Pilates Equipment Market Size

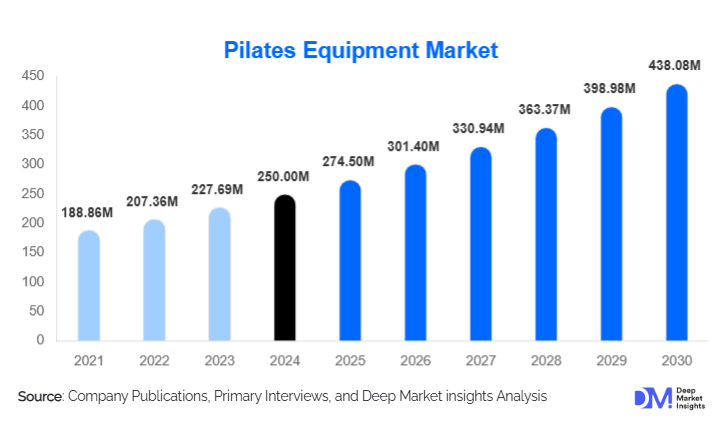

According to Deep Market Insights, the global Pilates equipment market size was valued at USD 250 million in 2025 and is projected to grow from USD 274.50 million in 2026 to reach USD 438.08 million by 2031, expanding at a CAGR of 9.8% during the forecast period (2026–2031). The Pilates equipment market growth is driven by rising global health awareness, increasing adoption of home fitness solutions, expansion of boutique Pilates and wellness studios, and growing rehabilitation-sector demand for low-impact, therapeutic exercise equipment.

Key Market Insights

- Reformers dominate the global product landscape, accounting for over 40% of total market revenue due to their high versatility and widespread adoption by studios and home users.

- Commercial Pilates studios and boutique fitness centers remain the largest end-use segment, benefiting from expanding wellness culture and premium fitness experiences.

- North America holds the largest market share in 2025, supported by strong consumer spending on fitness, high adoption of Pilates studios, and robust home-gym penetration.

- Asia-Pacific is the fastest-growing region, driven by rising middle-class income, urban wellness trends, and the expansion of physiotherapy and rehabilitation clinics.

- Home-fitness demand continues to accelerate, with significant growth in sales of mats, resistance bands, accessories, and portable reformers.

- Technological integration, including smart Pilates reformers, connected workout apps, and eco-friendly materials, is increasingly shaping product innovation.

Latest Market Trends

Rehabilitation-Focused Pilates Solutions Gaining Adoption

Physiotherapy centers, hospitals, and rehabilitation clinics are increasingly integrating Pilates-based training into therapeutic programs. Low-impact motion, core stabilization, posture correction, and controlled muscle engagement make Pilates beneficial for injury recovery and chronic pain management. As healthcare systems emphasize preventive and mobility-enhancing treatments, demand for specialized rehabilitation-grade reformers, stability chairs, and barrels is rising. Manufacturers are collaborating with clinicians to design apparatus tailored for patients with spinal injuries, joint limitations, and age-related mobility decline. This trend positions Pilates as not only a fitness discipline but a medically aligned therapeutic modality, expanding its reach into clinical and institutional settings.

Technology-Enhanced Pilates Equipment

Digitalization is reshaping how Pilates users engage with equipment. Smart reformers with adjustable digital resistance, app-controlled workout programs, integrated performance tracking, and virtual training features are entering the mainstream market. Home users increasingly seek connected fitness experiences, driving manufacturers to integrate Bluetooth, sensors, and guided video instruction into their apparatus. Enhanced pulley systems, frictionless movement technology, eco-conscious materials, and ergonomic designs are also trending. Online Pilates classes and subscription-based virtual training platforms further augment product value, making the equipment part of a holistic digital wellness ecosystem.

Pilates Equipment Market Drivers

Rising Global Health Consciousness and Wellness Lifestyle Shift

Consumers are increasingly prioritizing holistic wellness, posture correction, flexibility, and stress reduction. Pilates aligns closely with these values, offering low-impact exercise suitable for varied age groups and fitness levels. The surge in wellness-oriented lifestyles, especially among professionals, older adults, and women, continues to drive equipment adoption across both home and commercial environments.

Acceleration of the Home-Fitness Economy

The post-pandemic shift to home-based fitness remains strong, with hybrid work models enabling more at-home workout routines. Affordable, space-efficient Pilates gear, mats, resistance bands, foam rollers, and portable reformers have become essential home gym equipment. Direct-to-consumer e-commerce channels, influencer-led workouts, and virtual Pilates classes have amplified this segment’s growth, making home users a central revenue driver.

Growing Use of Pilates in Rehabilitation and Senior Wellness

Pilates has gained significant traction within physiotherapy, orthopedic rehabilitation, and senior-care environments due to its mobility-enhancing and low-strain nature. Clinics are investing in reformers, chairs, and barrel systems tailored for therapeutic use. Aging populations worldwide and the rising incidence of musculoskeletal conditions further increase demand for professionally certified, medical-grade Pilates equipment.

Market Restraints

High Cost of Premium Pilates Apparatus

Large equipment such as reformers, cadillacs, and towers is expensive, restricting adoption in low- and middle-income markets. High-quality materials, precision engineering, and import tariffs raise final costs. For many consumers and small studios, budget limitations remain a critical barrier to equipment purchase or upgrade cycles.

Fragmented Market and Lack of Standardization

The global Pilates equipment industry lacks uniform safety and performance standards. Quality variation, especially among small, emerging manufacturers, creates inconsistency that can hinder adoption in professional clinical environments. Certification gaps, inconsistent product durability, and lack of regulatory oversight complicate market expansion and institutional procurement.

Pilates Equipment Market Opportunities

Expansion of Home-Fitness and Hybrid Wellness Ecosystems

The booming home-fitness economy creates opportunities for companies to design compact, foldable, entry-level apparatus that fit small spaces while offering studio-like performance. Subscription-based virtual Pilates platforms can also integrate with equipment, enabling hybrid digital experiences. Bundled equipment + digital class packages represent a lucrative business model for both new entrants and established brands.

Technological Innovation and Smart Pilates Products

Smart reformers, app-integrated Pilates apparatus, digital resistance controls, and AI-driven movement corrections present a major avenue for product differentiation. As consumers increasingly seek connected fitness experiences similar to smart bikes and rowers, manufacturers can develop high-margin smart Pilates equipment that enhances user engagement, performance tracking, and subscription-based training.

Rehabilitation and Healthcare Integration

The growing role of Pilates in physiotherapy, chiropractic care, orthopedic recovery, and geriatric mobility programs creates robust long-term demand. Manufacturers offering certified therapeutic-grade apparatus can serve clinics, hospitals, wellness centers, and senior-care facilities. Governments promoting preventive healthcare provide an additional structural opportunity for institutional expansion.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 250 Million |

| Market Size in 2026 | USD 274.50 Million |

| Market Size in 2031 | USD 438.08 Million |

| CAGR | 9.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Reformers dominate the market, accounting for approximately 40–45% of global revenue in 2025. Their versatility, adaptability for strength and flexibility training, and widespread use across studios, rehab centers, and homes make them the cornerstone of Pilates practice. Chairs, barrels, and cadillacs represent the mid-tier apparatus segment, while mats, resistance bands, rings, and portable accessories capture high-volume but lower-margin consumer markets. Increased demand for lightweight, foldable reformers is driving premium product innovation tailored for home users.

Application Insights

Commercial Pilates studios and boutique fitness centers remain the largest application segment due to high equipment density requirements. Rehabilitation clinics increasingly adopt Pilates for spine, knee, and shoulder therapy, making therapeutic applications one of the fastest-growing categories. Home fitness applications continue to expand rapidly, with consumers integrating Pilates into daily wellness routines. Corporate wellness programs, hotel fitness suites, and senior wellness centers represent emerging applications that add incremental demand to the market.

Distribution Channel Insights

Offline specialty fitness retailers and B2B studio procurement channels currently dominate, representing over 55% of market share. These channels allow customers to assess equipment quality, durability, and installation needs. However, online channels, including brand-owned e-commerce sites and global retailers, are expanding rapidly. Direct-to-consumer sales are driven by influencer marketing, at-home Pilates trends, and digital demonstrations. Omni-channel strategies combining showrooms with digital platforms are becoming increasingly prevalent.

End-User Insights

Commercial users, including boutique studios and gyms, lead the market, accounting for 30–35% of global revenue. Home users represent the fastest-growing segment, fueled by rising adoption of small accessories and portable reformers. Rehabilitation clinics and hospitals form a high-value institutional segment due to sustained demand for clinical-grade apparatus. Corporate wellness buyers and senior-care centers are emerging segments contributing to steady growth.

Explore more data points, trends and opportunities Download Free Sample Report

Pilates Equipment Market Segmentations

By Product Type

- Apparatus / Machines

- Portable & Accessories

By End-User / Buyer Type

- Commercial Use

- Home / Personal Use

- Institutional Use

By Distribution Channel

- Offline Retail

- Online Retail / E-commerce

- Hybrid / Omni-channel

Regional Insights

North America

North America remains the largest regional market with a 35–40% share in 2025, driven by high fitness spending, a mature network of Pilates studios, and strong home-gym adoption. The U.S. leads demand, followed by Canada, where physiotherapy-driven Pilates adoption is rising. Premium product uptake, advanced studio infrastructure, and influencer-driven home fitness trends reinforce regional growth.

Europe

Europe holds a 15–20% market share, supported by wellness-oriented consumers and increasing adoption of Pilates in rehabilitation centers. Germany, the U.K., France, Italy, and Spain lead demand. Aging demographics and strong physiotherapy traditions drive equipment purchases, while boutique studio culture continues to expand.

Asia-Pacific

Asia-Pacific is the fastest-growing region with a 20–25% share and strong forecasted growth through 2031. Rising middle-class incomes, urban lifestyles, and the expansion of rehabilitation services fuel demand in China, India, Japan, Australia, and South Korea. Increasing corporate wellness initiatives and digital fitness communities further accelerate growth.

Latin America

Latin America accounts for 5–7% of global revenue, led by Brazil, Mexico, and Argentina. Boutique fitness culture is gradually expanding, although affordability constraints limit the adoption of premium equipment. Growth is driven by younger urban populations seeking wellness-focused routines.

Middle East & Africa

MEA represents 3–5% of global demand. The UAE, Saudi Arabia, and Qatar lead Pilates adoption due to high-income populations and rising wellness infrastructure. In Africa, South Africa shows the most robust demand, while growth in other countries remains modest due to economic constraints.

Key Players in the Pilates Equipment Market

- Balanced Body Inc.

- Merrithew Corporation

- Gratz Industries

- Stamina Products Inc.

- Peak Pilates

- XTF Fitness

- Align-Pilates

- AeroPilates

- BASI Systems

- Elina Pilates

- Mad Dogg Athletics

- AGM Group

- Power Pilates

- ReformerFit

- Pilates Design LLC