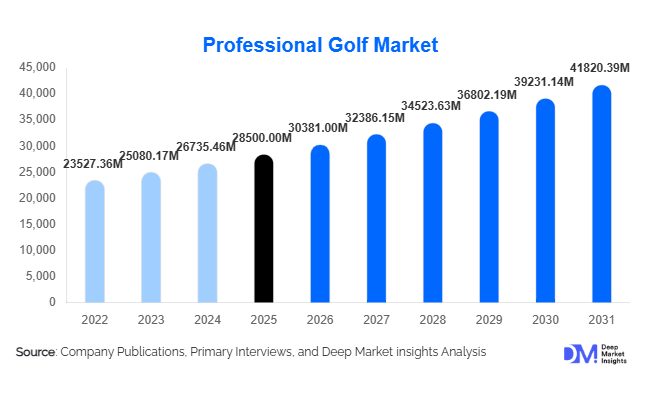

According to Deep Market Insights, the global professional golf market size was valued at USD 28,500 million in 2025 and is projected to grow from USD 30,381.00 million in 2026 to reach USD 41,820.39 million by 2031, expanding at a CAGR of 6.6% during the forecast period (2026–2031). The professional golf market growth is primarily driven by rising media rights valuations, increasing sponsorship investments, and the globalization of tournaments across emerging regions. The expansion of digital streaming platforms and the introduction of new competitive formats have further strengthened commercial opportunities within the ecosystem.

Key Market Insights

- Media and broadcasting rights dominate revenue generation, accounting for over 30% of the global market, driven by long-term contracts and digital streaming expansion.

- North America leads the market, supported by established tours, high sponsorship spending, and a mature fan base.

- Asia-Pacific is the fastest-growing region, fueled by infrastructure investments and increasing participation in countries such as China, India, and South Korea.

- Emerging golf leagues are reshaping competition, increasing prize pools, and intensifying player and sponsor engagement.

- Corporate hospitality is a high-margin segment, with premium event experiences driving strong revenue growth.

- Technology adoption is accelerating, including data analytics, immersive broadcasting, and fan engagement tools.

What are the latest trends in the professional golf market?

Digital Transformation and Streaming Expansion

The professional golf market is witnessing a strong shift toward digital consumption, with OTT platforms and streaming services gaining prominence over traditional broadcasting. Fans increasingly prefer on-demand viewing, multi-angle coverage, and real-time analytics, enhancing engagement levels. This transition is enabling leagues and tournament organizers to tap into younger demographics while unlocking new advertising and subscription-based revenue streams. Interactive features such as live player tracking, shot analytics, and personalized viewing experiences are becoming standard offerings.

Emergence of Alternative Formats and New Leagues

The introduction of shorter, team-based formats and new professional leagues is transforming the competitive landscape. These formats cater to modern audiences seeking faster-paced entertainment, thereby increasing viewership and sponsorship opportunities. The entry of new leagues has also led to higher prize pools and innovative tournament structures, creating a more dynamic and competitive environment within professional golf.

What are the key drivers in the professional golf market?

Growth in Media Rights and Broadcasting Revenues

The increasing value of media rights agreements is a major growth driver for the professional golf market. Global broadcasters and streaming platforms are competing for exclusive rights, resulting in higher revenues for tours and tournament organizers. This trend is supported by expanding global audiences and the growing popularity of live sports content.

Rising Sponsorship and Brand Investments

Professional golf continues to attract significant sponsorship investments due to its premium positioning and affluent audience base. Global brands, particularly in luxury goods, automotive, and financial services, are leveraging golf tournaments for brand visibility and customer engagement. Long-term sponsorship agreements and title partnerships are contributing significantly to market growth.

What are the restraints for the global market?

High Operational and Infrastructure Costs

Organizing professional golf tournaments requires substantial investments in course maintenance, logistics, and event management. These high costs can limit profitability, particularly for smaller tours and emerging markets, posing a challenge to market expansion.

Fragmentation and Competitive Conflicts

The emergence of multiple leagues and governing bodies has led to fragmentation within the professional golf ecosystem. Player participation conflicts and inconsistent regulations can impact audience engagement and create uncertainties for sponsors and stakeholders.

What are the key opportunities in the professional golf industry?

Expansion into Emerging Markets

Emerging regions such as the Asia-Pacific and the Middle East present significant growth opportunities for the professional golf market. Increasing investments in golf infrastructure, rising disposable incomes, and government support for international tournaments are driving demand. These markets offer untapped potential for audience expansion and sponsorship growth.

Technology Integration and Fan Engagement

The adoption of advanced technologies, including artificial intelligence, augmented reality, and data analytics, is creating new opportunities for enhancing fan engagement. Interactive platforms and immersive viewing experiences are attracting younger audiences and increasing overall market participation.

Growth in Corporate Hospitality

Corporate hospitality is emerging as a lucrative segment within the professional golf market. High-value networking opportunities, premium event experiences, and exclusive access packages are driving demand from corporate clients. This segment offers strong revenue potential due to its high-margin nature and repeat business opportunities.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 28500 Million |

| Market Size in 2026 | USD 30381 Million |

| Market Size in 2031 | USD 41820.39 Million |

| CAGR | 6.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Major global tours continue to dominate the professional golf market, accounting for approximately 45% of total revenue in 2025. Their leadership is primarily driven by high-value media rights agreements, significantly larger prize pools, and long-standing sponsorship ecosystems that attract elite players and global audiences. These tours benefit from strong brand equity and legacy positioning, enabling them to command premium advertising rates and secure multi-year commercial partnerships. Additionally, their global event calendars and established fan bases ensure consistent revenue generation across multiple channels.

Regional and developmental tours play a critical supporting role in market expansion by developing emerging talent pipelines and expanding the sport’s geographic reach. These tours are increasingly gaining attention from sponsors and broadcasters as they penetrate untapped markets, particularly in the Asia-Pacific and Latin America. Women’s professional tours are witnessing accelerated growth, driven by increasing gender inclusivity initiatives, rising sponsorship interest, and improved media visibility. The growing emphasis on diversity and equal prize distribution is expected to further enhance the commercial viability of this segment over the forecast period.

Application Insights

Media and broadcasting applications represent the largest segment, contributing approximately 32% of the total market share in 2025. This dominance is driven by the rapid expansion of OTT platforms, increasing global demand for live sports content, and rising competition among broadcasters for exclusive rights. Enhanced viewer experiences through real-time analytics, multi-angle coverage, and interactive features are further strengthening this segment’s growth trajectory.

Sponsorship and advertising applications are the second-largest contributors, fueled by strong brand alignment with golf’s premium audience and high engagement levels during tournaments. Global brands, particularly in luxury goods, automotive, and financial services, are increasingly investing in golf to enhance brand visibility and customer engagement. Meanwhile, merchandising and licensing are gaining traction as fan engagement deepens, supported by growing demand for branded apparel, equipment, and collectibles. This segment is benefiting from digital commerce platforms and direct-to-consumer sales strategies.

Distribution Channel Insights

Digital platforms dominate the distribution landscape, with streaming services and online broadcasting accounting for the majority of global viewership. This shift is driven by changing consumer preferences toward on-demand content, mobile accessibility, and personalized viewing experiences. OTT platforms are increasingly offering subscription-based models, interactive features, and global accessibility, making them the preferred choice among younger audiences.

Traditional television continues to hold a significant share, particularly among older demographics and in regions with limited digital infrastructure. However, it is gradually уступed by digital channels due to limited interactivity and declining linear viewership. Direct event ticketing and corporate sales channels remain crucial for revenue generation, especially for high-profile tournaments. The growth of premium hospitality packages and corporate partnerships is further strengthening these offline distribution channels.

End-Use Insights

The sports entertainment industry remains the primary end-use segment, driven by global fan engagement, increasing viewership, and the commercialization of professional golf tournaments. This segment benefits from diversified revenue streams, including ticket sales, broadcasting rights, and sponsorships, making it the backbone of the market.

The media and broadcasting industry is the fastest-growing end-use segment, projected to expand at a CAGR exceeding 7% during the forecast period. This growth is fueled by rising demand for live sports content, increasing digital subscriptions, and the expansion of global streaming platforms. Corporate hospitality and tourism sectors are also significant contributors, as professional golf events attract high-net-worth individuals, international tourists, and corporate clients seeking premium networking experiences. Emerging applications in sports tourism, experiential entertainment, and destination marketing are further expanding the market’s reach, particularly in developing economies.

Explore more data points, trends and opportunities Download Free Sample Report

Professional Golf Market Segmentations

Product Type

- Major Global Tours

- Regional Professional Tours

- Developmental Tours

- Women’s Professional Tours

Application

- Media & Broadcasting

- Sponsorship & Advertising

- Merchandising & Licensing

- Event Ticketing & Hospitality

Distribution Channel

- Digital Streaming Platforms (OTT)

- Television Broadcasting

- Direct Event Ticketing

- Corporate & Hospitality Sales

End-Use

- Sports Entertainment Industry

- Media & Broadcasting Industry

- Corporate Hospitality

- Sports Tourism & Experiential Entertainment

Regional Insights

North America

North America leads the global professional golf market, accounting for approximately 40% of total market share in 2025, with the United States as the dominant contributor. The region’s leadership is driven by well-established professional tours, high media rights valuations, and a mature sponsorship ecosystem. Strong corporate participation, particularly from financial services and luxury brands, continues to drive revenue growth. Additionally, the presence of world-class golf infrastructure and a large, engaged fan base supports consistent demand. Technological innovation in broadcasting and analytics further enhances the region’s competitive advantage.

Europe

Europe holds around 25% of the global market share, with key contributions from the United Kingdom, Germany, and Spain. The region benefits from historic tournaments, strong cultural affinity for golf, and a well-developed player base. Growth is supported by increasing sponsorship investments and rising interest in sustainable and experiential sports events. European markets are also witnessing growing adoption of digital streaming platforms, which is expanding audience reach and enhancing revenue opportunities.

Asia-Pacific

Asia-Pacific accounts for approximately 20% of the market and is the fastest-growing region, with a CAGR exceeding 8%. Growth in this region is driven by rapid urbanization, rising disposable incomes, and significant investments in golf infrastructure. Countries such as China, Japan, South Korea, and India are emerging as key markets due to increasing participation and government support for international tournaments. The expansion of middle-class populations and growing interest in premium sports entertainment are further accelerating demand. Additionally, the region is benefiting from strategic partnerships with global tours and increasing corporate sponsorships.

Latin America

Latin America contributes approximately 7% of the global market, with Brazil and Mexico leading regional demand. Growth in this region is supported by rising interest in golf as a leisure and professional sport, increasing tourism, and the development of regional tournaments. While the market is still emerging, improving economic conditions and growing middle-class participation are expected to drive future expansion. Investments in sports infrastructure and international event hosting are also contributing to market development.

Middle East & Africa

The Middle East & Africa region holds about 8% of the global market share, with the UAE and Saudi Arabia as key contributors. Growth in this region is driven by significant government investments in sports infrastructure, strategic positioning as global sporting hubs, and the hosting of high-profile international tournaments. The Middle East, in particular, is leveraging golf as part of broader economic diversification strategies, attracting global players and sponsors. Africa continues to play a vital role as a host region, benefiting from natural golf landscapes, tourism-driven demand, and international tournament circuits. Increasing investments in hospitality and sports tourism are expected to further strengthen the region’s market position.