Patches Market Size

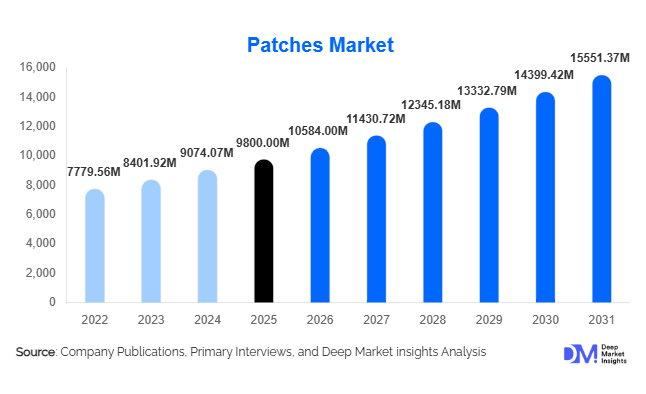

According to Deep Market Insights, the global patches market size was valued at USD 9,800 million in 2025 and is projected to grow from USD 10,584.00 million in 2026 to reach USD 15,551.37 million by 2031, expanding at a CAGR of 8.0% during the forecast period (2026–2031). The patches market growth is primarily driven by increasing demand for non-invasive drug delivery systems, rising prevalence of chronic diseases, and expanding applications across pharmaceuticals, cosmetics, and wearable healthcare technologies. The growing preference for self-administered therapies and advancements in transdermal and microneedle technologies are further accelerating adoption globally.

Key Market Insights

- Transdermal drug delivery patches dominate the market, accounting for nearly 48% of total demand due to their effectiveness in chronic disease management.

- Smart and wearable patches are emerging rapidly, integrating biosensors and digital health capabilities for real-time monitoring.

- North America leads the global market, driven by high healthcare expenditure and early adoption of advanced drug delivery systems.

- Asia-Pacific is the fastest-growing region, supported by expanding healthcare access and large patient populations.

- Retail pharmacies remain the primary distribution channel, contributing approximately 45% of total sales.

- Technological advancements, including microneedle patches and drug-in-adhesive systems, are enhancing product efficacy and expanding applications.

What are the latest trends in the patches market?

Rise of Smart and Connected Patches

The integration of digital health technologies into patch-based systems is transforming the market landscape. Smart patches equipped with biosensors can monitor physiological parameters such as glucose levels, heart rate, and temperature in real time. These devices enable remote patient monitoring and personalized treatment, aligning with the growing trend toward telemedicine and preventive healthcare. Companies are increasingly investing in IoT-enabled patches that connect with mobile applications, offering data analytics and actionable insights for both patients and healthcare providers. This trend is particularly gaining traction in diabetes management and cardiovascular monitoring, where continuous tracking is essential.

Expansion of Microneedle and Cosmetic Patches

Microneedle patches are gaining significant attention due to their ability to deliver drugs painlessly and efficiently through the skin. These patches are being explored for vaccine delivery, insulin administration, and dermatological treatments. Simultaneously, the cosmetic industry is driving demand for dermal patches used in anti-aging, acne treatment, and skin hydration. Consumers are increasingly adopting these products for their convenience and targeted application, making cosmetic patches one of the fastest-growing segments in the market.

What are the key drivers in the patches market?

Increasing Prevalence of Chronic Diseases

The rising incidence of chronic conditions such as cardiovascular diseases, diabetes, and neurological disorders is a major driver of the patches market. These conditions often require long-term medication, and patches offer a convenient and consistent drug delivery mechanism. Their ability to provide controlled release improves therapeutic outcomes and enhances patient compliance, making them a preferred choice among healthcare providers.

Growing Demand for Non-Invasive Drug Delivery

Patients are increasingly seeking painless and easy-to-use treatment options, driving demand for non-invasive drug delivery systems. Patches eliminate the need for injections and reduce gastrointestinal side effects associated with oral medications. This shift is particularly evident among aging populations and individuals managing chronic conditions at home, contributing to sustained market growth.

What are the restraints for the global market?

Limited Drug Permeability

One of the primary challenges in the patches market is the limitation of drug permeability through the skin. Not all drugs are suitable for transdermal delivery, particularly those with large molecular sizes. This restricts the range of therapeutics that can be delivered via patches, limiting market expansion.

High Cost of Advanced Patches

Advanced patches, especially smart and microneedle variants, involve complex manufacturing processes and stringent regulatory requirements. This results in higher costs compared to traditional drug delivery methods, which can hinder adoption in price-sensitive markets and developing regions.

What are the key opportunities in the patches industry?

Integration with Digital Health Ecosystems

The convergence of patches with digital health platforms presents significant opportunities for market growth. Smart patches that provide real-time health data can be integrated with telemedicine systems, enabling remote monitoring and personalized treatment plans. This is particularly relevant in managing chronic diseases and reducing hospital visits, creating new revenue streams for manufacturers and healthcare providers.

Emerging Market Expansion

Emerging economies in Asia-Pacific, Latin America, and Africa offer substantial growth opportunities due to rising healthcare investments and increasing awareness of advanced medical technologies. The demand for cost-effective and easy-to-use drug delivery systems is particularly high in these regions, making patches an attractive solution for expanding healthcare access.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 9800 Million |

| Market Size in 2026 | USD 10584 Million |

| Market Size in 2031 | USD 15551.37 Million |

| CAGR | 8.0% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Transdermal drug delivery patches represent the largest segment, accounting for approximately 48% of the global market in 2025. This segment’s leadership is primarily driven by its extensive clinical validation and widespread adoption across therapeutic areas such as pain management, smoking cessation, cardiovascular diseases, and hormone replacement therapy. The ability of transdermal patches to deliver controlled and sustained drug release while improving patient compliance remains a key growth driver. Additionally, increasing preference for non-invasive and self-administered treatment solutions continues to reinforce their dominance globally.

Topical and cosmetic patches are rapidly gaining traction, supported by rising consumer awareness around skincare, anti-aging, and wellness products. The convenience of targeted application and visible results has made these patches highly popular among younger and urban populations. Meanwhile, microneedle patches are emerging as a high-growth segment, driven by their ability to deliver biologics, vaccines, and insulin painlessly, overcoming traditional skin permeability barriers. The increasing focus on mass immunization and biologics delivery is expected to accelerate this segment further. Smart and connected patches are also gaining significant momentum, particularly in developed markets. These patches integrate biosensors and wireless connectivity to enable real-time health monitoring and data transmission. Growth in this segment is fueled by advancements in wearable technology, increasing adoption of remote patient monitoring, and the rising integration of digital health ecosystems.

Application Insights

Pain management remains the leading application segment, contributing approximately 30% of the global market in 2025. The segment’s dominance is driven by the high global prevalence of chronic pain conditions such as arthritis, back pain, and post-operative pain. Transdermal patches provide continuous drug delivery and reduce dependency on oral medications, making them a preferred solution for long-term pain management.

Smoking cessation and hormonal therapy applications also hold significant shares, supported by growing health awareness and lifestyle-related disorders. Nicotine patches are widely adopted as part of smoking cessation programs, particularly in developed markets with strong public health initiatives. Hormonal patches, including estrogen and testosterone therapies, are increasingly used for managing menopause and endocrine disorders. The diabetes management segment is witnessing rapid growth, driven by the increasing global diabetic population and the adoption of continuous glucose monitoring systems integrated with wearable patches. Additionally, cosmetic and dermatology applications are expanding at a strong pace, fueled by consumer demand for non-invasive skincare treatments, particularly in Asia-Pacific and North America. The growing overlap between healthcare and beauty industries is further accelerating innovation in this segment.

Distribution Channel Insights

Retail pharmacies dominate the distribution landscape, accounting for approximately 45% of total market sales in 2025. Their leadership is driven by widespread accessibility, strong consumer trust, and the availability of both prescription and over-the-counter patches. Retail pharmacies serve as the primary channel for chronic disease management products, including pain relief and nicotine patches.

Hospital pharmacies hold a significant share, particularly for prescription-based and specialized therapeutic patches used in clinical settings. This segment is supported by increasing hospital admissions and the growing use of patches in post-operative and chronic care treatments. Online pharmacies are emerging as the fastest-growing distribution channel, driven by increasing digital adoption, e-commerce penetration, and the convenience of home delivery. The COVID-19 pandemic accelerated this shift, and the trend continues as consumers prefer contactless purchasing options. Additionally, direct institutional sales to healthcare providers, research organizations, and pharmaceutical companies are contributing to market expansion, particularly for advanced and specialty patches.

End-Use Insights

Hospitals and clinics represent the largest end-use segment, accounting for approximately 40% of global demand in 2025. This dominance is driven by the extensive use of prescription-based patches in clinical treatments, including pain management, cardiovascular care, and hormonal therapies. The increasing burden of chronic diseases and hospital-based treatment protocols continues to support demand in this segment. Home healthcare is the fastest-growing end-use segment, expanding at a CAGR of over 9%. The shift toward outpatient care, aging populations, and rising preference for self-administered therapies are key drivers. Patches offer a convenient and safe alternative for patients managing long-term conditions at home, reducing the need for frequent hospital visits.

The pharmaceutical and biotechnology industry remains a major contributor, with a market size exceeding USD 6,000 million in 2025, as companies increasingly invest in advanced drug delivery systems. Meanwhile, the cosmetic and personal care industry is emerging as a significant end-use segment, driven by rising consumer demand for innovative skincare and wellness solutions. The convergence of healthcare and beauty is expected to create new growth avenues in this segment.

Explore more data points, trends and opportunities Download Free Sample Report

Patches Market Segmentations

By Product Type

- Transdermal Drug Delivery Patches

- Topical (Dermal) & Cosmetic Patches

- Microneedle Patches

- Smart / Connected Patches

- Specialty Patches

By Application

- Pain Management

- Smoking Cessation

- Hormonal Therapy

- Cardiovascular & Neurological Disorders

- Diabetes Management

- Cosmetic & Dermatology

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies / E-commerce

- Direct Institutional Sales

Regional Insights

North America

North America dominates the global patches market, accounting for approximately 38% of total market share in 2025, with the United States being the largest contributor. The region’s leadership is driven by high healthcare expenditure, advanced healthcare infrastructure, and early adoption of innovative drug delivery technologies. Strong presence of leading pharmaceutical and medical device companies further supports market growth. Additionally, the increasing prevalence of chronic diseases, high awareness of smoking cessation programs, and rapid adoption of smart wearable patches are key drivers. Favorable reimbursement policies and regulatory approvals for advanced therapies also contribute significantly to regional expansion.

Europe

Europe holds around 27% of the global market share, with Germany, the UK, and France as major contributors. The region benefits from a well-established healthcare system and stringent regulatory frameworks that ensure product quality and safety. Growth in Europe is driven by a rising geriatric population, an increasing incidence of chronic diseases, and strong government support for innovative drug delivery systems. Additionally, high adoption of nicotine patches due to anti-smoking regulations and growing demand for hormone replacement therapies are key regional drivers. The region is also witnessing increased investment in research and development of advanced patch technologies.

Asia-Pacific

Asia-Pacific accounts for approximately 24% of the global market and is the fastest-growing region, with a CAGR exceeding 9.5%. China, Japan, and India are the primary growth engines. The region’s rapid expansion is driven by large patient populations, rising healthcare expenditure, and increasing awareness of advanced treatment options. Government initiatives to improve healthcare access, coupled with growing middle-class income, are accelerating adoption. Japan leads in technological innovation, particularly in transdermal systems, while China and India are witnessing strong demand due to expanding pharmaceutical manufacturing and increasing prevalence of chronic diseases. The growth of the cosmetic industry in this region is also boosting demand for dermal patches.

Latin America

Latin America represents a smaller but steadily growing market, led by Brazil and Mexico. The region’s growth is supported by improving healthcare infrastructure, rising healthcare investments, and increasing awareness of modern drug delivery systems. Expanding access to healthcare services and government initiatives to address chronic diseases are key drivers. Additionally, the growing middle-class population and increasing adoption of over-the-counter healthcare products are contributing to demand. However, pricing sensitivity remains a challenge, influencing the adoption of advanced patch technologies.

Middle East & Africa

The Middle East & Africa region is gradually expanding, with countries such as the UAE and South Africa leading demand. Growth in this region is driven by increasing investments in healthcare infrastructure, rising prevalence of chronic diseases, and growing awareness of advanced medical technologies. Government initiatives to modernize healthcare systems and improve access to treatment are supporting market development. Additionally, the expansion of private healthcare providers and the increasing import of advanced medical products are contributing to market growth. While the market remains in a developing stage, rising urbanization and healthcare spending are expected to drive future demand.

Key Players in the Patches Market

- Johnson & Johnson

- Novartis AG

- Viatris Inc.

- Hisamitsu Pharmaceutical

- Teva Pharmaceutical Industries

- Bayer AG

- GlaxoSmithKline

- 3M Company

- UCB Pharma

- Purdue Pharma

- AbbVie Inc.

- Nitto Denko Corporation

- Luye Pharma Group

- Samyang Biopharmaceuticals

- LTS Lohmann Therapie-Systeme