Pre-Owned Luxury Watches Market Size

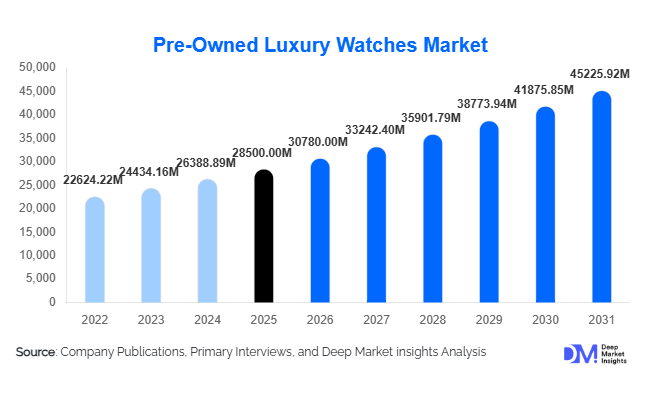

According to Deep Market Insights, the global Pre-Owned Luxury Watches Market was valued at USD 28,500 million in 2025 and is projected to grow from USD 30,780.00 million in 2026 to reach USD 45,225.92 million by 2031, expanding at a CAGR of 8.0% during the forecast period (2026–2031). The market growth is primarily driven by rising demand for authenticated luxury timepieces, increasing popularity of certified pre-owned programs launched by leading brands, and growing consumer preference for luxury watches as alternative investment assets. In addition, digital resale platforms and blockchain-based authentication systems are improving trust, transparency, and global accessibility, further strengthening market expansion.

Key Market Insights

- Luxury watches are increasingly being viewed as investment-grade assets, with strong value retention for brands like Rolex, Patek Philippe, and Audemars Piguet.

- Certified Pre-Owned (CPO) programs are reshaping the resale ecosystem, improving authenticity, pricing transparency, and brand control over secondary markets.

- Online resale platforms dominate growth, enabling cross-border transactions and expanding access to global buyers.

- Asia-Pacific is emerging as the fastest-growing region, driven by rising wealth in China, India, and Southeast Asia.

- Sustainability and circular economy trends are accelerating demand, especially among younger luxury consumers.

- Blockchain and AI-based authentication technologies are transforming market trust and pricing accuracy.

Pre-Owned Luxury Watches Market Trends

Expansion of Certified Pre-Owned Ecosystems

Luxury watch brands are increasingly establishing certified pre-owned programs to directly participate in the secondary market. This shift is helping brands regain control over pricing, authentication, and customer relationships. It is also reducing counterfeit risks and improving buyer confidence. As a result, the market is becoming more structured, with greater transparency and stronger brand-led resale ecosystems emerging globally.

Digital Transformation of Secondary Watch Trading

The market is rapidly shifting toward digital-first resale platforms that leverage AI-based pricing engines, real-time valuation tools, and global logistics networks. Online marketplaces are making luxury watches accessible to a broader consumer base, enabling seamless cross-border transactions. Blockchain integration is further strengthening provenance tracking, ensuring authenticity and reducing fraud risks in high-value transactions.

Pre-Owned Luxury Watches Market Drivers

Rising Investment Demand for Luxury Watches

Luxury watches are increasingly being treated as alternative investment assets, particularly by high-net-worth individuals and collectors. Scarcity of limited-edition and discontinued models has resulted in strong price appreciation in the secondary market. This investment appeal is significantly boosting demand, especially for ultra-luxury and collectible watch segments.

Growing Sustainability and Circular Economy Adoption

Consumers are increasingly shifting toward sustainable luxury consumption, driving demand for pre-owned products. Buying pre-owned luxury watches aligns with environmental consciousness while still offering premium brand access. This trend is especially strong among younger demographics who prioritize ethical consumption and long-term value retention.

Pre-Owned Luxury Watches Market Restraints

Counterfeit Risks and Authentication Challenges

The presence of counterfeit watches and grey market trading continues to pose a major challenge for the industry. Despite technological advancements in authentication, high-value luxury watches remain vulnerable to fraud, which can reduce buyer trust and impact market growth in unregulated segments.

Price Volatility in Secondary Markets

The pre-owned luxury watch market is exposed to significant price fluctuations, especially for hype-driven or celebrity-endorsed models. This volatility can create uncertainty among buyers and investors, limiting participation from risk-averse consumer segments and affecting overall market stability.

Pre-Owned Luxury Watches Market Opportunities

Growth of Investment-Oriented Watch Financing

The financialization of luxury watches presents a major opportunity, including watch-backed lending, fractional ownership, and investment funds. As watches become recognized as tangible alternative assets, financial institutions are increasingly exploring structured investment products linked to luxury timepieces.

Expansion of Emerging Market Demand

Rapid wealth creation in Asia-Pacific and the Middle East is driving strong demand for pre-owned luxury watches. Consumers in these regions are increasingly entering the luxury market through secondary channels due to affordability and accessibility. This creates significant growth opportunities for digital platforms and global resale networks.

Product Type Insights

Mechanical automatic watches dominate the global pre-owned luxury watches market, accounting for approximately 42% of global market share in 2025. Their leadership is primarily driven by superior craftsmanship, long-term durability, and strong resale liquidity across global secondary markets. These watches are highly preferred by collectors and investors due to their mechanical complexity, heritage value, and consistent price appreciation over time. The strong brand equity of Swiss manufacturers further reinforces demand stability in this segment, making it the most traded category across both online platforms and auction houses.

Ultra-luxury and complication watches, including chronographs, tourbillons, and perpetual calendars, continue to command premium valuations due to extreme scarcity and strong collector-driven demand. Although lower in volume, these segments significantly influence overall market value due to high-ticket transactions and auction-driven price benchmarks. Quartz luxury watches occupy a smaller share of the market but remain relevant in entry-level luxury consumption, particularly among first-time luxury buyers seeking affordability and brand access. Vintage and limited-edition watches represent one of the fastest-growing segments, driven by scarcity-led appreciation, celebrity influence, and increasing interest in heritage timepieces. Rising demand for discontinued models from brands such as Rolex, Patek Philippe, and Audemars Piguet is further strengthening this segment’s growth trajectory. The combination of emotional value, historical significance, and investment potential positions vintage watches as a structurally expanding category in the secondary luxury ecosystem.

Application Insights

The pre-owned luxury watches market is primarily driven by collectors and investors, who together account for more than 55% of total global demand. Collectors play a crucial role in sustaining demand for rare, vintage, and limited-edition timepieces, often focusing on heritage value, craftsmanship, and exclusivity. Investors, on the other hand, are increasingly treating luxury watches as alternative asset classes, benefiting from price appreciation, scarcity-driven valuation, and portfolio diversification advantages.

Fashion-oriented consumers represent a rapidly expanding segment, particularly among millennials and Gen Z buyers entering the luxury ecosystem through pre-owned channels. This group is driven by affordability, brand aspiration, and sustainability considerations, making pre-owned watches an accessible entry point into luxury ownership. Corporate gifting and institutional acquisitions also contribute meaningfully to demand, especially in emerging economies where luxury watches symbolize prestige, wealth, and professional status.

Distribution Channel Insights

Online luxury watch marketplaces dominate global distribution, accounting for approximately 33% of total transactions in 2025. Their growth is driven by enhanced price transparency, global accessibility, AI-powered valuation tools, and secure cross-border logistics systems. These platforms are significantly lowering entry barriers for buyers and enabling seamless international trade of high-value timepieces. Auction houses remain critical for ultra-luxury and rare collectible watches, often setting global price benchmarks for iconic models. Brick-and-mortar dealers continue to play a strong role in localized luxury ecosystems, particularly for high-value transactions requiring physical verification and personalized service. Brand-certified pre-owned programs are rapidly gaining traction, reshaping trust dynamics by offering manufacturer-backed authentication and warranty support.

Peer-to-peer transactions, while still present, are gradually declining due to increasing concerns over counterfeit risks, lack of authentication, and pricing inconsistencies. The market is steadily shifting toward structured, transparent, and brand-influenced resale ecosystems.

End-User Insights

Collectors and investors remain the dominant end-user groups in the pre-owned luxury watches market, collectively shaping over half of global demand. Collectors focus on rarity, provenance, and heritage significance, while investors prioritize capital appreciation and asset diversification. This dual demand structure strengthens market resilience and reduces dependence on purely consumption-driven cycles.

Fashion-conscious buyers represent a growing segment, particularly in urban centers and emerging economies where luxury accessibility is expanding. These consumers are increasingly attracted to pre-owned luxury watches as a sustainable and cost-effective entry into high-end fashion. Institutional buyers, including auction houses, luxury funds, and portfolio managers, are also expanding their presence, contributing to the market’s increasing financialization. The market is progressively shifting from consumption-based ownership to investment-oriented acquisition, positioning luxury watches as alternative financial instruments within global wealth portfolios.

| By Product Type | By Application | By Distribution Channel | By End-User |

|---|---|---|---|

|

|

|

|

Regional Insights

North America

North America accounts for approximately 28% of the global market in 2025, led by the United States, which remains one of the most mature and high-value secondary luxury watch markets globally. Strong purchasing power, established collector networks, and deep penetration of digital resale platforms support consistent demand growth. The region is particularly active in investment-grade watches, with strong participation from high-net-worth individuals and financial investors. Expansion of luxury investment portfolios, high adoption of online resale platforms, and strong presence of auction houses are key factors driving regional growth. Increasing interest in alternative asset classes is further accelerating demand for collectible timepieces.

Europe

Europe holds approximately 32% market share in 2025, making it the largest regional market for pre-owned luxury watches. Switzerland serves as the global production and authentication hub, while the United Kingdom, Germany, and France dominate resale and auction activity. The region benefits from strong heritage brands, deep collector culture, and well-established luxury retail infrastructure. Strong manufacturing heritage, dominance of Swiss luxury brands, and high concentration of auction houses are key growth enablers. Additionally, rising demand for certified pre-owned programs and sustainable luxury consumption is reinforcing market expansion across Europe.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, driven by rising disposable incomes and rapid expansion of luxury consumption in China, India, Japan, and Southeast Asia. China leads in luxury watch consumption, while India is emerging as a strong growth market for mid-range and entry-luxury pre-owned watches. Japan maintains steady demand driven by vintage and precision watch appreciation. Expanding middle-class wealth, increasing digital adoption, rising investment awareness in luxury assets, and strong influence of social media-driven luxury culture are fueling rapid regional expansion. Improved cross-border e-commerce infrastructure is further accelerating market penetration.

Middle East & Africa

The Middle East is witnessing strong growth, particularly in the UAE and Saudi Arabia, driven by high-net-worth populations and strong luxury consumption culture. The region is increasingly positioning itself as a luxury trading hub connecting Europe, Asia, and Africa. Africa contributes through emerging intra-regional luxury trade, particularly in South Africa and Nigeria, where affluent consumer bases are expanding. Rising ultra-high-net-worth population, strong preference for luxury status symbols, and expanding luxury retail infrastructure are key drivers. Additionally, increasing tourism and cross-border luxury trade flows are strengthening regional demand.

Latin America

Latin America is an emerging market for pre-owned luxury watches, with Brazil and Mexico leading demand. Growth is supported by rising affluent consumer populations and increasing exposure to global luxury resale platforms. While still developing, the region is gradually integrating into global secondary luxury networks. Expanding high-income consumer base, increasing luxury aspiration, and growing digital penetration of global resale platforms are supporting regional growth. Rising interest in wealth diversification through luxury assets is also contributing to demand expansion.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Pre-Owned Luxury Watches Market

- Rolex

- Patek Philippe

- Audemars Piguet

- Omega

- Cartier

- Richard Mille

- Jaeger-LeCoultre

- Vacheron Constantin

- Breitling

- TAG Heuer

- Hublot