Perfume Market Size

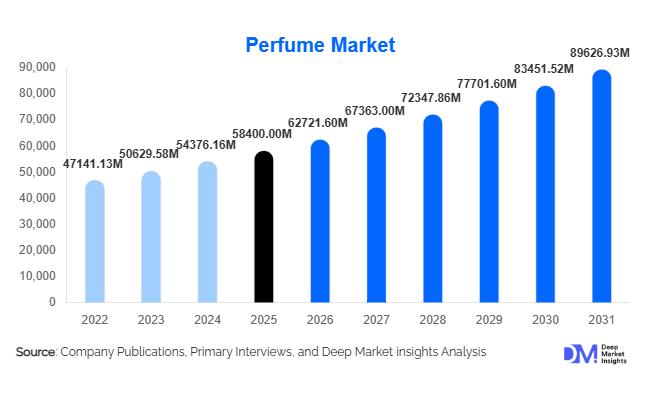

According to Deep Market Insights, the global perfume market size was valued at USD 58,400 million in 2025 and is projected to grow from USD 62,721.60 million in 2026 to reach USD 89,626.93 million by 2031, expanding at a CAGR of 7.4% during the forecast period (2026–2031). The market growth is driven by rising disposable incomes, increasing demand for premium and luxury fragrances, expansion of e-commerce distribution channels, and growing consumer preference for personalized and long-lasting scent formulations. The shift toward sustainable, clean-label ingredients and the rapid rise of niche and artisanal perfume brands are further reshaping the competitive landscape.

The global perfume market is experiencing strong structural transformation as consumer behavior shifts toward experiential luxury and identity-driven consumption. In 2025, fragrance products are no longer limited to traditional personal care but are increasingly positioned as lifestyle and fashion statements. Premiumization is a key trend, with consumers willing to pay higher prices for exclusivity, brand heritage, and long-lasting performance. Additionally, gender-neutral fragrances are expanding the consumer base, particularly among millennials and Gen Z. Emerging markets in Asia-Pacific and the Middle East are witnessing rapid growth due to increasing urbanization, rising middle-class income, and stronger exposure to global luxury brands. Meanwhile, digital transformation is reshaping the retail landscape, with online fragrance sales gaining momentum through AI-based recommendations, virtual sampling, and influencer-led marketing strategies. Overall, the perfume industry is positioned for sustained growth, supported by innovation in formulation, packaging sustainability, and omnichannel distribution expansion.

Key Market Insights

- Premiumization trend dominates global demand, with luxury perfumes accounting for a significant share of revenue across developed markets.

- Gender-neutral fragrances are expanding rapidly, driven by shifting consumer identity preferences and inclusive branding strategies.

- Europe leads in heritage luxury perfume production, while Asia-Pacific shows the fastest consumption growth.

- E-commerce is becoming a critical sales channel, contributing nearly one-third of global perfume distribution.

- Sustainable and clean-label formulations are gaining traction, particularly in Europe and North America due to regulatory and consumer pressure.

- Influencer marketing and celebrity endorsements continue to strongly influence purchasing behavior across all major regions.

Perfume Market Trends

Rise of Niche and Artisanal Fragrances

Consumers are increasingly shifting toward niche perfume brands that offer unique scent profiles, exclusivity, and storytelling-driven branding. These products often use rare ingredients and limited production runs, enabling higher margins and stronger brand loyalty. This trend is particularly strong in Europe and North America, where luxury consumers prioritize individuality over mass-market fragrances.

Clean Beauty and Sustainable Fragrance Innovation

Sustainability is becoming a central pillar in perfume manufacturing. Brands are adopting biodegradable ingredients, recyclable packaging, and cruelty-free formulations. Regulatory pressure in Europe and consumer awareness globally are accelerating the adoption of clean-label perfumes. Companies investing in green chemistry and ethical sourcing are gaining competitive advantage.

Digital Fragrance Discovery and AI Personalization

Technology is reshaping how consumers discover perfumes. AI-driven recommendation engines, virtual scent profiling, and augmented reality-based testing tools are improving online conversion rates. D2C perfume brands are leveraging digital platforms to bypass traditional retail, improving margins and customer engagement significantly.

Perfume Market Drivers

Rising Disposable Income and Luxury Consumption

Increasing global income levels, particularly in emerging economies, are boosting demand for premium fragrances. Consumers are treating perfumes as affordable luxury items, leading to frequent purchases and brand switching. Growth in affluent populations across Asia-Pacific and the Middle East is significantly supporting market expansion.

Expansion of Gender-Neutral and Inclusive Fragrances

The shift toward unisex fragrances is broadening market reach. Modern consumers prefer identity-neutral scent profiles, prompting brands to develop more versatile product lines. This trend is particularly strong among younger demographics, driving innovation in fragrance composition.

Influence of Celebrity and Luxury Branding

Celebrity-endorsed perfumes and luxury fashion house fragrances continue to dominate global sales. Strong brand storytelling, emotional marketing, and aspirational positioning are key factors driving consumer willingness to pay premium prices.

Perfume Market Restraints

High Price Sensitivity in Emerging Markets

Despite strong demand growth, affordability remains a barrier in developing economies. Premium and luxury fragrances remain out of reach for a large portion of consumers, limiting mass-market penetration.

Regulatory Restrictions on Ingredients

Strict global regulations on synthetic fragrance compounds and allergens increase compliance costs for manufacturers. Reformulation requirements in Europe and North America also limit product flexibility and innovation speed.

Perfume Market Opportunities

Personalized and Custom Fragrance Development

AI-driven customization and DNA-based fragrance profiling present major growth opportunities. Brands offering tailored scent experiences can achieve significantly higher margins and stronger customer retention.

Sustainable and Ethical Fragrance Production

Eco-friendly perfumes using plant-based ingredients and sustainable sourcing are gaining traction. Companies investing in circular packaging and carbon-neutral production processes are likely to benefit from long-term brand equity growth.

Expansion of D2C and E-commerce Channels

Online perfume sales are growing rapidly due to improved digital sampling technologies and influencer-driven marketing. Direct-to-consumer models help reduce distribution costs and increase profitability for brands.

Product Type Insights

Eau de Parfum (EDP) remains the dominant product category in the global perfume market, accounting for approximately 42% of total market revenue in 2025. The segment’s leadership is primarily driven by its higher fragrance oil concentration, long-lasting performance, and strong premium positioning among luxury consumers. Consumers increasingly prefer EDP products due to their superior longevity and stronger scent projection, particularly in premium markets across Europe, North America, and the Middle East. Luxury fashion houses and niche fragrance brands continue to prioritize Eau de Parfum launches because of their higher profit margins and stronger brand perception. Additionally, rising consumer willingness to invest in premium personal grooming products is supporting segment expansion globally. Eau de Toilette (EDT) represents the second-largest category, driven by affordability, lighter scent intensity, and suitability for everyday use. The segment remains particularly popular among younger consumers and mass-market buyers in emerging economies, where price sensitivity is relatively higher. Increasing urbanization and growing office-going populations are supporting demand for lighter fragrances suitable for daily wear. Seasonal fragrance consumption patterns also favor EDT products in warmer climates due to their lighter formulations.

Perfume oils are witnessing significant growth, especially across the Middle East, India, and parts of Southeast Asia, where alcohol-free and concentrated fragrance formats align with cultural and religious preferences. Oud-based oils and attars continue to experience strong demand due to their traditional significance and long-lasting aromatic profiles. In addition, natural and essential-oil-based fragrances are gaining traction globally as consumers increasingly prefer clean-label and skin-friendly formulations. Luxury and premium fragrances continue to dominate total revenue contribution due to higher average selling prices and strong aspirational demand. However, mass-market perfumes remain important for driving overall volume growth, particularly in Asia-Pacific and Latin America where expanding middle-class populations are entering the fragrance category for the first time.

Application Insights

Personal use remains the largest application segment within the global perfume market, accounting for the majority of fragrance consumption worldwide. Growth in this segment is primarily driven by rising consumer focus on grooming, self-expression, lifestyle enhancement, and daily wellness routines. Fragrances are increasingly viewed not only as beauty products but also as emotional and identity-driven purchases. Millennials and Gen Z consumers, in particular, are driving frequent product experimentation and multi-fragrance ownership trends, significantly increasing repeat purchases and overall consumption frequency. Luxury gifting represents another major application area, especially during festive seasons, weddings, anniversaries, and corporate celebrations. Premium perfume gift sets continue to perform strongly in regions such as the Middle East, Europe, China, and India, where luxury gifting culture is deeply embedded in consumer behavior. Limited-edition collections and personalized packaging are further enhancing the attractiveness of perfumes as gifting products.

The hospitality and tourism industry is emerging as a high-growth application segment, with luxury hotels, resorts, spas, and airlines increasingly adopting signature fragrances to create differentiated customer experiences and strengthen brand identity. Scent branding is becoming a strategic tool within premium hospitality environments, helping improve customer retention and emotional engagement. Corporate gifting and branding applications are also expanding rapidly, particularly across Asia-Pacific and the Middle East, where premium fragrance products are commonly used for client engagement, executive gifting, and festive corporate campaigns. In addition, the integration of fragrance into wellness, aromatherapy, and lifestyle products is creating new commercial applications for perfume manufacturers globally.

Distribution Channel Insights

Offline retail channels continue to dominate the global perfume market, accounting for the largest share of fragrance sales in 2025. Luxury boutiques, department stores, airport duty-free outlets, and specialty beauty retailers remain critical distribution points because perfume purchasing is highly experiential in nature. Consumers often prefer in-store fragrance testing before purchasing, especially for premium and luxury products. High-end retail environments also help brands strengthen customer engagement, premium positioning, and personalized consultation services. Department stores and travel retail channels remain particularly important in Europe, North America, and the Middle East, where international tourism and luxury shopping continue to support premium fragrance sales. Duty-free retail at international airports has become a significant revenue contributor for luxury perfume brands due to strong demand from international travelers seeking exclusive products and tax advantages.

However, online distribution channels are witnessing the fastest growth globally and currently account for nearly one-third of total perfume sales. Rapid digitalization, increased smartphone penetration, and the growing influence of social media marketing are accelerating online fragrance purchases. E-commerce platforms are increasingly utilizing AI-driven recommendation engines, virtual scent discovery tools, customer reviews, and influencer collaborations to improve online conversion rates. Direct-to-consumer (D2C) perfume brands are reshaping the competitive landscape by bypassing traditional retail intermediaries and improving profit margins. Subscription-based fragrance discovery services, sample-box models, and personalized fragrance platforms are further driving digital adoption. Younger consumers, particularly in Asia-Pacific and North America, are increasingly comfortable purchasing fragrances online due to convenience, discounts, and broader product availability.

| By Product Type | By Application | By Distribution Channel | By Gender | By Price Range |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

Europe

Europe remains the largest regional market for perfumes, accounting for approximately 34% of global market share in 2025. The region’s dominance is led by France, Germany, Italy, Spain, and the United Kingdom. France continues to serve as the global fragrance manufacturing and luxury perfume innovation hub due to its historical expertise, strong luxury fashion ecosystem, and advanced fragrance ingredient supply chain. Paris-based luxury houses and premium niche fragrance brands continue to drive significant export revenues globally.

Regional growth is primarily supported by strong consumer preference for luxury and artisanal fragrances, high disposable income levels, and increasing demand for sustainable and clean-label perfumes. European consumers are highly conscious of ingredient transparency, cruelty-free production, and environmentally friendly packaging, encouraging manufacturers to invest heavily in sustainable fragrance innovation. In addition, the expansion of premium travel retail, tourism recovery, and strong gifting culture across Western Europe continue to support market growth. Germany and the UK are also witnessing strong online fragrance sales growth due to increasing digital adoption and omnichannel retail strategies.

North America

North America accounts for approximately 28% of the global perfume market share, with the United States representing the largest revenue contributor in the region. The market is characterized by strong luxury retail infrastructure, celebrity fragrance influence, and high consumer spending on premium beauty and personal care products. Growth in North America is being driven by rising demand for niche fragrances, gender-neutral scents, and personalized fragrance experiences. Consumers are increasingly seeking exclusive and limited-edition perfumes that reflect individuality and lifestyle preferences. The region is also witnessing rapid growth in direct-to-consumer fragrance brands and subscription-based fragrance services. Social media platforms, influencer marketing, and celebrity endorsements continue to strongly shape purchasing behavior among younger consumers.

The United States remains the largest fragrance consumption market globally due to high per-capita spending and strong penetration of luxury beauty products. Canada is also experiencing steady growth, supported by increasing demand for premium clean-label and wellness-oriented fragrances.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, projected to expand at the highest CAGR through 2031. China, India, Japan, South Korea, and Southeast Asian countries are driving substantial demand growth due to rapid urbanization, rising disposable incomes, expanding middle-class populations, and increasing exposure to global luxury brands. China remains the largest growth engine in the region, supported by increasing premiumization trends and the rapid expansion of online luxury retail. Younger consumers in China are increasingly adopting fragrances as lifestyle products, while social commerce and livestream-based beauty marketing are significantly boosting product awareness. India is witnessing strong growth in affordable luxury perfumes and attars, driven by rising urban consumption and evolving grooming preferences among younger demographics.

South Korea and Japan continue to lead fragrance innovation and premium beauty consumption trends, while Southeast Asian markets are benefiting from expanding retail infrastructure and tourism growth. E-commerce penetration, influencer-led marketing, and increasing Western lifestyle adoption are key regional growth drivers.

Middle East & Africa

The Middle East & Africa region demonstrates one of the world’s highest per-capita fragrance consumption levels, particularly in the UAE, Saudi Arabia, and Qatar. Perfume usage is deeply embedded in cultural and religious practices, making fragrances an essential component of daily personal care and luxury consumption. Regional demand is strongly driven by oud-based perfumes, attars, concentrated perfume oils, and ultra-premium luxury fragrances. Consumers in the Gulf countries demonstrate strong preference for long-lasting and high-intensity scents, supporting demand for niche and artisanal fragrance brands. The expansion of luxury retail malls, rising tourism activity, and strong purchasing power among affluent consumers continue to support regional market growth.

In Africa, South Africa is emerging as a key growth market due to expanding middle-class populations, increasing urbanization, and rising adoption of international beauty brands. International luxury perfume manufacturers are increasingly expanding retail presence across the Gulf Cooperation Council (GCC) region to capitalize on strong premium fragrance demand.

Latin America

Latin America is experiencing steady growth in perfume consumption, led primarily by Brazil and Mexico. Brazil remains one of the largest fragrance consumption markets globally in terms of volume, supported by strong cultural affinity toward personal grooming and beauty products. Regional growth is driven by increasing penetration of affordable luxury fragrances, expansion of organized retail, and growing consumer aspiration for international beauty brands. Mass-market perfumes dominate volume sales, while premium fragrances are gaining traction among affluent urban consumers. The region also benefits from strong direct-selling networks and social-commerce-driven beauty retail models.

Mexico is witnessing increasing demand for imported premium fragrances due to rising disposable incomes and expanding e-commerce adoption. Additionally, celebrity fragrance brands and influencer-driven beauty marketing are playing a growing role in shaping purchasing trends across Latin America.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Perfume Market

- LVMH

- The Estée Lauder Companies

- L'Oréal

- Coty Inc.

- Puig

- Chanel

- Hermès

- Gucci

- Dior

- Shiseido