Personal Safety Alarm for Women Market Size

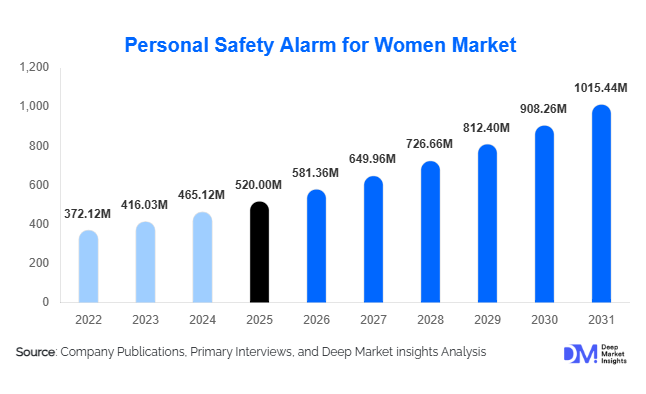

According to Deep Market Insights, the global personal safety alarm market for women was valued at USD 520 million in 2025 and is projected to grow from USD 581.36 million in 2026 to reach USD 1,015.44 million by 2031, expanding at a CAGR of 11.8% during the forecast period (2026–2031). The market growth is primarily driven by rising safety concerns among women, increasing urban crime rates, and growing adoption of compact, wearable personal security devices. Technological advancements, including GPS-enabled alarms, smartphone integration, and AI-powered alert systems, are further accelerating adoption across both developed and emerging economies.

Key Market Insights

- Growing awareness around women’s safety is significantly boosting demand, particularly in urban regions and high-density cities.

- Wearable and discreet safety devices are gaining popularity, including smart jewelry and wristband-based alarms.

- North America dominates the market, driven by high consumer awareness and strong retail penetration.

- Asia-Pacific is the fastest-growing region, supported by government initiatives and rising disposable incomes.

- E-commerce platforms are transforming distribution, enabling global accessibility and competitive pricing.

- Integration with mobile apps and IoT ecosystems is reshaping product innovation and user engagement.

What are the latest trends in the personal safety alarm for women market?

Shift Toward Smart and Connected Safety Devices

The market is undergoing a significant shift from traditional sound-based alarms to smart, connected devices. Modern personal safety alarms now integrate with smartphones, enabling features such as real-time location sharing, emergency contact alerts, and automated SOS notifications. Bluetooth and GPS-enabled alarms are becoming increasingly popular, especially among younger consumers who prioritize connectivity and convenience. Companies are also developing app-based ecosystems that allow users to monitor safety metrics and access emergency services instantly, thereby enhancing the overall value proposition of these devices.

Rising Demand for Wearable and Fashionable Safety Solutions

Consumers are increasingly seeking safety devices that are both functional and aesthetically appealing. This has led to the emergence of wearable safety alarms embedded in jewelry, keychains, and wristbands. These products are designed to blend seamlessly into everyday fashion, encouraging consistent usage. Brands are focusing on compact, lightweight designs with customizable features to cater to diverse consumer preferences. This trend is particularly prominent among urban women and younger demographics, who value discreet yet effective safety solutions.

What are the key drivers in the personal safety alarm for women market?

Increasing Urban Safety Concerns

The rise in urban crime rates and incidents of harassment has heightened the need for personal safety solutions. Women, particularly in metropolitan areas, are adopting personal alarms as a preventive safety measure. Governments and advocacy groups are also promoting awareness campaigns, further driving market growth.

Growth in Wearable Technology Adoption

The increasing adoption of wearable devices has positively influenced the personal safety alarm market. Consumers are more inclined to use safety devices that integrate seamlessly with their daily lifestyle. Smart wearables with safety features are gaining traction, especially in developed markets where technology adoption is high.

What are the restraints for the global market?

Product Commoditization and Price Competition

The availability of low-cost, similar-functionality products has led to intense price competition. Many basic alarm devices offer limited differentiation, which restricts pricing power and impacts profit margins for manufacturers.

Limited Awareness in Emerging Rural Markets

Despite growing adoption in urban areas, awareness of personal safety alarms remains relatively low in rural and semi-urban regions. Lack of education and limited access to distribution channels hinder market penetration in these areas.

What are the key opportunities in the personal safety alarm for women industry?

Integration with IoT and Smart Ecosystems

The integration of personal safety alarms with IoT ecosystems presents significant growth opportunities. Devices that connect with smartphones, smartwatches, and home security systems can provide enhanced functionality, including predictive alerts and automated emergency responses. This opens avenues for subscription-based services and recurring revenue streams for manufacturers.

Government and Institutional Safety Programs

Governments across various regions are launching initiatives to enhance women’s safety, creating opportunities for bulk procurement of personal safety devices. Educational institutions and corporate organizations are also adopting these devices as part of safety programs, offering a scalable growth avenue for market participants.

Product Type Insights

Keychain alarms continue to dominate the global personal safety alarm for women market, accounting for approximately 38% of the global market share in 2025. The leadership of this segment is primarily driven by its affordability, compact design, and ease of use, making it highly accessible to a broad consumer base across both developed and emerging markets. These devices require minimal technical knowledge and offer instant activation, which enhances their appeal for first-time users and mass adoption. Additionally, their wide availability across online and offline channels further strengthens their market position. Wearable alarms, including smart jewelry such as pendants, rings, and wristbands, are rapidly gaining traction as consumers increasingly seek discreet and aesthetically appealing safety solutions. This segment is being driven by the convergence of fashion and functionality, particularly among younger demographics and urban consumers. The ability to integrate these devices seamlessly into daily lifestyles without drawing attention is a key adoption factor.

Multi-function safety devices that combine alarms with additional features such as GPS tracking, LED flashlights, and mobile connectivity are emerging as a premium segment. These products are particularly popular among tech-savvy users and in developed markets, where demand for advanced, feature-rich solutions is growing. The shift toward multifunctionality reflects a broader trend of integrating personal safety devices into the connected ecosystem.

Technology Insights

Basic sound-based alarms hold the largest share in the market at around 42% in 2025, primarily due to their cost-effectiveness, reliability, and independence from external connectivity. These devices, typically emitting sound levels above 120 dB, provide immediate deterrence and are widely adopted in price-sensitive markets. Their simplicity ensures compatibility without reliance on battery-intensive features such as GPS or Bluetooth, making them particularly suitable for mass-market deployment. However, GPS-enabled and Bluetooth-connected devices are witnessing significantly faster growth rates. This growth is being driven by increasing smartphone penetration, rising consumer awareness of connected safety solutions, and the need for real-time location tracking in emergencies. These technologies allow users to instantly alert predefined contacts and share their location, enhancing response time and overall safety outcomes.

AI-integrated alarms represent the next phase of technological evolution in this market. These advanced systems are expected to gain traction in the coming years, offering features such as predictive threat detection, automated emergency alerts, and behavioral pattern analysis. As digital ecosystems continue to expand, the integration of artificial intelligence and IoT capabilities is likely to redefine the competitive landscape.

Distribution Channel Insights

Online retail remains the dominant distribution channel, accounting for approximately 55% of the market share in 2025. The growth of this segment is driven by the increasing penetration of e-commerce platforms, ease of product comparison, and the availability of a wide range of options across price points. Consumers benefit from detailed product descriptions, reviews, and competitive pricing, which significantly influence purchasing decisions. Additionally, the rise of social media marketing and influencer-driven promotions has further accelerated online sales.

Offline channels, including supermarkets, hypermarkets, electronics retailers, and specialty safety stores, continue to play a vital role, particularly in regions with lower digital adoption or where consumers prefer in-person product evaluation. These channels also contribute to impulse purchases and brand visibility through physical displays. Brand-owned websites and direct-to-consumer (D2C) strategies are gaining importance as manufacturers seek to build stronger relationships with customers, improve margins, and offer customized product experiences. Subscription-based safety services and bundled offerings are also emerging within this channel, further enhancing customer engagement.

End-Use Insights

Individual consumers represent the largest end-use segment, accounting for nearly 62% of the market in 2025. This dominance is driven by increasing personal safety awareness, especially among women in urban areas, and the growing perception of personal alarms as essential everyday accessories. The affordability and accessibility of these devices have further supported widespread adoption at the individual level.

Institutional adoption is emerging as a significant growth driver, particularly across educational institutions and corporate organizations. Schools and universities are increasingly distributing personal safety alarms to students as part of campus safety initiatives, while corporations are integrating these devices into employee safety programs, especially for women working in late shifts or remote locations. Government-led initiatives are also contributing to rising demand, with several countries implementing programs aimed at enhancing women’s safety through the distribution of personal security devices. These large-scale deployments not only drive volume growth but also increase overall market awareness and acceptance.

| By Product Type | By Technology | By Distribution Channel | By End User |

|---|---|---|---|

|

|

|

|

Regional Insights

North America

North America holds the largest market share at approximately 34% in 2025, led by the United States. The region’s dominance is driven by high consumer awareness regarding personal safety, strong purchasing power, and early adoption of advanced technologies. The presence of established manufacturers and a well-developed e-commerce ecosystem further supports market growth. Additionally, increasing participation from educational institutions and corporate safety programs is boosting demand. Rising concerns around personal security in urban areas and strong advocacy for women’s safety continue to act as key growth drivers in this region.

Europe

Europe accounts for around 26% of the global market, with countries such as the UK, Germany, and France leading adoption. Growth in this region is primarily driven by stringent safety regulations, high urban population density, and increasing government focus on public safety initiatives. European consumers also show a strong preference for sustainable and wearable safety solutions, encouraging innovation in eco-friendly and aesthetically designed products. Additionally, widespread awareness campaigns and the integration of safety devices into public transport systems are contributing to steady market expansion.

Asia-Pacific

Asia-Pacific is the fastest-growing region, with a CAGR of approximately 14%. Key markets such as China, India, and Japan are driving growth due to rising awareness of women’s safety, increasing disposable incomes, and rapid urbanization. Government initiatives and public safety campaigns, particularly in India, are significantly boosting adoption. The expansion of e-commerce platforms and the availability of low-cost devices are further enhancing accessibility. Additionally, the large population base and increasing smartphone penetration create a strong foundation for the growth of connected safety devices in this region.

Latin America

Latin America is experiencing steady growth, with Brazil and Mexico leading demand. The market in this region is primarily driven by high crime rates and growing concerns around personal safety, particularly in urban centers. Increasing awareness campaigns and the gradual expansion of online retail channels are supporting adoption. Economic improvements and rising middle-class populations are also contributing to higher spending on personal safety products. However, price sensitivity remains a key factor influencing purchasing decisions.

Middle East & Africa

The Middle East & Africa region is witnessing moderate growth, supported by rapid urbanization, rising security concerns, and increasing awareness of personal safety solutions. Key markets such as the UAE and South Africa are leading adoption due to higher income levels and better access to advanced technologies. Government initiatives aimed at improving public safety, along with growing investments in smart city infrastructure, are acting as key growth drivers. Additionally, increasing the participation of women in the workforce is contributing to higher demand for personal safety devices across urban areas.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|