Portable Toilet Market Size

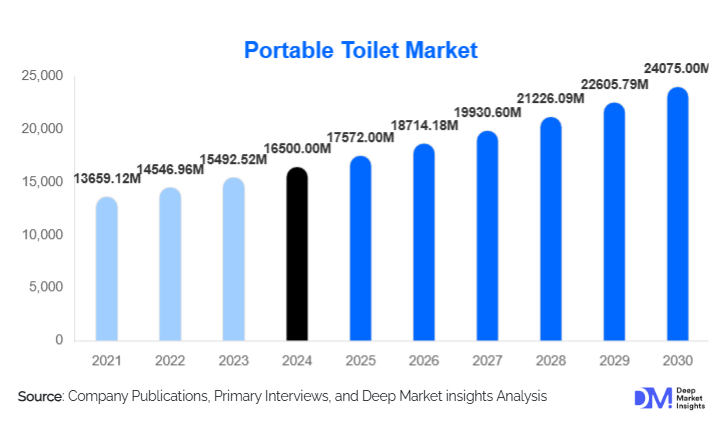

According to Deep Market Insights, the global portable toilet market size was valued at USD 16,500 million in 2025 and is projected to grow from USD 17,572 million in 2026 to reach USD 24,075 million by 2031, expanding at a CAGR of 6.5% during the forecast period (2026–2031). The portable toilet market growth is primarily driven by rapid infrastructure development, the expansion of outdoor events and construction activities, rising hygiene and sanitation standards, and increasing adoption of eco-friendly and smart-enabled mobile sanitation solutions.

Key Market Insights

- Standard portable toilets remain the core product category worldwide, serving construction sites, public events, and disaster relief operations due to their cost-effectiveness and ease of deployment.

- Construction sites and large-scale infrastructure projects account for the largest share of demand, supported by worker welfare regulations and mandatory sanitation compliance at project locations.

- Rental-based business models dominate procurement, as contractors, event organizers, and municipalities increasingly prefer flexible, service-inclusive contracts over outright purchases.

- Asia-Pacific and North America together contribute a major share of global revenue, with Asia-Pacific driven by urbanization and North America by well-established rental networks and stringent safety standards.

- Eco-friendly, water-saving, and chemical-reduced portable toilets are gaining traction, as regulators and customers push for lower environmental impact and better waste management.

- Leading manufacturers are integrating IoT, sensors, and solar power to deliver smart units with remote monitoring, optimized servicing, and improved user experience, especially in high-traffic locations.

Portable Toilet Market Trends

Eco-Friendly and Water-Efficient Portable Sanitation Solutions

Environmental sustainability is reshaping product development in the portable toilet market. Manufacturers are increasingly introducing units that use low-flush or waterless systems, biodegradable deodorizing chemicals, and recycled plastics in cabin construction. Composting and dry-flush designs are being deployed at eco-parks, nature reserves, and off-grid worksites to minimize water consumption and reduce the burden on local sewage infrastructure. Circularity initiatives, such as reclaiming and reprocessing damaged cabins into new units, are also gaining ground, extending product lifecycles and lowering embodied carbon footprints. Several leading brands now highlight sustainability as a key value proposition, offering “green” product lines that meet stricter environmental regulations and corporate ESG requirements.

Smart and IoT-Enabled Portable Toilets

Digitalization is emerging as a major trend, especially in large rental fleets and urban deployments. Smart portable toilets equipped with fill-level sensors, door-open counters, geolocation tracking, and maintenance alerts allow fleet operators to optimize service routes, reduce emergency overflows, and improve cleanliness. These connected units are increasingly integrated with fleet management software and customer portals, providing dashboards on usage intensity, cleaning history, and service schedules. In high-profile events, stadiums, and transportation hubs, smart modules also enable dynamic reallocation of units based on real-time demand. The development of IoT-ready portable toilets is supported by investment in mobile toilet rental and mobile sanitation services, where operational efficiency and data-driven planning significantly boost profitability.

Premium and User-Centric Portable Restroom Experiences

Beyond basic units, there is a clear shift toward premium and luxury portable toilets featuring flushing systems, interior lighting, ventilation fans, integrated handwashing basins, and touchless dispensers. Luxury restroom trailers for weddings, VIP zones, film sets, and corporate events often include climate control, upscale finishes, and accessibility-compliant layouts. User expectations for cleanliness, privacy, and comfort, accelerated by post-pandemic hygiene awareness, are pushing operators to upgrade fleets with more spacious and aesthetically pleasing units. This premiumization trend is particularly visible in developed markets in North America and Europe, where event organizers and brands view restroom quality as part of the overall guest experience and brand image.

Portable Toilet Market Drivers

Rapid Infrastructure Development and Construction Activities

Global investments in infrastructure, spanning roads, bridges, rail networks, industrial parks, renewable energy plants, and urban redevelopment, are a fundamental growth engine for the portable toilet market. Construction sites often operate in locations without permanent restrooms, making mobile units the only practical sanitation option. Regulatory bodies and labor codes in many countries now mandate adequate restroom facilities for workers, with specific ratios of toilets per worker on-site. This has significantly increased fleet sizes for rental providers and driven recurring contracts with large engineering, procurement, and construction (EPC) companies. Emerging markets in Asia-Pacific, the Middle East, and Latin America, where construction output is expanding at high single-digit rates, are particularly vital to long-term demand.

Rising Focus on Hygiene, Public Health, and Emergency Response

Heightened awareness of hygiene and infectious disease prevention has elevated the importance of safe sanitation in public spaces, events, and temporary facilities. Governments and municipalities increasingly deploy portable toilets for public gatherings, vaccination sites, refugee camps, and disaster relief operations to prevent open defecation and contamination risks. Aid agencies and NGOs also rely on mobile sanitation units in flood-hit or conflict-affected regions where permanent infrastructure is damaged or absent. These deployments often require rugged, easy-to-clean units that can be quickly transported and serviced. The perception of portable toilets has thus shifted from a convenience item at festivals to critical public-health infrastructure, supporting sustained demand across both developed and developing economies.

Growth of Outdoor Events, Recreation, and Mobile Workforces

The expansion of outdoor festivals, concerts, sporting events, religious gatherings, and recreational activities such as camping and caravanning is another strong demand driver. Event organizers prefer portable toilet rentals that include delivery, set-up, and scheduled servicing, enabling them to accommodate large crowds without permanent facility investments. Similarly, mobile workforces in sectors such as mining, oil & gas exploration, utilities maintenance, and forestry operations depend on temporary sanitation at remote locations. As tourism boards and private operators promote outdoor and adventure-based activities, the need for compliant, user-friendly portable restrooms at campgrounds, beaches, national parks, and highways continues to grow, supporting higher unit uptake, especially in premium and accessible formats.

Portable Toilet Market Restraints

High Lifecycle Service and Maintenance Costs

Despite strong demand, the portable toilet market faces profitability challenges linked to service-intensive operations. Each unit requires regular pumping, cleaning, consumable replenishment, and transport to and from sites. In regions with long travel distances, traffic congestion, or difficult terrain, service routes become time-consuming and fuel-intensive. Fleet owners must also invest in specialized vacuum trucks, treatment facilities, and trained staff to comply with waste-handling standards. These operational expenses can erode margins, particularly in price-sensitive contracts or low-density service areas. Smaller operators often struggle to scale profitably, while larger fleets must continually optimize routing and asset utilization to maintain competitiveness.

Stringent Environmental and Waste-Disposal Regulations

Regulations governing chemical use, effluent disposal, and odor control are becoming more stringent across many jurisdictions. Chemical toilets using formaldehyde or other harsh biocides face restrictions or phaseouts, forcing operators to transition to more expensive, eco-friendly additives and advanced treatment systems. In addition, local authorities may limit discharge points or impose higher fees for wastewater treatment, especially in environmentally sensitive zones. Non-compliance risks fines, license suspension, or reputational damage. These regulatory pressures increase compliance costs and may slow expansion in markets where enforcement is tight but customers resist higher rental prices.

Portable Toilet Market Opportunities

Green, Circular, and Low-Impact Sanitation Solutions

There is substantial opportunity in developing portable toilets that align with circular economy and net-zero ambitions. Units designed from high-recycled-content plastics, with long service lives and modular, replaceable components, are increasingly attractive to ESG-focused customers. Composting and bio-digester toilets that transform waste into usable fertilizer or biogas present attractive solutions for remote communities, agricultural sites, and eco-resorts. Suppliers that can certify lower lifecycle emissions, offer take-back schemes, and integrate with decentralized waste treatment systems are well-positioned to win government tenders and corporate sustainability-driven contracts.

Smart Fleets, Data-Driven Services, and Premium Experiences

IoT integration and data analytics open new value pools beyond basic rentals. Fleet operators can sell “service-level guarantees” based on predictive maintenance, dynamic servicing, and uptime commitments, differentiating themselves through reliability and cleanliness metrics. Digital platforms for online booking, route optimization, and customer reporting enable more transparent pricing and performance benchmarking. At the same time, premium segments, such as luxury event trailers, ADA-compliant units, and specialized sanitary cabins for film, defense, and offshore operations, offer higher margins. Vendors combining hardware innovation with integrated services and software are likely to capture disproportionate value as the market professionalizes.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 16500 Million |

| Market Size in 2026 | USD 17572 Million |

| Market Size in 2031 | USD 24075 Million |

| CAGR | 6.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Standard portable toilets dominate global product demand, accounting for an estimated 50–55% share of the market in 2025. These units are the “workhorses” of the industry, typically comprising a single toilet, urinal, and basic ventilation within a polyethylene or composite cabin. They are favored by construction contractors and event organizers due to low upfront cost, easy transport, and flexible deployment across varied terrains. Optional add-ons, such as hand-sanitizer dispensers, small washbasins, solar lighting, and occupancy indicators, allow operators to tailor standard units for both construction and special-event applications. While luxury trailers and flushing cabins are growing faster in relative terms, standard units will remain the backbone of fleet compositions worldwide because they provide the best balance of cost, durability, and utilization rates.

Application Insights

Construction sites represent the single largest application segment, contributing an estimated 40–45% of global portable toilet revenue in 2025. Regulatory requirements for labor welfare, combined with continuous infrastructure expansion in Asia-Pacific, the Middle East, and parts of Africa and Latin America, sustain high recurring demand. Special events, including music festivals, sports tournaments, religious gatherings, and elections, form the second key application cluster and are one of the fastest-growing segments, supported by short-term rentals with higher daily rates and premium unit mixes. Additional demand arises from recreational vehicle (RV) parks, campgrounds, marine applications, remote industrial and mining sites, and emergency relief operations, where reliable, flexible sanitation is essential for public health and operational continuity.

Distribution Channel Insights

Rental services are the predominant distribution and revenue model in the portable toilet market, accounting for a substantial majority of global turnover. Customers such as construction firms, municipalities, and event organizers typically prefer renting to avoid capital expenditure, storage, and servicing responsibilities. Leading rental operators offer bundled contracts that include unit delivery, installation, routine servicing, and waste disposal, often on weekly or monthly schedules. Direct sales remain important for campsites, industrial facilities, defense establishments, and large venues that require permanent on-site fleets. Digitalization is strengthening online and B2B platforms, enabling customers to configure unit types, servicing frequency, and contract duration via self-service portals, while dynamic pricing and route optimization improve operator margins.

End-User Insights

The construction and infrastructure sector is the most significant end-user group, with strong alignment between project pipelines and mobile sanitation needs. Oil & gas, mining, and utilities contribute additional structural demand from remote operations, where robust, weather-resistant units are prioritized. The events and entertainment industry is emerging as the fastest-growing end-user cluster, driven by rising attendance at festivals, sports tournaments, corporate roadshows, and large outdoor gatherings. Government and municipal bodies also form a key end-user segment via public-park deployments, transport hubs, roadside rest areas, and emergency shelters. Healthcare, hospitality, and tourism industries increasingly deploy portable toilets to manage surge capacity, pop-up facilities, and temporary expansions, such as vaccination camps or seasonal tourism flows.

Technology Insights

From a technology perspective, the market is gradually transitioning from purely dry, non-flush units to more sophisticated flushing, recirculating, and waterless systems. Recirculating flush technology offers improved user experience and odor control, especially in high-end and long-stay deployments, while still conserving water relative to traditional flush toilets. Vacuum-assisted units are gaining traction where efficient waste evacuation and reduced odor are critical, such as in dense urban events or confined worksites. Smart monitoring technology, integrating sensors and telematics, enables operators to remotely track usage, tank levels, and door cycles, improving service planning. As regulatory and customer pressure intensifies, there is growing investment in bio-based deodorants, odor-neutralizing technologies, and closed-loop waste treatment solutions that reduce environmental impact and lower per-use operating costs over time.

Explore more data points, trends and opportunities Download Free Sample Report

Portable Toilet Market Segmentations

Product Type

- Standard Portable Toilets

- Luxury Portable Toilets

- Trailer-Mounted Portable Toilets

- Chemical Portable Toilets

- Composting Portable Toilets

- Vacuum Flush Portable Toilets

- Solar-Powered Portable Toilets

Application

- Construction Sites

- Events & Festivals

- Mining & Oil Exploration Sites

- Disaster Relief Camps

- Military & Defense Operations

- Agriculture & Forestry Sites

- Tourism & Recreational Areas

End-User Industry

- Construction & Infrastructure

- Entertainment, Sports & Events

- Oil & Gas and Mining

- Government & Municipal Bodies

- Defense

- Hospitality & Tourism

- Healthcare & Emergency Services

Technology

- Dry Portable Toilets

- Flushing Portable Toilets

- Recirculating Flush Toilets

- Waterless Portable Toilets

- Biodegradable / Waste-to-Energy Toilets

- Self-Cleaning & Smart-Enabled Toilets

Material

- Plastic (HDPE / Polyethylene)

- Fiber Reinforced Plastic (FRP)

- Steel & Aluminum

- Composite Materials

Distribution Channel

- Rental Service Providers

- Direct Sales to End Users

- Online Platforms & Marketplaces

- Authorized Dealers & Distributors

Regional Insights

North America

North America is one of the leading regional markets for portable toilets, underpinned by a large and stable rental industry. The U.S. accounts for the majority of regional revenue, benefiting from stringent workplace regulations, extensive construction pipelines, and a packed calendar of sports and entertainment events. Major rental operators and manufacturers headquartered in the region support nationwide coverage, enabling large-scale deployments for infrastructure projects, disaster response, and national events. Canada contributes additional demand from mining regions, energy projects, and outdoor recreation areas. Overall, North America is estimated to represent roughly 30% of global market value in 2025, with steady mid-single to high-single-digit growth expected through 2031.

Europe

Europe is a mature and regulation-driven market, with key demand centers in Germany, the U.K., France, Italy, Spain, and the Nordic countries. The region hosts some of the world’s largest mobile sanitation operators, which maintain extensive fleets across construction, events, and industrial sectors. Europe’s focus on sustainability and waste-management compliance supports strong adoption of eco-friendly units, closed-loop waste handling, and cabins with integrated handwashing systems. Large music festivals, trade fairs, and sports tournaments contribute substantial seasonal demand. Europe’s share of the global market is estimated at around 25–28% in 2025, with growth fuelled by infrastructure renovation, renewable energy projects, and increasingly stringent sanitation rules at outdoor events.

Asia-Pacific

Asia-Pacific is the fastest-growing region in the portable toilet market, driven by rapid urbanization, large-scale infrastructure development, and improving sanitation standards. China, India, Japan, Australia, and Southeast Asian economies are key contributors. Government initiatives such as national clean sanitation programs and smart-city projects have significantly accelerated portable toilet deployment in urban and semi-urban areas. Construction booms in Southeast Asia, infrastructure upgrades in Australia, and rising popularity of outdoor recreation across the region further support demand. Asia-Pacific accounts for an estimated 30–33% of global revenue in 2025and is expected to post the highest regional CAGR through 2031, making it a key focus area for global manufacturers and rental groups.

Latin America

Latin America’s portable toilet market is growing steadily, supported by infrastructure spending, large public events, and a gradual tightening of health and safety regulations. Brazil and Mexico lead regional demand, with additional contributions from Argentina, Chile, Colombia, and Peru. Construction projects in energy, transport, and urban development, as well as mass cultural and sports events, create recurring rental opportunities. However, market penetration remains lower than in North America or Europe, leaving headroom for expansion as awareness of sanitation standards and environmental compliance increases. International brands often partner with or acquire local operators to strengthen distribution and service networks.

Middle East & Africa

The Middle East & Africa region presents a mix of high-value and humanitarian-driven demand. In the Gulf Cooperation Council (GCC) countries, including the UAE, Saudi Arabia, and Qatar, portable toilet usage is closely tied to mega-projects, industrial zones, and high-profile events. Large construction initiatives and tourism developments are creating substantial, long-duration contracts for mobile sanitation services. In Africa, mining operations, infrastructure investment, and public-health initiatives drive portable toilet deployment, particularly in South Africa, Nigeria, Kenya, and emerging East African markets. Refugee camps and disaster-relief operations in parts of Africa and the Middle East also rely heavily on mobile sanitation solutions, often funded or coordinated by governments and international organizations.

Company Market Share

The portable toilet market share is moderately consolidated at the global level, with the top five manufacturers and integrated service providers estimated to account for roughly 35% of total industry revenue in 2025. The remainder of the market is fragmented among regional rental companies, specialized niche suppliers, and local manufacturers. Leading players compete on product durability, service reliability, geographic coverage, and the breadth of their product portfolios, which span standard cabins, luxury trailers, ADA-compliant units, and specialized solutions for construction, events, and industrial sites. Ongoing consolidation, via acquisitions of regional operators and fleet expansions, is gradually increasing the scale and sophistication of major brands, while still leaving room for agile local competitors in niche markets.

Key Players in the Portable Toilet Market

- Satellite Industries

- PolyJohn Enterprises Corporation

- Thetford Corporation

- TOI TOI & DIXI Group GmbH

- Sanitech

- United Site Services Inc.

- Armal Srl

- Shorelink International Ltd.

- Camco Manufacturing, Inc.

- Blue Bowl Sanitation Inc.

- B&B Portable Toilets

- Honey Bucket

- Waste Management, Inc.

- Mr. John

- Aussie Loo

Recent Developments

- In January 2025, United Site Services launched a new line of eco-friendly portable toilets with reduced water usage and biodegradable deodorizing solutions, targeting construction and event clients seeking lower environmental impact.

- In March 2025, Satellite Industries introduced solar-powered and smart-enabled portable toilet models designed to cut energy costs and support remote monitoring of tank levels, service frequency, and unit utilization.

- In April 2025, PolyJohn expanded its ADA-compliant and recirculating flush product portfolio, addressing stricter accessibility regulations and demand for higher-comfort units at premium events and public sites.

- In Q3 2025, TOI TOI & DIXI Group announced a strategic partnership focused on sustainable portable toilets for major European festivals and construction projects, reinforcing its position as a leader in eco-conscious mobile sanitation.