Pencil Cases Market Size

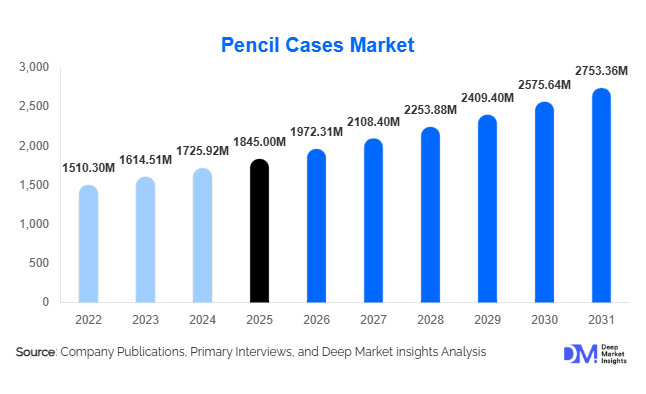

According to Deep Market Insights, the global pencil cases market size was valued at USD 1,845 million in 2025 and is projected to grow from USD 1,972.31 million in 2026 to reach USD 2,753.36 million by 2031, expanding at a CAGR of 6.9% during the forecast period (2026–2031). The pencil cases market growth is primarily driven by rising global student enrollment, increasing demand for organized stationery products, and growing consumer preference for aesthetically designed and multifunctional storage accessories. While digital learning adoption continues globally, hybrid education models and recurring back-to-school purchasing cycles sustain stable demand across both developed and emerging economies.

Key Market Insights

- Soft fabric pencil cases dominate global demand, supported by affordability, flexibility, and customization potential.

- Premium and designer stationery products are expanding rapidly, driven by lifestyle branding and personalization trends among younger consumers.

- Asia-Pacific leads global consumption, supported by large student populations and expanding education infrastructure.

- Online retail channels are the fastest-growing distribution segment, enabling niche brands to scale globally.

- Sustainable and recycled materials adoption is accelerating, particularly across Europe and North America.

- Multi-functional organizer designs are transforming pencil cases into lifestyle accessories used beyond classrooms.

What are the latest trends in the pencil cases market?

Shift Toward Sustainable and Eco-Friendly Materials

Environmental awareness is significantly influencing purchasing behavior within the stationery industry. Manufacturers are increasingly introducing pencil cases made from recycled polyester, organic cotton, and biodegradable materials to align with sustainability goals. Educational institutions and corporate buyers are also integrating environmentally responsible procurement policies, encouraging brands to adopt eco-certifications and reduced plastic packaging. Sustainable products often command premium pricing, improving margins while strengthening brand differentiation. Many companies are redesigning supply chains to incorporate recycled raw materials and lower carbon manufacturing processes, positioning sustainability as a long-term competitive advantage.

Multi-Functional and Lifestyle-Oriented Designs

Pencil cases are evolving from basic storage accessories into multifunctional organizers. New product formats include expandable compartments, stand-up designs, and integrated holders for digital accessories such as cables and styluses. Consumers increasingly view stationery as an extension of personal identity, leading to strong demand for themed, designer, and licensed merchandise. Social media influence and aesthetic-driven purchasing trends are encouraging brands to launch limited-edition collections and customizable products. This transition toward lifestyle positioning is increasing average selling prices and expanding usage among professionals and creative users.

What are the key drivers in the pencil cases market?

Growing Global Student Population

Rising enrollment across primary and secondary education systems remains the strongest driver for the pencil cases market. Governments worldwide continue investing in education accessibility, particularly across Asia-Pacific, Africa, and Latin America. Annual replacement cycles for school supplies ensure recurring demand regardless of broader economic conditions. Institutional procurement programs further reinforce stable volume consumption.

Expansion of E-Commerce and Organized Retail

The rapid growth of online marketplaces has significantly expanded product visibility and accessibility. Consumers can now compare designs, pricing, and product features globally, encouraging experimentation and premium purchases. E-commerce platforms allow smaller brands to compete internationally without extensive physical retail networks, accelerating product innovation and diversity within the market.

What are the restraints for the global market?

Digitalization Reducing Traditional Stationery Usage

The increasing adoption of tablets and laptops in developed education systems has slightly reduced reliance on traditional writing instruments, indirectly impacting stationery consumption. Although demand remains stable due to hybrid learning models, long-term digital adoption may moderate growth rates in mature markets.

Raw Material Price Volatility

Fluctuations in polyester fibers, plastics, and packaging materials create cost pressures for manufacturers. Price-sensitive markets limit the ability of producers to fully transfer increased costs to consumers, leading to margin compression and pricing competition, particularly within economy product segments.

What are the key opportunities in the pencil cases industry?

Premiumization and Personalization

Consumers increasingly seek personalized stationery reflecting individual preferences and lifestyle choices. Premium pencil cases featuring ergonomic designs, branded collaborations, and aesthetic customization are witnessing faster growth than standard products. Companies investing in personalization technologies and design collaborations can achieve higher margins while strengthening customer loyalty.

Emerging Market Education Expansion

Rapidly growing education sectors in countries such as India, Indonesia, Vietnam, and Nigeria present strong volume expansion opportunities. Government-funded school programs and literacy initiatives create large-scale procurement demand. Manufacturers entering these markets through institutional partnerships and localized production strategies can achieve significant growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1845 Million |

| Market Size in 2026 | USD 1972.31 Million |

| Market Size in 2031 | USD 2753.36 Million |

| CAGR | 6.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Soft pencil cases represent the leading product category, accounting for approximately 46% of the global market in 2025. Their dominance is primarily driven by their lightweight construction, cost efficiency, and flexibility, which make them suitable for a wide range of student age groups and everyday usage scenarios. Increasing preference for portable and space-efficient school accessories has further strengthened adoption, particularly in urban education environments where compact storage solutions are preferred. Manufacturers are also introducing reinforced fabrics, water-resistant materials, and ergonomic zipper designs, improving durability while maintaining affordability, thereby reinforcing the segment’s leadership position.

Hard pencil cases maintain steady demand, particularly among younger students and parents seeking enhanced protection for stationery items. The segment benefits from growing awareness around product longevity and organized storage, especially in primary education settings. Meanwhile, expandable organizer cases are gaining traction among college students, professionals, and creative users who require multifunctional storage capable of accommodating digital accessories alongside traditional stationery. Designer and specialty pencil cases are emerging as a premium niche segment driven by brand collaborations, licensed characters, and lifestyle-oriented product positioning. The broader industry trend toward multifunctionality continues to shape innovation, encouraging manufacturers to integrate modular compartments, hybrid organizers, and aesthetic customization features that appeal to both functional and fashion-conscious consumers.

Application (End-Use) Insights

K–12 students remain the largest end-use segment, contributing nearly 54% of global demand due to recurring academic purchasing cycles and consistent annual replacement requirements. Growth in this segment is supported by expanding global school enrollment, government education initiatives, and increasing parental spending on organized learning tools that enhance student productivity. The predictable nature of back-to-school purchasing patterns provides manufacturers with stable revenue visibility, making this segment the primary demand driver across both developed and emerging economies.

College students represent a rapidly expanding segment as aesthetic appeal, personalization, and multifunctional organizers gain importance among younger consumers. Rising campus culture trends and social media influence are encouraging purchases that combine utility with personal expression. Professional and office users maintain stable demand, particularly across Asian markets where handwritten documentation, examination preparation, and hybrid work practices sustain stationery usage. Artists and designers are emerging as a fast-growing niche segment requiring specialized storage solutions capable of holding brushes, markers, and technical tools. Institutional buyers such as schools, educational NGOs, and training centers further contribute to bulk procurement demand, ensuring consistent baseline sales volumes and supporting large-scale distribution contracts for manufacturers.

Distribution Channel Insights

Offline retail channels continue to dominate distribution, accounting for approximately 57% of global sales, largely driven by seasonal back-to-school purchasing through stationery stores, supermarkets, hypermarkets, and bookstores. Physical retail remains highly relevant due to consumer preference for tactile product evaluation, particularly among parents purchasing school supplies for children. Promotional bundling, in-store discounts, and localized merchandising strategies further strengthen offline sales performance during peak academic seasons.

However, online retail represents the fastest-growing channel, supported by rapid expansion of e-commerce ecosystems, improved logistics infrastructure, and increasing smartphone penetration worldwide. Influencer-driven marketing, product reviews, and digital brand storytelling are significantly shaping purchasing decisions, especially among younger consumers. Direct-to-consumer brand websites are gaining traction as manufacturers invest in digital engagement strategies, enabling greater control over branding, pricing, and customer relationships. Additionally, subscription-based school supply kits and bundled stationery offerings are emerging as innovative distribution models, improving convenience for parents while generating recurring revenue opportunities for brands.

Price Range Insights

Mid-range pencil cases priced between USD 5 and USD 15 account for the largest share of the market at roughly 48%, supported by their ability to balance affordability with enhanced design quality and durability. Consumers increasingly seek products that offer value-added features such as multiple compartments, premium fabrics, and modern aesthetics without significant price escalation. This positioning allows mid-range products to capture both price-sensitive buyers and consumers seeking moderate product upgrades.

Economy products continue to play a critical role in emerging economies where price sensitivity remains high and bulk purchasing dominates educational supply chains. These products benefit from large population bases and government-supported education expansion programs. In contrast, premium products priced above USD 15 represent the fastest-growing price segment, driven by branding, sustainability initiatives, licensed designs, and lifestyle positioning. Premiumization trends are particularly visible in developed markets where consumers increasingly prioritize eco-friendly materials, design innovation, and long-lasting product quality, contributing to rising average selling prices across the industry.

Explore more data points, trends and opportunities Download Free Sample Report

Pencil Cases Market Segmentations

By Product Type

- Soft Pencil Cases

- Hard Pencil Cases

- Multi-Compartment Organizer Cases

- Stand-Up / Expandable Pencil Cases

- Specialty & Designer Pencil Cases

By Material Type

- Polyester & Synthetic Fabrics

- Cotton & Canvas

- Plastic

- Metal

- Leather & Faux Leather

- Sustainable / Recycled Materials

By Distribution Channel

- Offline Retail

- E-commerce Marketplaces

- Brand Websites

- Educational Supply Platforms

By End User

- K–12 Students

- College & University Students

- Professionals & Office Users

- Artists & Designers

- Institutional Buyers

Regional Insights

Asia-Pacific

Asia-Pacific leads the global pencil cases market with approximately 39% market share in 2025, supported by a combination of large student populations, strong manufacturing ecosystems, and expanding consumer spending. China remains the largest manufacturing and consumption hub due to integrated supply chains, cost-efficient production capabilities, and strong export networks. India is among the fastest-growing markets, driven by rising school enrollment rates, expanding middle-class income levels, and increasing awareness of organized educational accessories. Japan and South Korea contribute significantly to premium market growth through strong design culture, brand loyalty, and consumer willingness to pay for aesthetically refined stationery products. Regional growth is further accelerated by rapid urbanization, digital retail expansion, and government investments in education infrastructure, which collectively sustain long-term demand.

North America

North America accounts for nearly 24% of global demand, led primarily by the United States, where structured back-to-school retail cycles strongly influence annual sales performance. Growth in the region is driven by increasing consumer preference for branded, eco-friendly, and premium stationery products aligned with sustainability awareness. Retail innovation, including omnichannel shopping experiences and private-label product expansion, continues to strengthen market competitiveness. Canada contributes stable institutional procurement demand supported by well-funded educational systems and standardized supply purchasing practices. Rising adoption of reusable and environmentally responsible products further supports premium segment expansion across the region.

Europe

Europe holds approximately 22% market share, with Germany, the United Kingdom, and France leading regional consumption. Market growth is strongly influenced by sustainability regulations and eco-conscious consumer behavior, accelerating adoption of recycled materials, biodegradable fabrics, and environmentally certified products. European consumers place high importance on durability, product quality, and environmental compliance, encouraging manufacturers to focus on sustainable innovation. Educational stability, strong retail infrastructure, and increasing demand for premium stationery aesthetics also contribute to steady regional expansion.

Latin America

Latin America is experiencing gradual but consistent growth, with Brazil and Mexico dominating regional demand supported by urbanization, improving literacy rates, and expanding school enrollment. Rising disposable income levels and growing access to organized retail formats are encouraging a shift from unbranded to branded stationery products. E-commerce adoption is also improving product accessibility across secondary cities, supporting broader market penetration. Government educational programs and demographic expansion among younger populations continue to create favorable long-term demand conditions.

Middle East & Africa

The Middle East & Africa region represents the fastest-growing market, expanding at an estimated CAGR above 8%. Growth is primarily driven by government investments in education infrastructure across countries such as the UAE, Saudi Arabia, and South Africa, alongside increasing private school development. Expanding youth populations across African nations are creating sustained demand for affordable educational supplies. Rising retail modernization, improving distribution networks, and increasing awareness of organized school accessories are further supporting market expansion. Additionally, economic diversification initiatives and growing urban consumer bases are enabling gradual adoption of branded and mid-range stationery products across the region.

Key Players in the Pencil Cases Market

- Newell Brands

- Kokuyo Co., Ltd.

- Pilot Corporation

- Faber-Castell AG

- Maped Group

- STAEDTLER SE

- Pentel Co., Ltd.

- Lihit Lab., Inc.

- Sun-Star Stationery Co., Ltd.

- Tombow Pencil Co., Ltd.

- ACCO Brands Corporation

- BIC Group

- KOKUYO Camlin Ltd.

- Derwent Cumberland Pencil Company

- Schneider Schreibgeräte GmbH