Preschool Market Size

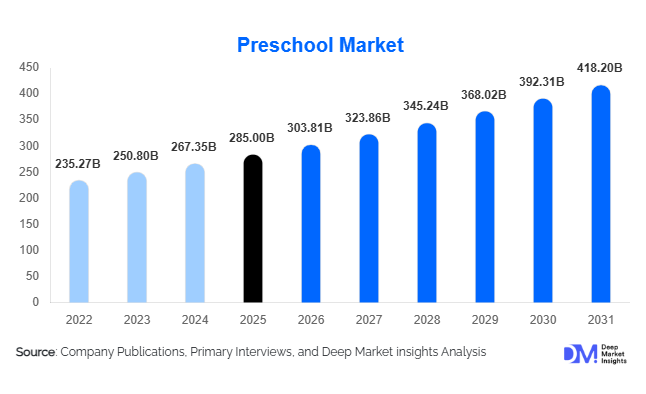

According to Deep Market Insights, the global preschool market size was valued at USD 285 billion in 2025 and is projected to grow from USD 303.81 billion in 2026 to reach USD 418.20 billion by 2031, expanding at a CAGR of 6.6% during the forecast period (2026–2031). The preschool market growth is primarily driven by rising awareness of early childhood education, increasing participation of women in the workforce, and strong government support for structured early learning programs worldwide.

Key Market Insights

- Private preschools dominate the global market, accounting for over 55% of total revenue due to higher perceived quality and standardized curricula.

- Asia-Pacific is the fastest-growing region, driven by rising population, urbanization, and expanding middle-class income.

- Hybrid learning models are gaining traction, combining physical classrooms with digital engagement tools for enhanced learning outcomes.

- Franchise-based preschool chains are expanding rapidly, particularly in emerging economies, due to scalability and brand recognition.

- Mid-range fee structures dominate globally, offering a balance between affordability and quality, capturing nearly 45% market share.

- Employer-sponsored childcare is emerging as a high-growth segment, supporting workforce productivity and retention.

What are the latest trends in the preschool market?

Digital and Hybrid Learning Integration

Preschool education is increasingly integrating digital tools into traditional classroom settings. Hybrid learning models, combining offline and online engagement, are gaining popularity among urban parents. Interactive apps, gamified learning platforms, and AI-based developmental tracking tools are being adopted to enhance cognitive development and personalize learning experiences. This trend is particularly prominent in developed markets and urban centers of emerging economies, where parents demand transparency, engagement, and measurable outcomes. Digital platforms are also improving parent-teacher communication, enabling real-time progress tracking and increasing overall satisfaction.

Rise of Branded and Franchise Preschool Chains

The preschool market is witnessing the rapid expansion of franchise-based and branded chains that offer standardized curricula, infrastructure, and operational models. These chains are particularly successful in emerging markets where demand is rising but quality supply remains inconsistent. Franchise models allow for rapid geographic expansion while maintaining brand consistency and quality standards. Investors are increasingly attracted to this model due to its scalability, predictable revenue streams, and relatively lower risk compared to independent setups.

What are the key drivers in the preschool market?

Increasing Female Workforce Participation

The rise in dual-income households globally has significantly boosted demand for structured preschool education. Working parents require reliable and safe environments for early childhood care, making preschools an essential service. This trend is especially strong in urban areas across Asia-Pacific, North America, and Europe, where workforce participation among women continues to grow steadily.

Growing Awareness of Early Childhood Development

Scientific research emphasizing the importance of early cognitive and social development has influenced parental preferences worldwide. Preschool education is increasingly viewed as a critical foundation for lifelong learning. Governments and institutions are actively promoting early education, leading to higher enrollment rates and increased spending on quality preschool services.

What are the restraints for the global market?

High Operational and Infrastructure Costs

Establishing and maintaining preschool facilities requires significant investment in infrastructure, safety compliance, and trained staff. These high operational costs can limit expansion, particularly in cost-sensitive markets where affordability is a major concern.

Regulatory and Quality Compliance Challenges

The preschool sector is subject to strict regulations related to safety, curriculum, and teacher qualifications. Variations in regulatory frameworks across regions create challenges for providers aiming to scale operations globally. Compliance costs and operational complexities can act as barriers to entry and expansion.

What are the key opportunities in the preschool industry?

Expansion in Emerging Markets

Emerging economies such as India, Indonesia, and parts of Africa present significant growth opportunities due to low preschool penetration rates. Increasing government focus on early childhood education and rising disposable incomes are creating favorable conditions for private sector participation. Expansion into tier-2 and tier-3 cities offers untapped potential for scalable and affordable preschool models.

Corporate and Employer-Sponsored Childcare

Organizations are increasingly investing in childcare facilities to support employee productivity and retention. Employer-sponsored preschool programs are gaining traction, particularly in developed markets and urban business hubs. This segment offers stable demand and long-term revenue opportunities for preschool providers through partnerships with corporations.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 285 Billion |

| Market Size in 2026 | USD 303.81 Billion |

| Market Size in 2031 | USD 418.20 Billion |

| CAGR | 6.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Private preschools dominate the global market, accounting for approximately 55% of total revenue in 2025. The leadership of this segment is primarily driven by increasing parental preference for high-quality early education, structured curricula, and enhanced child development outcomes. Private institutions can offer differentiated value through smaller class sizes, trained educators, advanced infrastructure, and international curriculum frameworks, which significantly enhance their appeal among urban and middle-to-high-income households. Additionally, the rapid expansion of branded preschool chains and franchise models has enabled scalability and standardization, further strengthening this segment’s dominance globally.

Public preschools continue to play a crucial role in ensuring mass access, particularly in developing economies where affordability is a key concern. Governments are actively investing in universal early childhood education programs, thereby increasing enrollment volumes in public institutions. NGO and community-based preschools are vital in underserved and rural regions, addressing accessibility gaps with low-cost models. Meanwhile, premium and international preschools are witnessing strong growth in metropolitan areas, driven by rising disposable incomes and demand for globally recognized education systems. Mid-tier and affordable private preschools remain the backbone of the market, capturing a large share of enrollments due to their balance between cost and quality.

Application Insights

Montessori-based programs lead the curriculum segment, accounting for nearly 28% of the global market share. This dominance is driven by the model’s strong global acceptance, emphasis on self-directed learning, and proven outcomes in cognitive and social development. Parents increasingly prefer Montessori education due to its child-centric approach, which fosters independence, creativity, and critical thinking at an early stage.

Play-based and activity-based learning models are rapidly gaining traction as they align with modern pedagogical approaches emphasizing experiential learning and emotional development. These models are particularly popular in developed markets and urban centers where parents prioritize holistic development over rote learning. Structured academic programs continue to maintain steady demand, especially in regions with competitive schooling systems where early academic readiness is valued. Hybrid curriculum models that integrate multiple teaching methodologies are emerging as a strong trend, offering flexibility and comprehensive developmental outcomes, thereby attracting a broader parent base.

Distribution Channel Insights

Physical classroom-based learning remains the dominant delivery mode, contributing over 75% of the global market. The leadership of this segment is driven by the critical importance of social interaction, hands-on activities, and emotional development during early childhood, which cannot be fully replicated through digital platforms. Parents continue to prioritize in-person learning environments that provide structured routines, peer interaction, and supervised development.

However, hybrid learning models are witnessing significant growth, supported by increasing digital adoption and demand for flexible learning solutions. These models combine classroom teaching with digital tools such as interactive applications and remote engagement platforms, enhancing both learning outcomes and parental involvement. Fully online preschool programs, while still a niche segment, are gaining traction in urban areas with high internet penetration and tech-savvy populations. Franchise networks serve as a critical distribution channel, enabling rapid geographic expansion, standardized service delivery, and brand-driven enrollment growth across both developed and emerging markets.

End-User Insights

Individual households represent the largest end-user segment, accounting for over 80% of total demand. This dominance is driven by rising disposable incomes, increasing awareness of early childhood education benefits, and a growing emphasis on structured learning environments. Parents are increasingly willing to invest in quality preschool education as a foundation for long-term academic success.

Employer-sponsored childcare is the fastest-growing segment, supported by rising corporate focus on employee well-being and productivity. Companies are investing in on-site childcare facilities or partnerships with preschool providers to attract and retain talent, particularly in urban business hubs. Government-supported enrollments are also expanding significantly, especially in developing countries where public policies are aimed at increasing preschool accessibility and improving educational outcomes. This segment plays a critical role in driving enrollment volumes, particularly among low- and middle-income populations.

Age Group Insights

The 3–4 years age group (LKG) accounts for the largest share of the preschool market, contributing approximately 35% of total enrollments. This segment leads due to its role as the primary entry point into structured education, where children begin formal learning and socialization. Parents view this stage as critical for preparing children for primary education, driving higher enrollment rates.

Nursery and UKG segments also contribute significantly, with steady demand across both developed and emerging markets. The pre-nursery segment is witnessing increasing growth, particularly with the integration of daycare services that cater to working parents. Overall, rising awareness of early childhood development and increasing urbanization are driving enrollment across all age groups, with a noticeable shift toward earlier entry into structured learning programs.

Explore more data points, trends and opportunities Download Free Sample Report

Preschool Market Segmentations

By Product Type

- Public Preschools

- Private Preschools

- NGO / Community-Based Preschools

By Application

- Montessori-Based Programs

- Play-Based / Activity-Based Learning

- Structured Academic Programs

- Hybrid / Integrated Curriculum Models

By Distribution Channel

- Physical Classroom-Based Learning

- Hybrid Learning Models

- Fully Online Preschool Programs

- Franchise Networks

By End-User

- Individual Households

- Employer-Sponsored Childcare

- Government-Supported Enrollments

By Age Group

- Pre-Nursery

- Nursery

- LKG

- UKG

Regional Insights

North America

North America holds approximately 30% of the global preschool market, with the United States accounting for the majority share. The region’s dominance is driven by high enrollment rates, strong government funding for early education programs, and widespread adoption of employer-sponsored childcare. Additionally, high disposable income levels and strong awareness of early childhood development contribute to sustained demand. The presence of large private preschool chains and advanced infrastructure further strengthens market growth. Increasing demand for premium and specialized preschool programs, including STEM-focused early education, is also shaping the regional landscape.

Europe

Europe accounts for around 25% of the global market, with leading countries including Germany, France, and the United Kingdom. Growth in this region is primarily driven by well-established public preschool systems, strong regulatory frameworks, and significant government investments in early childhood education. High enrollment rates and universal preschool policies ensure stable demand. Additionally, increasing focus on inclusive education and sustainability is influencing curriculum development. While the market is relatively mature, innovation in teaching methodologies and rising demand for bilingual and international programs are supporting moderate growth.

Asia-Pacific

Asia-Pacific represents approximately 28% of the market and is the fastest-growing region, with a CAGR of around 8%. China and India are the largest contributors, driven by large child populations, rapid urbanization, and rising middle-class incomes. Key growth drivers include increasing female workforce participation, expanding private preschool networks, and strong government initiatives promoting early education. The region is also witnessing the rapid adoption of franchise models and digital learning tools. In addition, rising parental aspirations for quality education and global curricula are fueling demand for premium preschool services in urban areas.

Latin America

Latin America contributes approximately 7% of the global market, with Brazil and Mexico leading demand. Growth in this region is driven by increasing awareness of early childhood education, gradual expansion of private preschool chains, and improving economic conditions. Government initiatives aimed at improving educational access are also supporting enrollment growth. Urbanization and rising middle-class populations are creating opportunities for mid-tier and affordable preschool models, which are gaining popularity across the region.

Middle East & Africa

The Middle East & Africa region holds around 10% of the global market, with demand concentrated in countries such as the UAE, Saudi Arabia, and South Africa. Growth is driven by increasing expatriate populations, rising disposable incomes, and government investments in education infrastructure. In the Middle East, demand for premium and international preschools is particularly strong, supported by high-income demographics and a preference for global curricula. In Africa, expansion is driven by population growth, urbanization, and an increasing focus on improving early childhood education access. Public-private partnerships and NGO initiatives are playing a key role in addressing infrastructure and accessibility challenges across the region.

Key Players in the Preschool Market

- Bright Horizons Family Solutions

- KinderCare Education

- Learning Care Group

- Busy Bees Childcare

- Primrose Schools

- Goddard School

- Maple Bear Global Schools

- Spring Education Group

- Kids ‘R’ Kids

- Safari Kid

- Kangaroo Kids Education

- EuroKids International

- Little Millennium

- Babilou Group

- Crestar Education Group