Personalized Nutrition Market Size

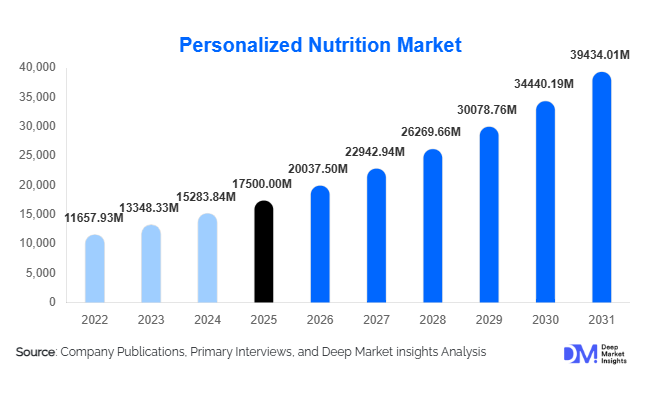

According to Deep Market Insights, the global personalized nutrition market size was valued at USD 17,500 million in 2025 and is projected to grow from USD 20,037.50 million in 2026 to reach USD 39,434.01 million by 2031, expanding at a CAGR of 14.5% during the forecast period (2026–2031). The market growth is primarily driven by increasing adoption of preventive healthcare, rising consumer demand for data-driven dietary guidance, and technological advancements in genomics, microbiome profiling, and AI-powered personalized nutrition platforms.

Key Market Insights

- Digital health integration is transforming personalized nutrition, enabling real-time dietary recommendations through apps, wearable devices, and AI analytics.

- Genetic testing and nutrigenomics dominate technology adoption, offering insights into individual nutrient requirements and risk factors for chronic diseases.

- North America holds the largest market share, driven by high health awareness, strong digital infrastructure, and early adoption of genomic and nutrition-based technologies.

- Europe is the second-largest market and emphasizes preventive health, with Germany, the UK, and Nordic countries leading the adoption of clinical and lifestyle-focused personalized nutrition solutions.

- Asia-Pacific is the fastest-growing region, fueled by rising disposable incomes, urbanization, and increasing awareness of lifestyle diseases in China, India, and Japan.

- Subscription-based digital platforms and online retail channels are shaping consumer engagement, offering scalability, recurring revenue, and ease of access for individual users.

What are the latest trends in the personalized nutrition market?

Integration of Multi-Omics and AI Analytics

Companies are increasingly combining genomics, metabolomics, and microbiome data to create precise nutrition recommendations. AI-driven analytics processes large datasets to identify individual nutritional needs, enabling hyper-personalized diet plans and supplement recommendations. This multi-omics approach is gaining traction in both clinical and consumer markets, offering predictive insights for disease prevention, weight management, and fitness optimization. Platforms that integrate wearable devices with continuous health monitoring are providing real-time feedback, enhancing adherence and user engagement.

Expansion of Digital Advisory Services

Digital subscription platforms and app-based advisory services are redefining accessibility in personalized nutrition. Users can now receive real-time insights based on their genetic, metabolic, and lifestyle data. Telehealth integration allows dietitians and nutritionists to offer remote consultations, expanding reach beyond urban centers. The trend appeals to younger, tech-savvy consumers and increases recurring engagement through gamified health tracking, reminders, and tailored supplement recommendations.

What are the key drivers in the personalized nutrition market?

Rising Prevalence of Chronic and Lifestyle Diseases

The global increase in obesity, diabetes, cardiovascular diseases, and metabolic disorders is driving demand for preventive nutrition solutions. Personalized nutrition helps individuals manage risk factors and adopt sustainable lifestyle changes, offering better outcomes than generic dietary advice. Health-conscious adults and aging populations are actively seeking solutions that can be tailored to their biological and genetic profiles.

Technological Advancements in Testing and Analytics

Next-generation sequencing, microbiome profiling, and AI-powered dietary modeling have made personalized nutrition more accurate and actionable. Wearable devices and health monitoring apps provide continuous data streams that inform dynamic nutritional guidance. These innovations not only enhance precision but also build consumer trust in personalized dietary interventions.

Increased Consumer Awareness and Digital Health Adoption

Growing knowledge about nutrition, genomics, and preventive health, combined with high smartphone penetration, is supporting market adoption. Consumers are increasingly willing to pay for services that promise measurable health benefits, fueling growth in subscription-based digital nutrition services and at-home testing kits.

What are the restraints for the global market?

Data Privacy and Regulatory Challenges

Personalized nutrition relies on sensitive health and genomic data, making compliance with privacy regulations critical. Regional disparities in data governance and consumer apprehension around data usage may slow adoption. Companies must invest in secure platforms and clear consent mechanisms to mitigate these challenges.

High Cost of Advanced Testing and Services

Genetic and microbiome testing, along with AI-driven analytics, remains expensive. High costs limit access for price-sensitive consumers, particularly in emerging markets. Until testing becomes more affordable and mainstream, growth may be constrained.

What are the key opportunities in the personalized nutrition industry?

Integration with Digital Health Ecosystems

The expansion of telehealth and wearable devices presents an opportunity to integrate personalized nutrition into holistic digital health platforms. Real-time health monitoring, AI-driven diet adjustments, and remote consultations create a seamless user experience, encouraging long-term engagement and higher retention rates.

Government Support and Preventive Healthcare Policies

Regulatory frameworks emphasizing preventive health and personalized interventions provide a favorable environment. Programs promoting genomic testing, dietary monitoring, and chronic disease prevention open revenue streams for service providers and encourage consumer adoption, particularly in developed markets.

Emerging Markets Demand Growth

Asia-Pacific and Latin America are witnessing rapid growth in personalized nutrition due to increasing urbanization, middle-class expansion, and rising lifestyle disease awareness. Customized nutrition offerings tailored to cultural preferences and dietary habits in these regions provide substantial growth potential for both startups and established players.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 17500 Million |

| Market Size in 2026 | USD 20037.50 Million |

| Market Size in 2031 | USD 39434.01 Million |

| CAGR | 14.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Customized dietary supplements dominate the product segment, accounting for approximately 32% of the 2025 market share. Their strong performance is primarily driven by ease of adoption, cost-effectiveness compared to genetic or microbiome testing, and the growing consumer focus on targeted nutrient interventions. Consumers increasingly prefer supplements tailored to specific health goals such as immunity support, metabolic health, and chronic disease management. Functional foods and beverages, as well as nutrigenomics products, are gaining momentum, reflecting rising awareness of precision nutrition and interest in preventive healthcare solutions. The leading segment driver in this category is the combination of personalized health insights and affordability, which allows a wider demographic to adopt personalized nutrition practices without the need for complex testing.

Application Insights

The individual consumer segment represents the largest share at 50% of the overall market demand. These consumers are focused on preventive health, weight management, fitness optimization, and mitigating chronic disease risks. Healthcare providers and dietitians are increasingly adopting personalized nutrition solutions to enhance patient outcomes, particularly in clinical settings managing metabolic disorders and cardiovascular diseases. Fitness and wellness centers leverage genomic, microbiome, and metabolic data to optimize athlete training, recovery, and performance. Additionally, cross-border adoption is growing, with export-driven demand from North America and Europe reaching emerging markets in APAC and LATAM. This trend highlights the global scalability of personalized nutrition solutions and underscores the role of technology-enabled platforms in expanding access across geographies.

Distribution Channel Insights

Online direct-to-consumer (D2C) channels hold the largest share, approximately 40%, due to their convenience, broader product access, and seamless integration with digital health applications. These channels enable real-time tracking of dietary recommendations, personalized supplement subscriptions, and interactive health dashboards. Pharmacies, clinics, and corporate wellness programs are also important adoption avenues, particularly for clinical and workplace nutrition initiatives. Subscription-based platforms and app-driven guidance are emerging as critical tools for customer engagement, fostering recurring revenue models and strengthening loyalty. The growth driver for distribution is the rising consumer preference for convenience, technology-enabled personalization, and seamless access to health insights.

Age Group Insights

Adults aged 18–64 account for the largest portion of market demand, approximately 45%, driven by disposable income, proactive health management, and a high inclination toward digital health solutions. Seniors (65+) are increasingly adopting personalized nutrition to manage chronic conditions and enhance quality of life. Adolescents and children are emerging as a growth segment, especially for wellness-focused interventions and school-based nutrition programs designed to improve long-term health outcomes. The key driver across age groups is health awareness combined with technology-enabled access to personalized recommendations.

Explore more data points, trends and opportunities Download Free Sample Report

Personalized Nutrition Market Segmentations

By Product Type

- Customized Dietary Supplements

- Functional Foods & Beverages

- Nutrigenomics Products

- Microbiome-Based Nutrition Products

- Nutrient Profiling & Diagnostic Kits

By Application / End-Use

- Individual Consumers

- Healthcare Providers & Dietitians

- Fitness & Wellness Centers

- Research & Clinical Labs

By Distribution Channel

- Online Retail / Direct-to-Consumer

- Pharmacies & Health Stores

- Clinics & Health Centers

- Corporate Wellness Programs

By Target Demographic

- Adults (18–64)

- Seniors (65+)

- Adolescents (13–17)

- Children (<13)

- Athletes & Fitness Enthusiasts

Regional Insights

North America

North America holds the largest market share at approximately 38%, driven by early adoption of preventive health solutions, high disposable incomes, and strong digital health infrastructure. The U.S. leads the market, followed by Canada, with growth fueled by widespread use of subscription-based nutrition platforms, at-home testing kits, and app-based dietary guidance. Key growth drivers include increasing prevalence of lifestyle diseases, strong consumer awareness of genomics and nutrigenomics, and well-established healthcare systems supporting preventive nutrition programs. Companies are leveraging AI-driven platforms and telehealth integration to further expand market penetration in urban and suburban populations.

Europe

Europe represents approximately 30% of the market, with Germany, the UK, and Nordic countries leading adoption. Growth is supported by government initiatives promoting preventive healthcare, rising awareness of lifestyle-related diseases, and integration of personalized nutrition into clinical services. Subscription platforms, nutrigenomic testing, and digital advisory services are widely adopted. Regional growth drivers include high consumer trust in health technologies, insurance reimbursement for nutrition programs in certain countries, and strong investments in digital health ecosystems that support personalized interventions.

Asia-Pacific

Asia-Pacific is the fastest-growing region, led by China, India, and Japan. Rising disposable incomes, urbanization, changing dietary habits, and increasing health awareness are major drivers. Online retail platforms and digital advisory services are critical growth enablers, providing convenient access to supplements and personalized diet plans. Government health initiatives promoting preventive care, growing smartphone penetration, and the adoption of AI-based dietary platforms are further fueling growth. The regional rise in lifestyle-related diseases, coupled with expanding middle-class wellness spending, continues to accelerate market expansion.

Latin America

Brazil and Mexico are key contributors to the market, with growth driven by rising wellness awareness, increased adoption of digital nutrition platforms, and demand for targeted dietary interventions among the urban middle class. Regional growth is supported by improving healthcare infrastructure, government health campaigns, and increasing availability of online subscription services. Consumers are showing greater willingness to invest in preventive nutrition and health optimization, particularly in metropolitan areas, which is driving segment expansion.

Middle East & Africa

The Middle East, led by the UAE, Saudi Arabia, and Qatar, is witnessing growing adoption of personalized nutrition solutions due to high disposable incomes, wellness-oriented lifestyles, and increasing prevalence of chronic lifestyle diseases. Africa is emerging as a niche market with potential in telehealth-driven personalized nutrition for urban centers. Key growth drivers include the expansion of digital health infrastructure, rising health awareness, and government-led preventive health initiatives targeting lifestyle disease management. Investment in e-health platforms and technology-driven dietary services is enhancing market accessibility across the region.

Key Players in the Personalized Nutrition Market

- Nestlé S.A.

- Danone S.A.

- Abbott Laboratories

- PepsiCo, Inc.

- DSM (Royal DSM)

- Amway Corporation

- Herbalife Nutrition Ltd.

- Viome, Inc.

- Baze Technologies

- Habit, Inc.

- Lifesum AB

- InsideTracker

- Nutrigenomix

- 23andMe, Inc.

- Nutraceutical Wellness, Inc.