Plastic Houseware Product Market Size

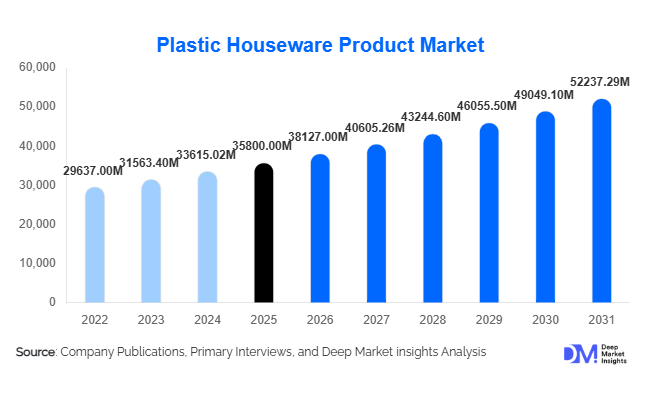

According to Deep Market Insights, the global plastic houseware product market size was valued at USD 35,800 million in 2025 and is projected to grow from USD 38,127.00 million in 2026 to reach USD 52,237.29 million by 2031, expanding at a CAGR of 6.5% during the forecast period (2026–2031). The market growth is primarily driven by increasing urbanisation, rising demand for cost-effective and durable household products, and expanding penetration of organised retail and e-commerce channels. Plastic houseware products continue to gain widespread adoption due to their lightweight nature, versatility, and affordability compared to alternative materials such as glass, metal, and wood.

Key Market Insights

- Plastic houseware products remain essential household items globally, driven by frequent replacement cycles and everyday utility.

- Asia-Pacific dominates the market, supported by large-scale manufacturing and strong domestic consumption in China and India.

- Eco-friendly and recyclable plastics are gaining traction as sustainability concerns reshape consumer preferences and regulations.

- E-commerce channels are rapidly expanding, enabling wider product accessibility and direct-to-consumer engagement.

- Economy and mid-range segments account for the majority of demand, particularly in emerging markets with price-sensitive consumers.

- Product innovation in modular storage and design aesthetics is driving premiumization in developed markets.

What are the latest trends in the plastic houseware product market?

Sustainability and Recycled Plastics Adoption

Manufacturers are increasingly adopting recycled and bio-based plastics to address environmental concerns and comply with regulatory requirements. The shift toward BPA-free, reusable, and recyclable products is gaining momentum, particularly in North America and Europe. Companies are investing in circular economy models, incorporating post-consumer recycled materials into product lines while maintaining durability and design appeal. Sustainability certifications and eco-labelling are becoming key differentiators, influencing consumer purchase decisions and allowing brands to command premium pricing.

Rise of Modular and Space-Saving Designs

With urban living spaces becoming smaller, especially in densely populated cities, there is a growing demand for compact, stackable, and multifunctional plastic houseware products. Modular storage systems, collapsible containers, and multi-use kitchen tools are gaining popularity among urban consumers. These designs not only optimise space but also enhance convenience and organisation. Manufacturers are focusing on ergonomic designs and aesthetic appeal to cater to modern households, blending functionality with style.

What are the key drivers in the plastic houseware product market?

Growing Urbanisation and Household Formation

Rapid urbanisation, particularly in the Asia-Pacific and Africa, is driving demand for basic and affordable household products. Increasing nuclear families and rising housing construction are creating sustained demand for plastic houseware items such as storage containers, cleaning tools, and kitchen accessories.

Cost Efficiency and Versatility

Plastic products offer significant cost advantages over traditional materials, making them accessible to a wide consumer base. Their lightweight nature, durability, and corrosion resistance further enhance their appeal across residential and commercial applications.

Expansion of Retail and E-commerce Channels

The growth of supermarkets, hypermarkets, and online platforms has improved product availability and visibility. E-commerce platforms, in particular, are enabling manufacturers to reach broader audiences and introduce innovative products with faster market penetration.

What are the restraints for the global market?

Environmental Regulations and Sustainability Concerns

Stringent regulations on plastic usage, particularly single-use plastics, are posing challenges for manufacturers. Compliance with environmental standards requires significant investment in R&D and sustainable material sourcing, increasing production costs.

Raw Material Price Volatility

Fluctuations in petrochemical prices directly impact the cost of plastic production. This volatility affects profit margins and creates pricing uncertainties for manufacturers, particularly in highly competitive markets.

What are the key opportunities in the plastic houseware product market?

Emerging Market Expansion

Rapid economic growth and urbanisation in countries such as India, Indonesia, and Nigeria present significant opportunities for market expansion. Increasing disposable incomes and improving living standards are driving demand for both basic and mid-range houseware products. Establishing localised manufacturing and distribution networks can help companies tap into these high-growth markets.

E-commerce and Direct-to-Consumer Models

The rise of online retail platforms is enabling manufacturers to bypass traditional distribution channels and directly engage with consumers. This allows for better margin control, personalised marketing, and rapid product launches. Data-driven insights from online platforms also help companies tailor offerings to evolving consumer preferences.

Innovation in Premium and Design-Led Products

In developed markets, there is a growing demand for aesthetically appealing and high-quality plastic houseware products. Premium segments focusing on design, durability, and sustainability offer higher margins and differentiation opportunities. Collaborations with designers and investment in product innovation can help companies capture this segment.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 35800 Million |

| Market Size in 2026 | USD 38127 Million |

| Market Size in 2031 | USD 52237.29 Million |

| CAGR | 6.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Kitchenware dominates the plastic houseware product market, accounting for approximately 32% of the global market share in 2025. This leadership position is primarily driven by the segment’s high usage frequency and essential role in daily household activities such as food storage, preparation, and consumption. The increasing trend of home cooking, meal prepping, and demand for airtight, durable, and microwave-safe containers has further strengthened growth in this segment. Additionally, rising health awareness has led to higher demand for BPA-free and food-grade plastic kitchen products, reinforcing its dominance globally.

Cleaning and utility products represent the second-largest segment, supported by their indispensable role in maintaining hygiene across residential and commercial spaces. The segment benefits from consistent demand for buckets, dustbins, and cleaning tools, particularly in emerging economies. Furniture and storage products are witnessing accelerated growth due to increasing urbanisation and shrinking living spaces, driving demand for lightweight, stackable, and portable storage solutions. Bathroom accessories and home décor segments are steadily expanding, particularly in urban and developed markets where consumers are increasingly prioritising aesthetics, organisation, and design-led products alongside functionality.

Material Type Insights

Polypropylene (PP) leads the material segment with approximately 38% share in 2025, owing to its superior balance of durability, flexibility, chemical resistance, and cost-effectiveness. Its widespread applicability in kitchenware, storage containers, and utility products makes it the preferred material for manufacturers. The growth of PP is further supported by its recyclability and suitability for food-grade applications, aligning with evolving consumer and regulatory requirements.

Polyethene (PE) holds a significant share, particularly in utility and cleaning products, due to its high impact resistance and moisture-proof properties. Engineering plastics such as ABS are gaining traction in premium and high-performance applications, especially in furniture and aesthetically designed products, where strength and finish are critical. Meanwhile, recycled plastics are emerging as the fastest-growing material category, driven by increasing environmental concerns, regulatory pressures, and corporate sustainability commitments. Manufacturers are investing in advanced recycling technologies to incorporate post-consumer materials without compromising product quality.

Distribution Channel Insights

Offline retail continues to dominate the distribution landscape, accounting for approximately 55% of total sales in 2025. This dominance is largely attributed to the strong presence of traditional retail networks, including local stores, wholesalers, and supermarkets, particularly in developing regions where consumer preference for physical inspection remains high. Immediate product availability, lower price points, and established supply chains further support offline sales.

However, e-commerce is the fastest-growing distribution channel, driven by increasing internet penetration, smartphone usage, and the convenience of home delivery. Online platforms enable consumers to access a wider variety of products, compare prices, and benefit from promotional discounts. The growth of direct-to-consumer (D2C) models is also enabling manufacturers to enhance margins and build stronger brand relationships. Institutional and B2B sales channels are expanding steadily, particularly due to rising demand from hospitality, healthcare, and corporate sectors, where bulk purchasing and standardised product requirements are common.

End-Use Insights

Residential households dominate the end-use segment, contributing approximately 68% of the global market in 2025. This is primarily driven by the essential nature of plastic houseware products in daily life, combined with frequent replacement cycles and increasing household formation, especially in urban areas. Rising disposable incomes and changing lifestyles are further encouraging consumers to upgrade to more durable, aesthetically appealing, and multifunctional products.

Commercial applications, including hotels, restaurants, and offices, represent the fastest-growing segment. Expansion of the global hospitality industry, along with increasing demand for cost-effective and durable solutions, is driving adoption in this sector. Institutional demand from schools, hospitals, and government facilities is also increasing steadily, supported by hygiene requirements, budget constraints, and the need for large-scale procurement. The growing emphasis on sanitation and cleanliness, particularly post-pandemic, has further strengthened demand across non-residential end-use segments.

Explore more data points, trends and opportunities Download Free Sample Report

Plastic Houseware Product Market Segmentations

By Product Type

- Kitchenware

- Cleaning & Utility Products

- Furniture & Storage

- Bathroom Accessories

- Home Décor & Miscellaneous

By Material Type

- Polypropylene (PP)

- Polyethylene (PE)

- Polyvinyl Chloride (PVC)

- Polystyrene (PS)

- ABS & Engineering Plastics

- Recycled Plastics

By Distribution Channel

- Offline Retail

- E-commerce Platforms

- Institutional/B2B Sales

By End-Use

- Residential Households

- Commercial

- Institutional

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global plastic houseware product market with approximately 42% share in 2025, led by China and India. China accounts for nearly 22% of global demand, supported by its robust manufacturing ecosystem, low production costs, and strong export capabilities. India is the fastest-growing market in the region, with a CAGR of around 8%, driven by rapid urbanisation, rising disposable incomes, and increasing penetration of organised retail. Government initiatives such as “Make in India,” along with expanding middle-class populations and housing demand, are key drivers supporting regional growth. Additionally, the availability of low-cost labour and raw materials further strengthens the Asia-Pacific’s dominance.

North America

North America holds around 18% of the global market share, with the United States being the primary contributor. The region’s growth is driven by strong consumer preference for premium, durable, and eco-friendly products. High disposable incomes and a well-established retail infrastructure support consistent demand. Additionally, increasing awareness regarding sustainability and regulatory emphasis on recyclable materials is encouraging innovation in product design and materials. The rapid growth of e-commerce and direct-to-consumer channels is also significantly contributing to market expansion in this region.

Europe

Europe accounts for approximately 16% of the market, with major contributions from Germany, France, and the United Kingdom. The region’s growth is strongly influenced by stringent environmental regulations and policies promoting the use of recyclable and sustainable materials. Consumers in Europe exhibit a high preference for eco-friendly, high-quality, and aesthetically designed products, driving demand for premium segments. Additionally, the presence of established manufacturers and strong retail networks supports steady market growth. Innovation in biodegradable plastics and circular economy initiatives are key driver shaping the regional market.

Middle East & Africa

The Middle East & Africa region represents around 12% of the global market, with growth driven by rapid urban expansion and increasing demand for affordable household products. Countries such as the UAE and South Africa are leading demand due to rising construction activities and growing urban populations. Increasing tourism and hospitality sector expansion in the Middle East are also contributing to higher demand for plastic houseware products. Additionally, improving retail infrastructure and rising consumer spending are supporting market growth across the region.

Latin America

Latin America holds nearly 12% market share, led by Brazil and Mexico. The region’s growth is supported by economic recovery, urbanisation, and the expansion of organised retail channels. Rising middle-class populations and increasing demand for affordable and durable household products are key drivers. Furthermore, improving supply chain infrastructure and growing penetration of e-commerce platforms are enhancing product accessibility. Government initiatives supporting domestic manufacturing and import substitution are also contributing to steady market expansion in the region.

Key Players in the Plastic Houseware Product Market

- Tupperware Brands Corporation

- Newell Brands Inc.

- Rubbermaid Commercial Products

- LocknLock Co. Ltd.

- IKEA

- Nilkamal Limited

- Supreme Industries Ltd.

- Dart Container Corporation

- Curver (Keter Group)

- Sterilite Corporation

- Hamilton Housewares Pvt. Ltd.

- Cello World Ltd.

- Sistema Plastics

- Plast Team Group

- Signoraware