Pet Skin Care Products Market Size

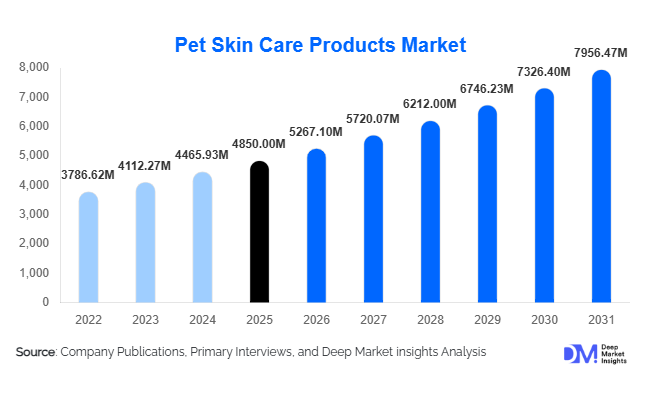

According to Deep Market Insights, the global pet skin care products market size was valued at USD 4,850 million in 2025 and is projected to grow from USD 5,267.10 million in 2026 to reach USD 7,956.47 million by 2031, expanding at a CAGR of 8.6% during the forecast period (2026–2031). The market growth is primarily driven by increasing pet ownership, rising awareness of pet dermatological health, and the growing trend of pet humanization, where pets are treated as family members. Additionally, the rising incidence of skin-related issues such as allergies, infections, and dermatitis is fueling demand for medicated and specialized skin care products globally.

Key Market Insights

- Natural and organic formulations are gaining strong traction, driven by consumer preference for chemical-free and safe products for pets.

- Dogs dominate the market, accounting for the largest share due to higher ownership and grooming needs.

- North America leads the global market, supported by high pet care spending and advanced veterinary infrastructure.

- Asia-Pacific is the fastest-growing region, driven by rising disposable income and increasing pet adoption in China and India.

- E-commerce channels are rapidly expanding, offering convenience, competitive pricing, and wider product availability.

- Veterinary dermatology innovations are enhancing product effectiveness and expanding prescription-based solutions.

What are the latest trends in the pet skin care products market?

Shift Toward Natural & Organic Products

Consumers are increasingly opting for natural and organic pet skin care products that avoid harsh chemicals such as parabens, sulfates, and synthetic fragrances. This trend mirrors the human skincare industry, where clean-label products are gaining widespread popularity. Manufacturers are incorporating plant-based ingredients such as aloe vera, oatmeal, and essential oils, positioning their offerings as safe and eco-friendly. Additionally, sustainable packaging and cruelty-free certifications are becoming important differentiators in the market.

Growth of Premium and Medicated Product Lines

The demand for premium and medicated skin care products is rising significantly, particularly for treating specific dermatological conditions such as fungal infections, allergies, and bacterial skin issues. Companies are investing in research and development to create veterinary-approved formulations that deliver targeted results. This trend is driving higher average selling prices and improving profit margins, especially in developed markets where pet owners are willing to spend more on advanced care solutions.

What are the key drivers in the pet skin care products market?

Increasing Pet Ownership and Humanization

The surge in global pet ownership, particularly post-pandemic, has been a major driver for the market. Pets are increasingly considered family members, leading to higher spending on grooming and healthcare products. This shift in consumer behavior is significantly boosting demand for specialized skin care solutions.

Rising Prevalence of Skin Disorders in Pets

Skin-related conditions such as dermatitis, allergies, and infections are among the most common health issues in pets. Environmental factors, dietary changes, and genetic predispositions are contributing to this rise, increasing the demand for medicated and therapeutic products.

Expansion of E-commerce Platforms

The growth of online retail has improved product accessibility and consumer awareness. E-commerce platforms enable easy comparison of products, reviews, and pricing, encouraging higher adoption rates and expanding the market reach globally.

What are the restraints for the global market?

High Cost of Premium Products

Premium and specialized pet skin care products often come at a higher price point, limiting their adoption in price-sensitive markets. This remains a key challenge, particularly in developing economies.

Limited Awareness in Emerging Markets

Despite increasing pet ownership, awareness regarding pet dermatological health remains relatively low in several regions. This leads to underutilization of advanced skin care products and reliance on basic grooming solutions.

What are the key opportunities in the pet skin care products industry?

Expansion in Emerging Markets

Rapid urbanization and rising disposable incomes in countries such as China, India, and Brazil present significant growth opportunities. Increasing pet adoption in these regions is driving demand for grooming and healthcare products, creating a favorable environment for market expansion.

Integration with Veterinary Dermatology

Advancements in veterinary dermatology and the development of prescription-based skin care products offer strong growth potential. Collaborations between pet care companies and veterinary clinics are enabling the creation of targeted treatment solutions, enhancing product effectiveness and market value.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4850 Million |

| Market Size in 2026 | USD 5267.10 Million |

| Market Size in 2031 | USD 7956.47 Million |

| CAGR | 8.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Shampoos and conditioners dominate the pet skin care products market, accounting for approximately 32% of the total market share in 2025. Their leadership position is primarily driven by their essential role in routine grooming and hygiene maintenance, making them a high-frequency purchase category among pet owners. The recurring nature of usage, often weekly or bi-weekly, ensures stable and consistent demand across both developed and emerging markets. Within this segment, medicated shampoos are witnessing accelerated growth due to the increasing prevalence of dermatological conditions such as fungal infections, dermatitis, and allergies. These products are often recommended by veterinarians, further strengthening their adoption.

Additionally, the rise in premiumization has led to the introduction of specialized variants such as hypoallergenic, anti-itch, and organic shampoos, catering to evolving consumer preferences. Other product categories, including sprays, creams, ointments, and wipes, are also gaining traction due to their targeted application benefits and convenience. For instance, sprays and wipes are increasingly used for quick cleaning and localized treatment, especially among urban pet owners seeking time-efficient solutions. This diversification of product offerings is expanding the overall market scope while reinforcing the dominance of shampoos and conditioners.

Application Insights

Grooming and hygiene maintenance represent the largest application segment, holding around 28% of the market share in 2025. This segment leads primarily due to its recurring demand cycle, as pet owners are increasingly adopting regular grooming routines to maintain pet health and cleanliness. The growing trend of pet humanization has significantly contributed to this shift, with owners investing in high-quality grooming products similar to human personal care items.

Moreover, the expansion of professional grooming services and DIY grooming practices has further strengthened this segment. Allergy management and infection treatment are also key application areas, driven by the rising incidence of skin-related conditions caused by environmental factors, dietary sensitivities, and parasitic infections. These segments are benefiting from increased veterinary consultations and awareness campaigns regarding pet health. Additionally, the demand for parasite control products is growing steadily, supported by preventive healthcare practices and rising awareness about flea and tick infestations, particularly in warmer climates. The convergence of preventive and therapeutic applications is expected to sustain long-term growth across all application segments.

Distribution Channel Insights

E-commerce platforms account for approximately 26% of the market share, making them one of the fastest-growing distribution channels in the pet skin care products market. The rapid growth of this segment is driven by the increasing penetration of digital platforms, the convenience of home delivery, and access to a wide variety of products across price ranges and brands. Consumers benefit from detailed product descriptions, reviews, and competitive pricing, enabling informed purchasing decisions.

The COVID-19 pandemic further accelerated the shift toward online purchasing, a trend that continues to persist. Subscription-based models and direct-to-consumer (D2C) strategies are also gaining popularity, ensuring repeat purchases and customer retention. Despite the growth of e-commerce, veterinary clinics and pet specialty stores remain critical channels, particularly for medicated and prescription-based products. These offline channels provide expert guidance, product authenticity assurance, and personalized recommendations, which are crucial for treating specific skin conditions. The coexistence of online and offline channels is creating an omnichannel ecosystem that enhances overall market accessibility.

Pet Type Insights

Dogs dominate the pet skin care products market, contributing nearly 58% of the total market share in 2025. This dominance is primarily attributed to their higher global ownership rates and greater grooming requirements compared to other pets. Dogs are more prone to skin conditions due to factors such as outdoor exposure, breed-specific sensitivities, and higher interaction with environmental allergens, which drives consistent demand for skin care products.

Cats represent the second-largest segment, supported by increasing urban adoption and growing awareness of feline health needs. While cats generally require less frequent grooming than dogs, the demand for specialized products such as hypoallergenic shampoos and anti-parasitic treatments is rising. Small mammals and exotic pets, including rabbits, guinea pigs, birds, and reptiles, account for a smaller share of the market. However, these segments are gradually gaining attention as niche markets, with manufacturers introducing tailored products to address their unique dermatological requirements. This diversification across pet types is expected to contribute to incremental market growth.

Explore more data points, trends and opportunities Download Free Sample Report

Pet Skin Care Products Market Segmentations

By Product Type

- Shampoos & Conditioners

- Sprays & Mists

- Creams & Ointments

- Wipes & Cleansing Pads

- Oils & Serums

- Medicated Treatments

By Application

- Grooming & Hygiene Maintenance

- Infection Treatment

- Allergy Management

- Parasite Control

- Wound Care & Healing

- Skin Hydration & Conditioning

By Distribution Channel

- E-commerce Platforms

- Veterinary Clinics

- Pet Specialty Stores

- Supermarkets/Hypermarkets

- Pharmacies

By Pet Type

- Dogs

- Cats

- Small Mammals

- Exotic Pets

Regional Insights

North America

North America holds the largest share of the global market, accounting for approximately 38% in 2025. The United States dominates the region due to its high pet ownership rates, advanced veterinary healthcare infrastructure, and strong consumer spending on pet care. One of the primary drivers of regional growth is the increasing trend of premiumization, with pet owners willing to invest in high-quality, organic, and veterinarian-recommended products. Additionally, the presence of major market players, strong distribution networks, and widespread adoption of pet insurance are further supporting market expansion. The region also benefits from high awareness levels regarding pet dermatological health, driving demand for specialized and medicated products.

Europe

Europe accounts for approximately 27% of the market share, with key countries such as Germany, the United Kingdom, and France driving demand. The region’s growth is driven by stringent regulatory standards related to pet care product safety and a strong consumer preference for natural and sustainable formulations. European consumers are highly conscious of product ingredients, leading to increased adoption of organic and eco-friendly skin care products. Additionally, the rising trend of pet humanization and increasing expenditure on premium pet care products are key growth drivers. Government regulations promoting animal welfare and product transparency further enhance consumer trust and support steady market growth across the region.

Asia-Pacific

Asia-Pacific is the fastest-growing region, with a projected CAGR of over 10%. China and India are the primary growth engines, driven by rapid urbanization, rising disposable incomes, and increasing pet adoption among younger populations. The growing middle class and changing lifestyles are encouraging higher spending on pet grooming and healthcare products. Additionally, the expansion of e-commerce platforms and improving veterinary infrastructure are facilitating market penetration. Japan contributes significantly with its demand for premium and technologically advanced products, while Southeast Asian countries are emerging as high-potential markets due to increasing awareness and retail expansion. The region’s growth is further supported by a shift toward Western pet care practices and increased availability of international brands.

Latin America

Latin America is witnessing steady growth, particularly in Brazil and Mexico, which are the largest markets in the region. The primary drivers of growth include increasing pet ownership, rising awareness of pet health and hygiene, and the gradual expansion of organized retail and e-commerce channels. Economic development and urbanization are also contributing to higher disposable incomes, enabling consumers to spend more on pet care products. Additionally, the growing presence of international brands and improved distribution networks are enhancing product accessibility. Preventive healthcare awareness, particularly related to parasite control, is further driving demand for skin care products in the region.

Middle East & Africa

The Middle East and Africa region is experiencing moderate growth, with countries such as the UAE and South Africa leading demand. Growth in this region is primarily driven by rising pet ownership among urban populations and increasing adoption of premium pet care products. In the Middle East, high disposable incomes and a strong preference for luxury products are driving demand for premium and imported skincare solutions. Meanwhile, South Africa serves as a key market in Africa, benefiting from a relatively developed pet care industry and increasing awareness of pet health. However, challenges such as limited awareness in certain areas and fragmented distribution networks may restrain growth. Despite these challenges, ongoing improvements in retail infrastructure and veterinary services are expected to support long-term market expansion.

Key Players in the Pet Skin Care Products Market

- Mars Petcare

- Nestlé Purina PetCare

- Zoetis Inc.

- Elanco Animal Health

- Virbac

- Beaphar

- PetIQ

- Himalaya Wellness (Animal Health Division)

- Vet’s Best

- TropiClean

- SynergyLabs

- Dechra Pharmaceuticals

- Boehringer Ingelheim Animal Health

- Bayer Animal Health

- Ceva Santé Animale