Portable Chopper Market Size

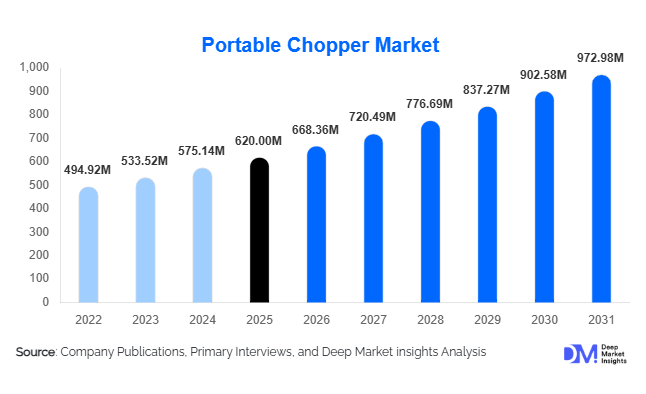

According to Deep Market Insights, the global portable chopper market size was valued at USD 620 million in 2025 and is projected to grow from USD 668.36 million in 2026 to reach USD 972.98 million by 2031, expanding at a CAGR of 7.8% during the forecast period (2026–2031). The portable chopper market growth is primarily driven by increasing consumer demand for compact, time-saving kitchen appliances, rising urbanization, and the growing adoption of modern cooking solutions across households and small food businesses.

Key Market Insights

- Portable choppers are increasingly evolving toward cordless and rechargeable designs, enhancing convenience and portability for urban consumers.

- Asia-Pacific dominates the market, driven by strong demand from India and China due to affordability and rising middle-class households.

- Online retail channels account for nearly half of total sales, supported by e-commerce growth and competitive pricing strategies.

- Residential usage represents over 75% of total demand, as portable choppers are widely adopted in home kitchens.

- Economy and mid-range products dominate volume sales, especially in emerging markets with price-sensitive consumers.

- Technological advancements, including USB charging, improved blade systems, and safety features, are enhancing product differentiation.

What are the latest trends in the portable chopper market?

Shift Toward Cordless and Rechargeable Devices

The market is witnessing a strong shift from manual and corded choppers to cordless, rechargeable variants. Consumers increasingly prefer USB-powered devices that offer portability and ease of use without dependency on electrical outlets. These products are particularly popular among urban households, travelers, and small kitchens where space and convenience are critical. Manufacturers are investing in battery efficiency, faster charging, and compact motor technologies to enhance product performance. This trend is expected to redefine the product landscape, especially in premium and mid-range segments.

Rising Demand for Compact and Multi-Functional Appliances

Consumers are increasingly seeking multifunctional kitchen tools that combine chopping, blending, and mincing capabilities. Portable choppers with interchangeable blades and attachments are gaining traction, offering greater value for money. This trend is closely aligned with shrinking kitchen spaces in urban apartments and the need for clutter-free cooking environments. Additionally, aesthetic designs and lightweight materials are becoming key purchase drivers, especially among younger consumers and first-time buyers.

What are the key drivers in the portable chopper market?

Growing Demand for Convenience in Food Preparation

The increasing pace of modern lifestyles has significantly boosted demand for time-saving kitchen appliances. Portable choppers reduce manual effort and preparation time, making them essential tools for working professionals and nuclear families. The shift toward quick meal preparation and ready-to-cook ingredients further supports this demand.

Expansion of the Small Kitchen Appliances Industry

The broader growth of the small kitchen appliances sector, supported by rising disposable incomes and lifestyle upgrades, is driving the adoption of portable choppers. Consumers are investing in compact appliances that enhance efficiency without occupying significant space. This trend is particularly strong in urban areas across emerging economies.

Rapid Growth of E-commerce Platforms

The proliferation of e-commerce has significantly increased product accessibility and visibility. Online platforms offer competitive pricing, product comparisons, and user reviews, encouraging higher adoption rates. Promotional campaigns, discounts, and bundled offers further accelerate sales, particularly in price-sensitive markets.

What are the restraints for the global market?

Durability Concerns in Low-Cost Products

A significant portion of the market is dominated by low-cost products that often suffer from limited durability and inconsistent performance. These quality concerns can impact consumer trust and reduce repeat purchases, posing a challenge for manufacturers operating in the economy segment.

Availability of Substitute Products

The presence of alternatives such as full-sized food processors, blenders, and traditional manual tools can limit market growth. In price-sensitive regions, consumers may prefer multifunctional appliances or conventional methods over purchasing a dedicated portable chopper.

What are the key opportunities in the portable chopper industry?

Expansion in Emerging Markets

Emerging economies across Asia-Pacific, Latin America, and Africa present significant growth opportunities. Rising disposable incomes, urbanization, and expanding retail infrastructure are driving demand for affordable kitchen appliances. Localized product offerings tailored to regional cooking habits can further enhance market penetration.

Product Premiumization and Innovation

There is growing consumer willingness to invest in premium products with enhanced durability, aesthetics, and advanced features. Stainless steel builds, noise reduction technologies, and multi-blade systems are gaining popularity. Eco-friendly materials and sustainable packaging also present differentiation opportunities for brands targeting environmentally conscious consumers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 620 Million |

| Market Size in 2026 | USD 668.36 Million |

| Market Size in 2031 | USD 972.98 Million |

| CAGR | 7.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Manual portable choppers continue to dominate the global market, capturing approximately 42% of the total share in 2025. This leadership is primarily driven by affordability, ease of use, and widespread adoption in developing regions where price sensitivity is high. Consumers in these markets often prioritize cost-effective, durable solutions for daily household food preparation. Electric cordless choppers, meanwhile, represent the fastest-growing segment, fueled by increasing demand for convenience, portability, and technological innovation such as rechargeable batteries and enhanced safety mechanisms. The convenience of cordless operation is particularly attractive to urban consumers and nuclear families with compact kitchens. Corded electric choppers maintain a smaller share due to limited portability but remain relevant in commercial applications and high-volume food preparation settings where a continuous power supply is required. Overall, technological advancements and evolving consumer preferences are expected to further accelerate the growth of electric and cordless variants over the forecast period.

Capacity Insights

The 500 ml to 1 liter capacity segment leads the market with around 38% share, offering an ideal balance between portability and practical usability for small to medium households. Choppers below 500 ml are widely used for quick or single-serving tasks such as chopping herbs or preparing small quantities of sauces, making them popular in urban apartments and dormitory kitchens. Conversely, larger capacity units above 1 liter cater primarily to commercial kitchens, restaurants, and catering services where bulk food preparation is required. The growth of the mid-capacity segment is driven by the increasing prevalence of nuclear families and small households seeking efficient, multi-purpose kitchen appliances that reduce meal preparation time without occupying excessive counter space.

Distribution Channel Insights

Online retail channels dominate the market with nearly 48% share, benefiting from rising e-commerce penetration, easy access to a wide variety of models, competitive pricing, and convenience in home delivery. Digital platforms also provide consumers with detailed product specifications, ratings, and reviews, helping them make informed purchase decisions. Offline retail channels, including supermarkets, hypermarkets, specialty kitchen stores, and multi-brand appliance stores, continue to play a critical role, particularly in regions where consumers prefer to physically inspect products prior to purchase. Additionally, brand-exclusive stores are increasingly serving as demonstration hubs for premium portable choppers, helping manufacturers showcase innovative features and reinforce brand loyalty.

End-Use Insights

The residential segment remains the dominant end-use category, accounting for over 75% of total demand, driven by the rising need for compact, time-saving kitchen appliances in urban households. Consumers are increasingly seeking multifunctional devices capable of performing chopping, mincing, and blending tasks to streamline meal preparation. The commercial segment, comprising restaurants, cafes, cloud kitchens, and catering services, is witnessing rapid growth due to the expansion of the foodservice industry and rising demand for efficient and hygienic food preparation tools. The proliferation of food delivery platforms and cloud kitchens has further stimulated demand from small and medium-sized businesses that require portable, reliable, and easy-to-clean appliances to manage high volumes in constrained kitchen spaces.

Explore more data points, trends and opportunities Download Free Sample Report

Portable Chopper Market Segmentations

By Product Type

- Manual Portable Choppers

- Electric Corded Portable Choppers

- Electric Cordless/Rechargeable Portable Choppers

By Capacity

- Below 500 ml

- 500 ml – 1 Liter

- 1 – 2 Liters

- Above 2 Liters

By Material Type

- Plastic Body Choppers

- Stainless Steel Body Choppers

- Glass Container Choppers

By Distribution Channel

- Online Retail

- Hypermarkets/Supermarkets

- Specialty Kitchen Stores

- Multi-Brand Appliance Stores

By End-Use

- Residential/Household

- Commercial

Regional Insights

Asia-Pacific

Asia-Pacific leads the global portable chopper market with approximately 38% share in 2025, with China and India serving as the primary contributors. Market growth in this region is driven by rapidly increasing urban populations, rising disposable incomes, and growing awareness of modern kitchen appliances. India, in particular, is one of the fastest-growing markets, supported by expanding e-commerce platforms, rising nuclear family households, and increasing adoption of compact, multifunctional appliances suitable for small urban kitchens. Additionally, favorable government policies supporting domestic manufacturing and the presence of cost-competitive local brands are further propelling growth. China benefits from high urban penetration of modern retail chains, coupled with a consumer trend toward premium and technologically advanced portable choppers.

North America

North America accounts for around 25% of the market, with the United States dominating regional demand. Key drivers include high consumer spending power, preference for premium appliances, and widespread adoption of advanced, technology-enabled kitchen devices. Growing interest in cordless and high-performance choppers, along with increasing awareness of convenience-driven cooking solutions, supports steady demand. Additionally, online retail expansion and lifestyle trends favoring small, efficient kitchen appliances contribute to consistent market growth. Urbanization and the rising number of dual-income households further encourage the adoption of portable choppers as essential household tools.

Europe

Europe represents nearly 20% of the market, led by Germany, the UK, and France. Market expansion is primarily driven by consumer preference for high-quality, durable, and aesthetically appealing products. Sustainability and eco-conscious trends are also shaping purchasing behavior, with rising demand for products made from environmentally friendly materials. The prevalence of nuclear families and compact urban kitchens, combined with high disposable income levels, fuels growth in premium and mid-range segments. Advanced e-commerce penetration and organized retail networks further facilitate access to innovative portable choppers.

Latin America

Latin America accounts for about 8% market share, with Brazil and Mexico leading regional demand. Growth is fueled by expanding middle-class populations, rising disposable incomes, and increasing awareness of modern kitchen appliances. However, price sensitivity remains a key consideration, making economy and mid-range segments particularly important. Urbanization trends, coupled with a growing interest in convenient cooking solutions for small households and families, are supporting market adoption, while the emergence of e-commerce platforms is helping expand reach across smaller cities and towns.

Middle East & Africa

The Middle East & Africa region accounts for approximately 9% of the market, with growth concentrated in the UAE, South Africa, and Saudi Arabia. Key drivers include rising urbanization, increasing disposable incomes, and the expansion of organized retail and e-commerce platforms. Growing adoption of modern kitchen appliances in urban households, coupled with a preference for premium, technologically advanced, and easy-to-use choppers, is further stimulating market demand. Expat-driven consumer trends and the popularity of cloud kitchens and home-delivery food services in metropolitan areas are additional contributors to growth in this region.

Key Players in the Portable Chopper Market

- Philips

- Panasonic

- Bajaj Electricals

- Prestige (TTK Group)

- Pigeon (Stovekraft)

- Wonderchef

- Hamilton Beach

- Black+Decker

- Cuisinart

- KitchenAid

- Morphy Richards

- Bosch

- Xiaomi

- Kent RO Systems

- Havells