Plain Gold Jewellery Market Size

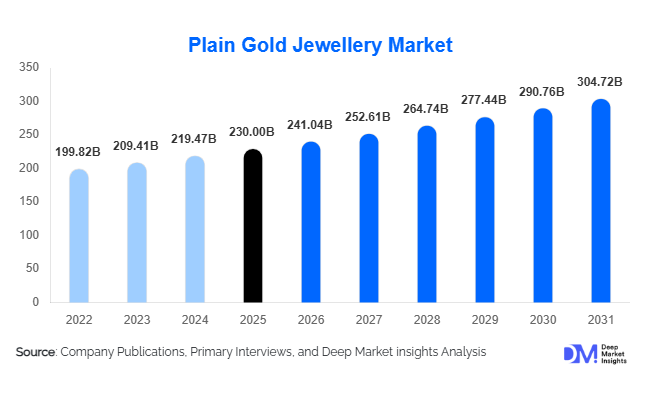

According to Deep Market Insights, the global plain gold jewellery market was valued at USD 230 billion in 2025 and is expected to grow from USD 241.04 billion in 2026 to USD 304.72 billion by 2031, registering a CAGR of 4.8% during the forecast period (2026–2031). The market growth is primarily driven by rising cultural and traditional demand for gold jewellery in emerging economies, increasing preference for gold as a dual-purpose asset for adornment and investment, and steady growth in disposable income across developing regions. In addition, expanding retail networks and growing digital penetration in jewellery sales are further supporting global market expansion.

Key Market Insights

- Plain gold jewellery continues to dominate traditional consumption markets, particularly in Asia-Pacific and the Middle East, where cultural significance strongly influences purchasing behavior.

- Investment-driven demand is rising globally, with consumers increasingly viewing gold jewellery as a liquid financial asset during inflationary cycles.

- Asia-Pacific dominates global consumption, led by India and China, which together account for a significant share of global demand.

- Mid-range and lightweight jewellery formats are gaining popularity, driven by affordability concerns and changing urban lifestyles.

- Offline retail remains dominant, but online jewellery sales are expanding rapidly due to transparency, certification, and convenience.

- Sustainability and ethical sourcing are emerging trends, influencing brand positioning and consumer trust in developed markets.

What are the latest trends in the plain gold jewellery market?

Shift Toward Lightweight and Minimalist Jewellery

Consumers are increasingly shifting toward lightweight plain gold jewellery, particularly in urban markets where daily-wear affordability and comfort are key priorities. This trend is especially strong in the 18K and 22K segments, where buyers seek a balance between purity, durability, and cost efficiency. Manufacturers are responding with design innovations that reduce gold weight without compromising visual appeal. This shift is also influenced by rising gold prices, encouraging consumers to prefer smaller, modular, and versatile jewellery pieces that can be worn across occasions.

Digital Transformation of Jewellery Retail

The market is witnessing rapid digitalisation through e-commerce platforms, virtual try-ons, and AI-based recommendation systems. Consumers are increasingly comfortable purchasing gold jewellery online due to certification transparency, return policies, and digital gold integration. Brands are investing in omnichannel strategies that combine offline trust with online convenience. This transformation is expanding access to younger demographics and non-traditional buyers, significantly widening the market base.

What are the key drivers in the plain gold jewellery market?

Cultural and Traditional Demand Strength

Gold jewellery remains deeply embedded in cultural traditions, particularly in countries such as India, China, and across the Middle East. Weddings, festivals, and religious ceremonies consistently generate strong baseline demand. In India alone, wedding-related gold purchases account for a major portion of annual consumption, reinforcing stable long-term market growth regardless of economic fluctuations.

Gold as a Safe-Haven Investment Asset

Plain gold jewellery serves both ornamental and investment purposes, making it highly attractive during inflationary periods and economic uncertainty. Consumers prefer gold as it retains intrinsic value and offers liquidity compared to other luxury goods. This dual functionality significantly strengthens demand across both developed and emerging markets, especially during currency volatility and geopolitical tensions.

Rising Disposable Income in Emerging Economies

Expanding middle-class populations across Asia-Pacific, Africa, and Latin America are driving increased spending on lifestyle and luxury goods, including gold jewellery. Urbanisation and income growth are enabling consumers to upgrade from low-purity to mid- and high-purity jewellery segments, further boosting overall market expansion.

What are the restraints for the global market?

Volatility in Gold Prices

Fluctuations in global gold prices directly impact consumer affordability and purchasing timing. Sharp price increases often lead to delayed or reduced jewellery purchases, particularly in price-sensitive markets, thereby affecting short-term demand cycles.

Growing Substitution from Alternative Jewellery Categories

The increasing popularity of diamond, platinum, and fashion jewellery is creating competitive pressure on plain gold jewellery demand, especially among younger consumers in Western markets. Changing fashion preferences and lifestyle-driven consumption are gradually diversifying jewellery demand away from traditional gold dominance.

What are the key opportunities in the plain gold jewellery industry?

Expansion in Emerging Markets

Rapid growth in emerging economies such as Indonesia, Vietnam, Nigeria, and Brazil presents significant opportunities for market expansion. Rising income levels, urbanisation, and cultural acceptance of gold jewellery are driving new demand pools. These regions remain underpenetrated compared to established markets, offering strong long-term growth potential for global brands.

Growth in Digital Gold and Omnichannel Retail

The integration of digital gold platforms with physical jewellery retail is creating new consumption models. Consumers can now invest in digital gold and convert it into jewellery, enhancing flexibility and accessibility. Omnichannel strategies are also enabling brands to reach younger demographics more effectively, expanding customer acquisition channels.

Ethical and Sustainable Gold Sourcing

Increasing awareness around responsible sourcing is creating opportunities for brands that adopt ethical mining and transparent supply chains. Certified and sustainably sourced gold jewellery is gaining traction in developed markets, helping companies differentiate and build long-term consumer trust.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 230 Billion |

| Market Size in 2026 | USD 241.04 Billion |

| Market Size in 2031 | USD 304.72 Billion |

| CAGR | 4.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Chains and necklaces continue to dominate the global plain gold jewellery market, accounting for an estimated 28% share of the total market in 2025. This leadership is primarily driven by their universal acceptance across genders, age groups, and cultural contexts. Chains are widely used for both daily wear and ceremonial purposes, making them a highly versatile product category. In addition, their relatively lower making charges compared to intricate jewellery designs make them more attractive from a value-retention perspective, further strengthening demand in investment-conscious markets such as India, China, and the Middle East.

Rings and earrings collectively represent a significant portion of the market, driven by their strong association with personal milestones such as engagements, weddings, and gifting occasions. Earrings, in particular, benefit from high repeat purchase rates due to evolving fashion trends. Bracelets and bangles hold substantial importance in Asia-Pacific markets, especially in India and Southeast Asia, where they are deeply embedded in cultural traditions and wedding customs. Coins and bars, while smaller in overall volume, are witnessing increased demand as hybrid products that combine ornamental use with investment value. This segment is particularly gaining traction during periods of economic uncertainty and high inflation. Across all product categories, a key trend shaping growth is the increasing focus on lightweight and modular jewellery designs. Manufacturers are innovating to reduce gold content per unit while maintaining visual appeal, enabling affordability and expanding accessibility among younger, urban consumers. This trend is expected to further accelerate demand across mid-range and premium segments globally.

End-Use Insights

Personal consumption remains the largest end-use segment, accounting for approximately 55% of global demand in 2025. This dominance is driven by everyday usage, fashion preferences, and cultural practices, particularly in emerging economies where gold jewellery is an integral part of daily life. The segment is further supported by increasing urbanization and rising disposable incomes, which enable consumers to purchase gold jewellery more frequently for personal use rather than only for special occasions. The investment segment is witnessing steady growth, expanding at a faster pace than overall market growth, as consumers increasingly view plain gold jewellery as a liquid and inflation-resistant financial asset. Unlike other forms of jewellery, plain gold items retain higher intrinsic value due to minimal design costs, making them more attractive for wealth preservation. This trend is particularly strong in regions experiencing currency volatility and economic uncertainty.

Wedding and gifting segments also play a critical role in market expansion, especially in South Asia and the Middle East, where gold jewellery is a traditional and often mandatory component of matrimonial ceremonies. In India, for instance, wedding-related purchases account for a substantial portion of annual gold demand. Additionally, gifting during festivals and religious events further boosts seasonal demand cycles. Increasingly, gold jewellery is also being integrated into structured wealth management strategies in emerging markets, reinforcing its dual role as both an adornment and a long-term financial asset.

Explore more data points, trends and opportunities Download Free Sample Report

Plain Gold Jewellery Market Segmentations

By Product Type

- Chains & Necklaces

- Rings

- Earrings

- Bracelets & Bangles

- Coins & Bars

- Anklets & Toe Rings

By Gold Purity (Karatage)

- 24K Pure Gold Jewellery

- 22K Traditional Jewellery

- 18K Mid-Purity Jewellery

- 14K & Below Fashion Jewellery

By Price Range

- Economy Segment (Below USD 300)

- Mid-Range (USD 300 – USD 1,500)

- Premium (USD 1,500 – USD 5,000)

- Luxury Segment (Above USD 5,000)

By End-Use

- Personal Consumption

- Investment / Wealth Preservation

- Wedding Jewellery

- Gifting

By Distribution Channel

- Offline Retail Stores

- Online Jewellery Platforms

- Brand-Owned Showrooms (D2C)

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global plain gold jewellery market, accounting for approximately 60% of total demand in 2025. The region’s leadership is driven by strong cultural affinity, high population density, and consistent demand across both consumption and investment segments. India contributes nearly 25% of global demand, primarily fueled by weddings, festivals, and religious ceremonies. China accounts for around 20%, supported by rising urban incomes, increasing middle-class consumption, and growing interest in gold as a financial asset.

Key growth drivers in the region include rapid urbanization, an expanding middle-class population, and increasing female workforce participation, which is boosting independent purchasing power. Government initiatives such as gold monetization schemes in India and evolving retail infrastructure in China are also enhancing market accessibility. Additionally, strong rural demand combined with increasing penetration of organized jewellery retail chains continues to sustain long-term growth in this region.

Middle East & Africa

The Middle East & Africa region accounts for approximately 15% of the global market, with strong demand from countries such as the UAE, Saudi Arabia, and South Africa. Gold jewellery holds significant cultural and financial importance in this region, often serving as a primary store of wealth. The UAE, in particular, acts as a global trading hub due to its favorable tax structure, high gold liquidity, and strong re-export capabilities.

Regional growth is driven by high per capita income levels in Gulf countries, increasing tourism-driven retail sales, and a strong preference for high-purity gold jewellery (22K and 24K). Additionally, rising urbanization and improving retail infrastructure in African economies are supporting demand expansion. Cultural practices, including bridal gifting and dowry traditions, further reinforce steady consumption patterns.

Europe

Europe holds approximately 10% share of the global market, with demand concentrated in countries such as Italy, the UK, Germany, and France. Italy serves as a major manufacturing and export hub, known for its craftsmanship and design innovation. Western European markets are characterized by stable demand for minimalist and lightweight gold jewellery, driven by fashion trends and changing consumer preferences.

Growth in Europe is supported by increasing demand for ethically sourced and sustainably produced gold jewellery, as consumers become more environmentally conscious. Additionally, strong luxury retail networks, high purchasing power, and the influence of global fashion trends contribute to steady market expansion. Tourism also plays a role, particularly in countries like Italy and France, where jewellery purchases are linked to luxury shopping experiences.

North America

North America accounts for approximately 8% of the global market, led by the United States. Demand in this region is primarily driven by fashion-oriented jewellery consumption rather than traditional or investment-based purchases. Consumers show a strong preference for lightweight, minimalist, and branded gold jewellery, particularly within younger demographics.

Key growth drivers include rising disposable income, increasing adoption of online jewellery platforms, and growing awareness of gold jewellery as a long-term value asset. The expansion of direct-to-consumer (D2C) brands and digital retail channels is also transforming the competitive landscape. Additionally, demand is supported by seasonal gifting occasions such as holidays and anniversaries.

Latin America

Latin America contributes approximately 7% of the global market, with Brazil and Mexico emerging as key demand centers. The region is experiencing steady growth driven by improving economic conditions, rising middle-class income, and increasing exposure to global jewellery trends.

Growth drivers in Latin America include urbanization, expansion of organized retail channels, and growing consumer awareness regarding gold as both a fashion and investment asset. Cultural events and celebrations also contribute to periodic spikes in demand. Additionally, increasing cross-border trade and imports of gold jewellery are supporting market development, particularly in urban metropolitan areas.

Key Players in the Plain Gold Jewellery Market

- Titan Company Limited

- Chow Tai Fook Jewellery Group

- Rajesh Exports Limited

- Malabar Gold & Diamonds

- Kalyan Jewellers

- Signet Jewelers Limited

- Luk Fook Holdings

- Chow Sang Sang Holdings

- PN Gadgil Jewellers

- Tribhovandas Bhimji Zaveri (TBZ)

- Richemont Group

- Tiffany & Co.

- Damiani Group

- Cartier (Richemont)

- BlueStone Jewellery