Plates Market Size

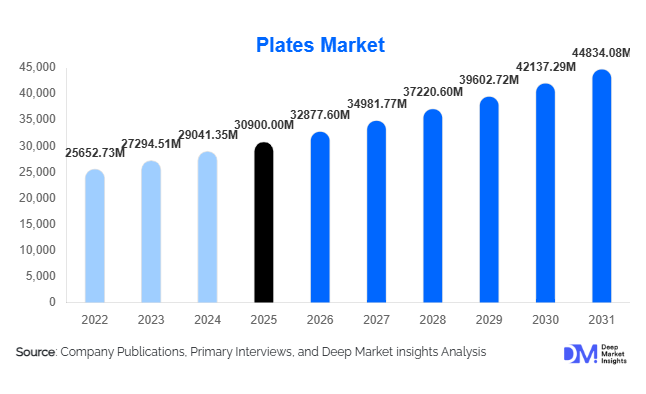

According to Deep Market Insights, the global plates market size was valued at USD 30,900 million in 2025 and is projected to grow from USD 32,877.60 million in 2026 to reach USD 44,834.08 million by 2031, expanding at a CAGR of 6.4% during the forecast period (2026–2031). The plates market growth is primarily driven by expanding global foodservice infrastructure, rising household spending on kitchenware products, and increasing demand for durable and aesthetically appealing dining solutions. Plates remain a fundamental component of dining and food presentation across households, restaurants, hospitality establishments, and catering services worldwide.

The increasing popularity of home dining, fueled by social media-driven food presentation trends and lifestyle upgrades, is encouraging consumers to purchase premium and designer tableware. At the same time, the growth of quick-service restaurants, cloud kitchens, and catering services is generating steady demand for both reusable and disposable plates. Sustainability trends are also reshaping the market landscape, as eco-friendly plates made from bamboo, bagasse, palm leaves, and other biodegradable materials gain traction due to regulatory pressure on plastic waste. Rapid expansion of e-commerce platforms and direct-to-consumer sales channels is further improving product accessibility and brand visibility globally.

Key Market Insights

- Ceramic plates dominate the global market, accounting for nearly 38% of total demand due to their durability, aesthetic appeal, and suitability for both household and commercial use.

- Residential households remain the largest end-use segment, representing approximately 52% of global demand as consumers continue investing in premium kitchenware.

- Asia-Pacific leads the global plates market, driven by strong manufacturing capabilities in China and growing consumer demand across India and Southeast Asia.

- Eco-friendly disposable plates are rapidly gaining popularity, supported by government regulations restricting single-use plastic tableware.

- Online retail platforms are becoming a major distribution channel, allowing consumers to explore product designs, materials, and pricing options easily.

- The global foodservice industry is a major growth driver, with restaurants, hotels, and catering companies creating consistent demand for durable and disposable plates.

What are the latest trends in the plates market?

Growing Demand for Sustainable and Biodegradable Plates

Environmental awareness and government regulations restricting plastic waste are accelerating the adoption of biodegradable plates. Materials such as bagasse, bamboo, palm leaves, and areca leaves are gaining popularity due to their compostable and renewable properties. Restaurants, catering companies, and event organizers are increasingly switching to eco-friendly tableware to comply with environmental regulations and improve brand sustainability credentials. Manufacturers are investing in advanced molding technologies to produce biodegradable plates with improved strength, moisture resistance, and heat tolerance. As sustainability becomes a key purchasing factor, demand for eco-friendly plates is expected to expand significantly across both developed and emerging markets.

Rise of Premium and Designer Tableware

Consumers are increasingly viewing tableware as part of lifestyle and home décor rather than purely functional kitchenware. Premium ceramic, porcelain, and designer plates featuring modern patterns, textured finishes, and artistic designs are gaining traction among urban households. Social media platforms and food presentation trends are encouraging consumers to purchase aesthetically appealing plates that enhance dining experiences. Luxury hospitality establishments are also investing in customized tableware collections to strengthen brand identity and enhance dining ambience. This shift toward designer dining products is creating opportunities for manufacturers to introduce innovative designs and premium product lines.

What are the key drivers in the plates market?

Expansion of the Global Foodservice Industry

The global foodservice industry continues to expand rapidly due to urbanization, rising disposable income, and changing consumer dining habits. Restaurants, cafés, hotels, and catering services require large quantities of durable plates to support daily operations. The growth of quick-service restaurants and cloud kitchens is particularly driving demand for disposable and lightweight plates. Commercial kitchens also prefer durable materials such as porcelain and stainless steel that can withstand frequent washing and heavy use. As global tourism and hospitality infrastructure continue to expand, demand for high-quality tableware is expected to grow steadily.

Rising Household Spending on Kitchenware

Consumers worldwide are increasingly investing in home dining experiences, leading to higher spending on kitchenware products. Plates are among the most frequently purchased tableware items due to wear and tear, evolving design trends, and lifestyle upgrades. Urban households, particularly in emerging economies, are adopting modern dining practices and replacing traditional utensils with contemporary tableware sets. Premium ceramic and porcelain plates are particularly popular among middle-class consumers seeking durable and stylish dining products.

What are the restraints for the global market?

Volatility in Raw Material Prices

The plates manufacturing industry relies on raw materials such as ceramic clay, pulp fibers, stainless steel, plastics, and energy-intensive production processes. Fluctuations in raw material prices can significantly impact manufacturing costs and profit margins. For example, rising energy prices increase the cost of firing ceramic plates, while pulp price fluctuations affect the cost of biodegradable disposable plates. These cost pressures can limit profitability for manufacturers operating in highly competitive markets.

Intense Competition from Low-Cost Manufacturers

The plates market is highly fragmented with numerous regional manufacturers offering low-cost products. In emerging markets, price competition remains intense, making it difficult for premium brands to maintain high margins. Manufacturers must differentiate their products through innovative designs, superior durability, and sustainability features in order to remain competitive.

What are the key opportunities in the plates industry?

Expansion of Eco-Friendly Tableware Manufacturing

Government restrictions on single-use plastics are creating major opportunities for manufacturers producing biodegradable tableware. Plates made from agricultural waste materials such as sugarcane bagasse and palm leaves are gaining widespread acceptance across restaurants, food delivery platforms, and catering services. Companies investing in sustainable manufacturing technologies can capitalize on this rapidly growing demand segment.

E-Commerce and Direct-to-Consumer Sales

Online retail channels are transforming the global tableware market. Consumers increasingly prefer purchasing plates through e-commerce platforms where they can explore a wide variety of designs, compare pricing, and access customer reviews. Manufacturers are leveraging digital marketing strategies and brand-owned online stores to reach consumers directly and expand global market presence.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 30900 Million |

| Market Size in 2026 | USD 32877.60 Million |

| Market Size in 2031 | USD 44834.08 Million |

| CAGR | 6.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Material Type Insights

Ceramic plates dominate the global plates market, accounting for nearly 38% of total market share. Porcelain, bone china, and stoneware plates are widely preferred across residential and commercial applications due to their superior durability, heat resistance, aesthetic appeal, and versatility in both casual and formal dining environments. The leading position of ceramic plates is primarily driven by growing consumer preference for premium dining experiences, increasing home décor awareness, and the expanding hospitality industry worldwide.Porcelain and bone china plates continue to gain traction in premium dining and luxury hospitality settings owing to their lightweight structure, refined finish, and long product lifespan. Stoneware plates are increasingly adopted in contemporary dining due to their rustic appearance and durability, aligning with modern culinary presentation trends.Glass plates represent a smaller but stable segment, primarily used in casual dining settings and modern households that favor minimalist aesthetics. Demand for tempered and decorative glass plates is supported by evolving interior design trends and urban consumer preferences.Metal plates, particularly stainless steel varieties, remain widely used in institutional dining, quick-service restaurants, and emerging markets due to their affordability, durability, and ease of maintenance. Their strong adoption in schools, healthcare facilities, and large-scale catering operations continues to sustain segment demand.Plastic and melamine plates maintain popularity for lightweight, reusable, and outdoor dining applications, including picnics, travel, and catering events. However, environmental concerns are gradually reshaping demand patterns.Biodegradable plates manufactured from bamboo, bagasse, and palm leaves are emerging as the fastest-growing material category. Growth in this segment is driven by increasing environmental regulations, rising consumer awareness regarding sustainability, and the global shift toward eco-friendly disposable tableware solutions across foodservice and event catering industries.

Product Type Insights

Dinner plates account for the largest share of the market, contributing nearly 41% of global demand. Their dominance is driven by universal usage across households, restaurants, hotels, and institutional dining environments. Replacement demand, growing household formation rates, and the expansion of organized foodservice establishments remain key drivers supporting this segment’s leadership position.Salad plates and dessert plates represent smaller but steadily growing segments as consumers increasingly purchase coordinated tableware collections and multi-piece dining sets. Rising interest in aesthetic food presentation, social dining culture, and premium home entertaining trends are accelerating adoption.Charger plates and serving platters are widely used in hospitality and luxury dining environments to enhance visual presentation and customer experience. Growth in fine dining restaurants, banquet services, and event management industries is contributing significantly to demand for decorative and specialty plates.Divided plates are gaining traction in institutional and healthcare dining settings due to their functional design, portion control benefits, and suitability for elderly care, hospitals, and school meal programs. Increasing focus on organized food distribution and nutritional management further supports segment expansion.

Distribution Channel Insights

Offline retail channels such as supermarkets, department stores, hypermarkets, and specialty kitchenware shops account for nearly 58% of total sales. Consumers continue to prefer physical retail outlets for tableware purchases because they can evaluate product weight, texture, finish, and durability before making purchasing decisions. Immediate product availability and in-store brand experiences further strengthen offline dominance.The leading driver for offline channel growth is the continued expansion of organized retail infrastructure, particularly in emerging economies, along with strong impulse purchasing behavior associated with home improvement and lifestyle shopping.However, online platforms are rapidly gaining market share as digital commerce expands globally. E-commerce marketplaces provide extensive product variety, price comparisons, customer reviews, and doorstep delivery convenience. Increasing smartphone penetration, digital payment adoption, and promotional pricing strategies are attracting younger consumers and urban buyers.Direct-to-consumer brand websites and online home décor platforms are also contributing to growth by offering customized collections, premium product lines, and exclusive designs.

End-Use Insights

The residential sector dominates the plates market, accounting for approximately 52% of global demand. Household consumption remains strong as consumers increasingly replace older tableware and invest in stylish, coordinated dining products that complement modern home interiors. Rising disposable incomes, urbanization, and the growing culture of home dining and social gatherings serve as the primary drivers for residential segment leadership.The foodservice industry represents the fastest-growing end-use segment, driven by rapid expansion of restaurants, hotels, cafés, cloud kitchens, and catering services worldwide. Increasing frequency of dining out, growth of food delivery services, and rising tourism activities significantly contribute to commercial tableware demand.Event catering and institutional dining sectors are also contributing to market expansion, particularly through rising demand for disposable and biodegradable plates used in large-scale gatherings, corporate events, healthcare facilities, and educational institutions.

Explore more data points, trends and opportunities Download Free Sample Report

Plates Market Segmentations

By Material Type

- Ceramic Plates

- Glass Plates

- Metal Plates

- Plastic & Melamine Plates

- Biodegradable & Eco-Friendly Plates

By Product Type

- Dinner Plates

- Salad Plates

- Dessert Plates

- Serving Plates & Platters

- Charger Plates

- Divided Plates

By Distribution Channel

- Online Retail & E-Commerce Platforms

- Supermarkets & Hypermarkets

- Specialty Kitchenware Stores

- Department Stores

- Wholesale & Institutional Supply

By End Use

- Residential Households

- Restaurants & Foodservice Chains

- Hotels & Hospitality Industry

- Catering & Events

- Institutional Dining

Regional Insights

Asia-Pacific

Asia-Pacific holds the largest share of the global plates market, accounting for approximately 37% of total demand. China remains the dominant manufacturing hub for ceramic tableware, benefiting from large-scale production capabilities, cost efficiency, and strong export networks supplying global markets.Regional growth is primarily driven by rapid urbanization, expanding middle-class populations, rising disposable income levels, and changing consumer lifestyles. India is emerging as a key growth market due to increasing household consumption, expanding hospitality infrastructure, and rising adoption of modern kitchenware products. Additionally, government initiatives supporting manufacturing and retail expansion are strengthening regional supply chains.Southeast Asian countries such as Thailand, Indonesia, and Vietnam are witnessing rising demand fueled by tourism growth, increasing restaurant penetration, and the expansion of organized retail and e-commerce sectors. Growing environmental awareness is also accelerating adoption of biodegradable plates across the region.

North America

North America accounts for nearly 24% of the global plates market, led by the United States. The region benefits from a highly developed foodservice ecosystem comprising restaurant chains, catering companies, and hospitality establishments that require durable and aesthetically appealing tableware.Key regional growth drivers include high consumer spending on home décor, strong replacement demand, and increasing preference for premium and designer tableware products. The rising popularity of home entertaining and seasonal dining collections further supports market expansion.Additionally, growing sustainability awareness and regulatory pressure to reduce plastic waste are encouraging adoption of biodegradable and compostable disposable plates across catering services, quick-service restaurants, and food delivery platforms.

Europe

Europe represents approximately 22% of global market share, supported by strong cultural emphasis on dining aesthetics and premium tableware craftsmanship. Countries such as Germany, France, Italy, and the United Kingdom demonstrate consistent demand for high-quality ceramic and porcelain plates.Regional growth is driven by consumer preference for sustainable products, premiumization trends, and increasing demand for artisanal and designer tableware collections. Strict environmental regulations across the European Union are also accelerating innovation in recyclable and biodegradable plate materials.The region’s well-established hospitality and tourism sectors further contribute to steady commercial demand for durable and visually appealing tableware solutions.

Latin America

Latin America is witnessing gradual growth in the plates market, particularly in Brazil and Mexico. Expanding urban populations, improving economic conditions, and rising disposable incomes are encouraging greater spending on kitchenware and dining products.Growth drivers include the expansion of casual dining restaurants, increasing adoption of organized retail channels, and rising consumer interest in modern home dining experiences. Local manufacturing expansion and affordable product offerings are also improving market accessibility.

Middle East & Africa

The Middle East and Africa region is experiencing increasing demand for premium tableware due to rapid hospitality infrastructure development and tourism expansion. Countries such as the UAE and Saudi Arabia are investing heavily in luxury hotels, fine dining restaurants, and large-scale entertainment projects, which is supporting demand for high-end ceramic and designer plates.Additional growth drivers include rising expatriate populations, increasing disposable income levels in Gulf countries, and growing adoption of western dining culture. In Africa, urbanization and retail modernization are gradually supporting market penetration, particularly in metropolitan areas.

Key Players in the Plates Market

- Arc Holdings

- Libbey Inc.

- Fiskars Group

- Steelite International

- Churchill China

- Corelle Brands

- Villeroy & Boch

- Noritake Co., Ltd.

- Lenox Corporation

- Luminarc

- Royal Doulton

- Homer Laughlin China Company

- Rosenthal GmbH

- Bormioli Rocco

- La Opala RG Limited