Philanthropy Fund Market Size

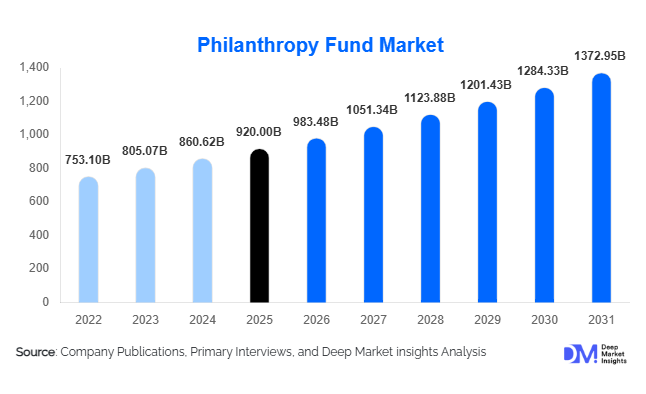

According to Deep Market Insights, the global philanthropy fund market size was valued at USD 920 billion in 2025 and is projected to grow from USD 983.48 billion in 2026 to reach USD 1,372.95 billion by 2031, expanding at a CAGR of 6.9% during the forecast period (2026–2031). The philanthropy fund market growth is primarily driven by rising global wealth concentration, increasing institutionalization of charitable giving, and the growing adoption of impact-oriented funding models aligned with measurable social outcomes.

Key Market Insights

- Donor-advised funds and private foundations dominate the ecosystem, supported by tax efficiency, flexibility, and long-term capital allocation strategies.

- Healthcare and public health initiatives lead funding allocation, driven by post-pandemic priorities and global health investments.

- North America dominates the global market, accounting for nearly 45% share due to a mature philanthropic infrastructure and favorable regulations.

- Asia-Pacific is the fastest-growing region, supported by rising HNWI populations and regulatory encouragement of CSR-led philanthropy.

- Impact measurement and transparency technologies are becoming essential, influencing donor decisions and fund allocation strategies.

- Blended finance models are gaining traction, enabling philanthropic capital to de-risk private investments in sustainability and development projects.

What are the latest trends in the philanthropy fund market?

Shift Toward Impact-Driven Philanthropy

The philanthropy fund market is increasingly transitioning toward outcome-based funding models where measurable impact is prioritized over traditional grant-making. Donors are demanding accountability through quantifiable metrics such as social return on investment (SROI), leading funds to adopt advanced analytics and reporting frameworks. This shift is particularly prominent among institutional donors and younger high-net-worth individuals, who emphasize transparency and long-term sustainability. As a result, funds are integrating ESG benchmarks, AI-driven impact tracking, and real-time reporting tools to demonstrate effectiveness and build donor trust.

Digitalization and Platform-Based Giving

Technology is reshaping the philanthropy landscape through digital platforms that facilitate donor engagement, fund management, and impact tracking. Online giving platforms, blockchain-based transparency tools, and AI-powered recommendation systems are enhancing the efficiency and scalability of philanthropy funds. These technologies are also enabling cross-border giving and democratizing access to philanthropy by allowing smaller donors to participate through pooled funding models. Digitalization is particularly appealing to younger donors, who prefer seamless, tech-enabled giving experiences aligned with modern financial ecosystems.

What are the key drivers in the philanthropy fund market?

Rising Global Wealth and HNWI Participation

The increasing number of high-net-worth and ultra-high-net-worth individuals globally is a major driver of philanthropy fund growth. Wealth accumulation in regions such as North America, Europe, and the Asia-Pacific is translating into higher allocations toward structured philanthropic vehicles. These funds are often used for legacy planning, tax optimization, and long-term social impact, significantly expanding the capital base of the market.

Institutionalization of Corporate Giving

Corporate social responsibility (CSR) mandates and sustainability commitments are driving structured corporate contributions into philanthropy funds. Governments across various economies are enforcing CSR spending requirements or offering tax incentives, encouraging corporations to channel funds into organized philanthropic structures. This has resulted in consistent capital inflows and increased market stability.

What are the restraints for the global market?

Lack of Standardized Impact Measurement

The absence of universally accepted frameworks for measuring philanthropic impact remains a key challenge. Variability in reporting standards makes it difficult to compare outcomes across funds, reducing transparency and potentially deterring institutional investors seeking data-driven insights.

Regulatory Complexity in Cross-Border Giving

Philanthropy funds operating across borders face diverse regulatory environments, including tax restrictions, compliance requirements, and limitations on foreign contributions. These complexities increase administrative costs and restrict the scalability of global philanthropic initiatives, particularly in emerging markets.

What are the key opportunities in the philanthropy fund market?

Integration of Impact Measurement Technologies

The growing demand for transparency presents significant opportunities for technology providers offering advanced impact measurement solutions. AI, blockchain, and big data analytics can enable real-time tracking of fund utilization and outcomes, improving donor confidence and attracting institutional capital. This technological integration is expected to redefine fund management practices and create competitive differentiation.

Expansion in Emerging Markets Through Policy Support

Emerging economies such as India and China are strengthening regulatory frameworks to encourage structured philanthropy. Mandatory CSR policies, tax incentives, and government-backed initiatives are driving increased participation from corporations and individuals. This creates a fertile environment for new fund managers and cross-border philanthropic vehicles to expand operations and capture untapped demand.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 920 Billion |

| Market Size in 2026 | USD 983.48 Billion |

| Market Size in 2031 | USD 1372.95 Billion |

| CAGR | 6.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Fund Structure Insights

Private foundations continue to represent the largest segment in the philanthropy fund market, accounting for approximately 38% of the global market in 2025. Their leadership is primarily driven by the availability of large, perpetual endowments, strong governance frameworks, and the ability to deploy capital over long investment horizons without liquidity constraints. These entities benefit from tax-advantaged structures and legacy-driven mandates, allowing them to sustain consistent funding flows across economic cycles. Additionally, their institutional credibility and ability to partner with governments and global organizations further reinforce their dominance.

Donor-advised funds (DAFs) are the fastest-growing sub-segment, driven by their operational flexibility, simplified administrative processes, and increasing adoption among high-net-worth individuals seeking structured yet agile giving mechanisms. Community foundations and charitable trusts remain critical for localized and grassroots-level funding, particularly in developing regions. Meanwhile, impact investment funds are emerging as a transformative segment, integrating philanthropic intent with financial returns, and acting as catalytic capital for large-scale development and sustainability projects.

Donor Type Insights

Ultra-high-net-worth individuals (UHNWIs) dominate the donor landscape, contributing nearly 35% of total philanthropic fund assets. Their leadership is driven by significant wealth accumulation, intergenerational wealth transfer trends, and increasing inclination toward legacy and impact-driven giving. UHNWIs are also early adopters of structured vehicles such as private foundations and donor-advised funds, enabling them to deploy capital strategically across multiple causes and geographies.

Corporate donors represent the second-largest segment, fueled by mandatory CSR regulations, ESG commitments, and stakeholder pressure to demonstrate social responsibility. Institutional donors, including NGOs, development finance institutions, and multilateral agencies, contribute substantial capital through structured and programmatic funding initiatives. Retail donors, although smaller in value contribution, are expanding rapidly due to digital platforms and crowdfunding models, democratizing access to philanthropy and enabling pooled contributions at scale.

Cause Focus Insights

Healthcare and public health initiatives lead the philanthropy fund market with an estimated 22% share, primarily driven by increased global focus on healthcare resilience, pandemic preparedness, and access to essential medical services. The sector benefits from strong alignment with government priorities and high visibility of outcomes, making it a preferred area for large-scale funding.

Education and environmental sustainability are among the fastest-growing segments. Education is gaining traction due to digital transformation, edtech adoption, and workforce reskilling needs, particularly in emerging economies. Environmental and climate-focused funding is accelerating rapidly, supported by global decarbonization goals and rising awareness of climate risks. Other sectors, such as poverty alleviation, arts and culture, and human rights, continue to receive consistent funding, ensuring diversification and balanced allocation across social impact areas.

Distribution Model Insights

Direct grant-making remains the dominant distribution model, accounting for approximately 40% of the global market. Its leadership is driven by its simplicity, transparency, and the ability for donors to retain control over fund allocation and beneficiary selection. This model is particularly preferred by private foundations and large institutional donors that require direct oversight of project outcomes.

However, the market is witnessing a gradual shift toward outcome-based funding and blended finance models. These approaches are gaining momentum in large-scale development projects, where measurable impact and financial sustainability are critical. Intermediary-based allocation through NGOs and agencies continues to play a key role in regions with limited direct access, while crowdfunding and pooled funding mechanisms are expanding reach among smaller donors.

Geographic Scope Insights

Domestic philanthropy funds dominate the market with nearly 65% share, driven by regulatory ease, tax benefits, and the preference for localized impact. Donors often prioritize funding within their own countries due to better visibility of outcomes and alignment with national development goals. Cross-border philanthropy is steadily expanding, particularly in sectors such as global health, climate change, and humanitarian aid. This growth is supported by increasing globalization, diaspora wealth, and international collaborations among large foundations. Global multi-region funds are also gaining prominence, enabling diversified impact portfolios and large-scale deployment of capital across multiple geographies.

End-Use Insights

Healthcare remains the largest end-use sector, supported by global spending exceeding USD 12 trillion annually and strong philanthropic contributions toward healthcare infrastructure, disease prevention, and innovation. The sector’s dominance is reinforced by its critical importance and measurable outcomes, making it a preferred focus for large donors.

Education is one of the fastest-growing end-use segments, with funding growth exceeding 7% annually. This growth is driven by increasing demand for digital learning, skill development, and inclusive education initiatives, particularly in emerging markets. Environmental and climate-related applications are witnessing the fastest expansion, supported by global climate finance demand surpassing USD 1 trillion annually. Emerging applications such as technology-driven social innovation, digital inclusion, and sustainable infrastructure are also gaining traction, where philanthropy funds are increasingly used as catalytic capital to unlock larger investments.

Explore more data points, trends and opportunities Download Free Sample Report

Philanthropy Fund Market Segmentations

By Fund Structure

- Private Foundations

- Donor-Advised Funds

- Endowment Funds

- Charitable Trusts

- Community Foundations

- Impact Investment Funds

- Religious/Institutional Funds

By Donor Type

- Ultra-High-Net-Worth Individuals (UHNWIs)

- High-Net-Worth Individuals (HNWIs)

- Corporate Donors (CSR Funds)

- Institutional Donors (NGOs, Multilateral Agencies)

- Retail / Crowd-Based Donors

By Cause Focus

- Healthcare & Public Health

- Education

- Environmental Sustainability

- Poverty Alleviation & Social Welfare

- Arts, Culture & Heritage

- Human Rights & Governance

- Disaster Relief & Humanitarian Aid

- Scientific Research & Innovation

By Distribution Model

- Direct Grant-Making

- Intermediary-Based Allocation

- Outcome-Based / Impact-Linked Funding

- Blended Finance Models

- Crowdfunded Philanthropy Pools

Regional Insights

North America

North America leads the global philanthropy fund market with approximately 45% share in 2025, with the United States alone contributing nearly 40% of global market value. The region’s dominance is driven by a highly mature philanthropic ecosystem, strong presence of large private foundations, and widespread adoption of donor-advised funds. Favorable tax policies, such as deductions for charitable contributions, significantly incentivize structured giving. Additionally, high concentration of UHNWIs, advanced financial infrastructure, and strong culture of institutional philanthropy further accelerate regional growth. The increasing focus on impact investing and ESG-aligned funding is also strengthening market expansion in this region.

Europe

Europe accounts for around 25% of the global market, led by countries such as the UK, Germany, and the Netherlands. Growth in the region is driven by strong institutional frameworks, government-supported social welfare systems, and increasing emphasis on sustainability and climate action. European donors are highly aligned with ESG principles, leading to increased adoption of impact-driven philanthropy. Regulatory support for non-profit organizations, along with cross-border collaboration within the European Union, further facilitates fund flows. Additionally, rising interest among younger donors in ethical and transparent giving is contributing to steady market growth.

Asia-Pacific

Asia-Pacific is the fastest-growing region, expanding at over 9% CAGR, with China and India as key growth engines. The region’s growth is driven by rapid wealth creation, an increasing number of high-net-worth individuals, and supportive government policies promoting structured philanthropy. In India, mandatory CSR regulations are a major driver, channeling billions of dollars annually into organized funds. China’s policy initiatives aimed at promoting “common prosperity” are also encouraging large-scale philanthropic contributions. Additionally, rising digital adoption is enabling new forms of giving through online platforms, further accelerating market penetration.

Latin America

Latin America holds approximately 7% market share, with Brazil and Mexico as leading contributors. Regional growth is driven by increasing corporate participation in philanthropy, rising social development needs, and growing awareness of structured giving mechanisms. However, regulatory complexity and economic volatility remain challenges. Despite these constraints, the expansion of community foundations and international funding partnerships is supporting gradual market development. The region is also witnessing increased focus on education and poverty alleviation initiatives, driving demand for philanthropic funds.

Middle East & Africa

The Middle East & Africa region accounts for nearly 8% of the global market. Growth in the Middle East is driven by strong cultural and religious traditions of giving, particularly through institutionalized charitable structures in countries such as the UAE and Saudi Arabia. High-income populations and the increasing establishment of formal philanthropic organizations are further supporting market expansion. In Africa, the region acts as a major recipient of global philanthropic funds, particularly in healthcare, education, and humanitarian aid. International donor funding, combined with increasing local philanthropic initiatives, is driving growth, although regulatory and infrastructure challenges remain key considerations.

Key Players in the Philanthropy Fund Market

- Bill & Melinda Gates Foundation

- Wellcome Trust

- Ford Foundation

- Lilly Endowment

- Silicon Valley Community Foundation

- Open Society Foundations

- Rockefeller Foundation

- MacArthur Foundation

- Novo Nordisk Foundation

- Gordon and Betty Moore Foundation

- Chan Zuckerberg Initiative

- Kuwait Foundation for the Advancement of Sciences

- Tata Trusts

- Azim Premji Foundation

- King Baudouin Foundation