Pen Holder Stand Market Size

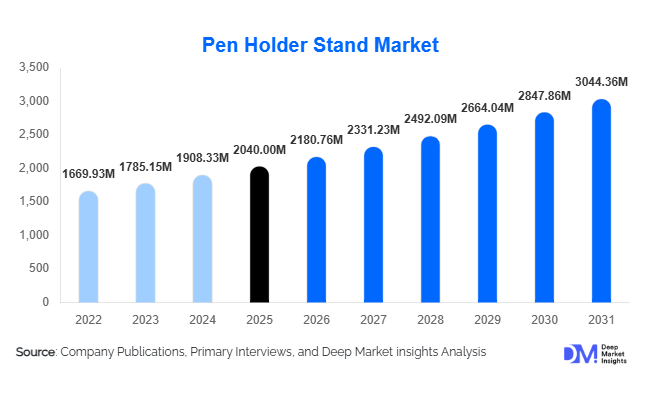

According to Deep Market Insights, the global pen holder stand market size was valued at USD 2,040 million in 2025 and is projected to grow from USD 2,180.76 million in 2026 to reach USD 3,044.36 million by 2031, expanding at a CAGR of 6.9% during the forecast period (2026–2031). Market growth is primarily driven by increasing workspace organization trends, expansion of hybrid work environments, rising educational infrastructure investments, and growing consumer preference for aesthetically designed desk accessories. The transition toward home offices and personalized workspaces has transformed pen holder stands from simple stationery storage products into multifunctional desk organization solutions.

Key Market Insights

- Hybrid and home-office culture is significantly boosting global demand for desk organization accessories, including multifunctional pen holder stands.

- Multi-compartment desk organizers dominate product demand, accounting for the largest share due to enhanced functionality and workspace efficiency.

- Asia-Pacific leads global production and consumption, supported by strong manufacturing ecosystems and expanding education sectors.

- Online retail channels account for over half of global sales, driven by e-commerce accessibility and product variety.

- Sustainable materials such as bamboo and recycled plastics are gaining adoption among corporate buyers and eco-conscious consumers.

- Smart desk accessories, including holders with wireless charging and lighting features, are emerging as premium growth categories.

What are the latest trends in the pen holder stand market?

Shift Toward Multifunctional Desk Organization

Consumers increasingly prefer multifunctional desk organizers that combine pen storage with compartments for stationery, mobile devices, and office accessories. Multi-compartment and modular pen holder stands are gaining widespread adoption across corporate offices and home workspaces. This trend is fueled by limited desk space in urban environments and rising productivity awareness among professionals. Manufacturers are introducing expandable and customizable organizers that adapt to changing workspace needs. Minimalist design aesthetics and ergonomic layouts are becoming essential product features, particularly among younger professionals and remote workers.

Sustainable and Eco-Friendly Material Adoption

Sustainability has emerged as a defining trend within the market. Corporate procurement departments and consumers increasingly favor products manufactured using bamboo, recycled plastics, and FSC-certified wood. Governments worldwide are implementing packaging waste and recyclability regulations, encouraging manufacturers to transition toward environmentally compliant materials. Eco-friendly pen holders often command premium pricing due to perceived environmental value and improved durability. Brands are also incorporating biodegradable packaging and circular manufacturing models, reinforcing sustainability as a long-term competitive differentiator.

What are the key drivers in the pen holder stand market?

Expansion of Hybrid Work and Home Office Setups

The global adoption of hybrid working models has significantly increased demand for personal workspace accessories. Employees investing in ergonomic and visually appealing desks are purchasing organization products that enhance productivity and aesthetics. Home-office penetration continues to rise across North America, Europe, and Asia-Pacific, creating sustained demand for pen holder stands across residential environments.

Growth of Educational Infrastructure Worldwide

Educational institutions remain one of the largest consumers of stationery accessories. Rapid expansion of schools and universities in emerging economies such as India, Indonesia, and Brazil is generating consistent procurement demand. Classroom desks, student housing, and administrative offices require low-cost yet durable organization products, supporting recurring market growth.

What are the restraints for the global market?

Digitalization and Reduced Writing Dependency

Increasing adoption of digital devices and paperless workflows in corporate environments reduces reliance on physical writing tools, indirectly moderating long-term demand growth. Although writing instruments remain essential in education and administration, digital transformation creates structural limitations in highly digitized economies.

Price Competition in Economy Segments

The presence of numerous low-cost manufacturers creates pricing pressure, particularly within plastic-based products. Limited differentiation in entry-level categories results in margin compression, forcing manufacturers to innovate through design, branding, and material upgrades.

What are the key opportunities in the pen holder stand industry?

Smart Desk Accessory Integration

Integration of technology into desk accessories presents a major opportunity. Pen holder stands equipped with wireless charging pads, LED lighting, digital clocks, and device holders are gaining popularity among professionals and gaming workstation users. These products deliver higher profit margins and enable manufacturers to enter premium consumer segments.

Eco-Friendly Product Innovation

Sustainability-driven procurement policies across corporations and institutions create opportunities for environmentally responsible product lines. Manufacturers investing in recycled materials and low-carbon production processes can secure long-term institutional contracts and differentiate their offerings globally.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2040 Million |

| Market Size in 2026 | USD 2180.76 Million |

| Market Size in 2031 | USD 3044.36 Million |

| CAGR | 6.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global pen holder market demonstrates strong diversification across product types, with multi-compartment desk organizer pen holders emerging as the leading category, accounting for approximately 32% of global revenue share in 2025. The dominance of this segment is primarily driven by increasing workspace optimization requirements across corporate offices and home environments. Modern consumers increasingly prefer multifunctional desk accessories capable of organizing multiple stationery items, mobile devices, sticky notes, and small electronic accessories within compact footprints. The rising adoption of hybrid work models has further strengthened demand, as users seek efficient desk organization solutions that enhance productivity while maintaining aesthetic appeal. Manufacturers are responding by integrating modular storage designs, ergonomic layouts, and space-saving configurations that cater to evolving workspace needs.

Rotating pen holders continue to gain adoption, particularly within corporate and institutional environments where accessibility and convenience are critical. Their ability to allow quick access to writing tools improves workflow efficiency, making them popular in shared workspaces and reception desks. Designer and premium pen holders are witnessing expanding demand within home-office setups and gifting applications, supported by growing consumer spending on workspace personalization and interior décor alignment. Meanwhile, smart pen holders represent the fastest-growing product category, driven by technological integration such as wireless charging, LED lighting, digital clocks, and device holders. Increasing consumer interest in smart desks and productivity-enhancing accessories is expected to accelerate innovation and adoption across this segment during the forecast period.

Material Insights

Plastic-based pen holder stands dominate the material segment, contributing nearly 41% of global revenue share, supported by their affordability, lightweight properties, and high manufacturing scalability. Plastic materials enable mass customization in terms of color, shape, and design, allowing manufacturers to cater to diverse consumer preferences across price-sensitive and emerging markets. Additionally, advancements in recyclable and biodegradable plastics are helping manufacturers address environmental concerns while maintaining cost advantages, thereby sustaining segment leadership.

Metal mesh pen holders maintain consistent demand within corporate offices and institutional settings due to their durability, professional aesthetics, and long product lifecycle. Their minimalist industrial appearance aligns with modern office design trends, supporting continued adoption. Wooden and bamboo pen holders are experiencing accelerated growth as sustainability awareness strengthens globally. Consumers, particularly in environmentally conscious markets, increasingly favor renewable and natural materials that complement eco-friendly workspace concepts. Premium materials such as leather and ceramic cater to luxury office décor and executive gifting applications, reinforcing the ongoing premiumization trend within the market. Rising disposable income levels and increased focus on workspace aesthetics are encouraging consumers to invest in visually distinctive and high-quality desk accessories.

Distribution Channel Insights

Online retail channels dominate global distribution, accounting for approximately 52% of total market sales, reflecting the rapid digital transformation of consumer purchasing behavior. E-commerce platforms provide extensive product variety, competitive pricing transparency, and convenient delivery options, enabling consumers to evaluate features, materials, and designs efficiently. The growth of global marketplaces and cross-border e-commerce has significantly expanded product accessibility, allowing small and niche manufacturers to reach international customers without extensive physical retail networks.

Offline distribution channels, including stationery stores, office supply retailers, and hypermarkets, continue to play an important role, particularly for institutional buyers and bulk procurement contracts. Businesses and educational institutions often prefer physical inspection of products prior to purchase, sustaining steady demand through traditional retail formats. Direct-to-consumer brand websites are emerging as a rapidly expanding channel, supported by increasing investments in digital marketing, customization tools, and brand storytelling strategies. These platforms allow manufacturers to improve margins, strengthen customer engagement, and offer personalized product options, further reshaping distribution dynamics within the industry.

End-Use Insights

Corporate offices represent the largest end-use segment, accounting for nearly 35% of total market demand. The segment’s leadership is driven by standardized workspace organization policies, increasing emphasis on employee productivity, and large-scale procurement agreements across enterprises. As organizations modernize office layouts and adopt ergonomic workplace solutions, demand for organized desk accessories continues to rise. Pen holders play an essential role in maintaining clutter-free environments, contributing to improved workflow efficiency and professional workspace presentation.

Educational institutions generate substantial volume demand due to continuous consumption across schools, colleges, and training centers worldwide. Rising student enrollment levels and expanding educational infrastructure, particularly in emerging economies, are supporting consistent product adoption. Household and home-office users represent the fastest-growing end-use segment, expanding at a growth rate exceeding 7% annually. Growth is fueled by remote working trends, freelancing expansion, and increasing investments in personalized home workspaces. Emerging applications are also expanding within gaming desks, creative studios, and co-working environments, where organized desk layouts contribute to both productivity enhancement and visual aesthetics, reinforcing long-term market growth opportunities.

Explore more data points, trends and opportunities Download Free Sample Report

Pen Holder Stand Market Segmentations

By Product Type

- Single-Compartment Pen Holder Stands

- Multi-Compartment Desk Organizer Pen Holders

- Rotating Pen Holder Stands

- Modular & Expandable Desk Organizers

- Decorative & Designer Pen Holders

- Smart/Functional Pen Holders

By Material Type

- Plastic

- Metal

- Wood

- Leather & Faux Leather

- Ceramic & Glass

- Eco-Friendly/Recycled Materials

By Distribution Channel

- Online Retail

- Stationery Stores

- Office Supply Chains

- Hypermarkets & Supermarkets

- Direct-to-Consumer Brand Websites

By End User

- Corporate Offices

- Educational Institutions

- Household & Home Offices

- Government & Public Institutions

- Hospitality & Commercial Spaces

Regional Insights

Asia-Pacific

Asia-Pacific holds the largest share of the global pen holder market, accounting for approximately 38% of total revenue in 2025. Regional dominance is supported by strong manufacturing ecosystems, cost-efficient production capabilities, and large consumer bases. China remains the global manufacturing hub, benefiting from integrated supply chains and export-oriented production, while India represents the fastest-growing consumption market driven by rapid urbanization, expansion of educational institutions, and increasing white-collar employment. Rising startup ecosystems and growing adoption of organized office infrastructure further stimulate product demand. Japan and South Korea contribute significant growth through demand for premium, minimalist, and design-oriented desk accessories, supported by high consumer preference for functional aesthetics and advanced workspace organization solutions.Regional growth is additionally driven by increasing digital literacy, expansion of e-commerce platforms, rising disposable incomes, and government investments in education and commercial infrastructure. The rapid penetration of hybrid work environments across major Asian economies is further accelerating adoption of desk organization accessories.

North America

North America accounts for nearly 27% of global demand, led primarily by the United States. Market growth in the region is strongly influenced by widespread adoption of home-office setups and continued investments in ergonomic workspace solutions. The shift toward remote and hybrid work has encouraged consumers to upgrade desk environments with multifunctional and aesthetically appealing accessories. High consumer purchasing power enables greater adoption of premium and smart pen holders, contributing to higher average selling prices.Regional growth drivers include strong e-commerce penetration, high awareness of productivity-enhancing accessories, and increasing corporate spending on employee workspace optimization. Sustainability trends are also influencing purchasing behavior, encouraging demand for recyclable and eco-friendly materials. Additionally, the presence of established office supply brands and advanced retail infrastructure supports consistent market expansion.

Europe

Europe captures approximately 22% market share, with Germany, the United Kingdom, and France representing key demand centers. The region’s growth is strongly influenced by stringent sustainability regulations and consumer preference for environmentally responsible products. Adoption of wooden, bamboo, and recycled-material pen holders is accelerating as organizations align procurement strategies with environmental standards and circular economy initiatives.European consumers place significant emphasis on design quality and minimalist aesthetics, supporting demand for premium and designer desk accessories. Growth is further supported by expanding remote work adoption, rising home-office investments, and increasing awareness of workspace organization as part of employee well-being initiatives. Innovation in eco-friendly materials and sustainable packaging continues to shape regional product development strategies.

Latin America

Latin America demonstrates stable market expansion, led by Brazil and Mexico, where growing small and medium-sized enterprises (SMEs) and expanding educational institutions are strengthening product demand. Increasing urban workforce participation and gradual modernization of office environments are contributing to steady adoption of desk organization products. Affordable plastic and multifunctional pen holders remain particularly popular due to price sensitivity across several regional markets.Regional growth is further supported by improving retail infrastructure, expanding online marketplaces, and rising investments in education and administrative sectors. Although economic fluctuations may influence short-term demand patterns, long-term growth remains supported by demographic expansion and increasing professional workforce development.

Middle East & Africa

The Middle East & Africa region is witnessing gradual yet consistent growth, supported by commercial infrastructure development and government-led diversification initiatives. Countries such as the United Arab Emirates and Saudi Arabia are experiencing rising demand driven by expansion of corporate offices, smart city projects, and public sector modernization programs. Increasing investments in business hubs and co-working spaces are contributing to growing adoption of organized desk accessories.Across Africa, improving educational access and institutional development are supporting rising consumption volumes, particularly in schools and administrative offices. Growth is also influenced by expanding retail distribution networks and increasing availability of affordable imported products. As urbanization accelerates and professional employment increases, demand for functional and cost-effective workspace organization solutions is expected to strengthen across the region.

Key Players in the Pen Holder Stand Market

- Newell Brands

- Kokuyo Co., Ltd.

- ACCO Brands Corporation

- Pilot Corporation

- Pentel Co., Ltd.

- Maped Group

- BIC Group

- Faber-Castell AG

- Deli Group Co., Ltd.

- Fellowes Brands

- Durable Hunke & Jochheim GmbH

- Staedtler Mars GmbH

- Office Depot Inc.

- 3M Company

- KOKUYO Furniture Division