Paper Cup Market Size

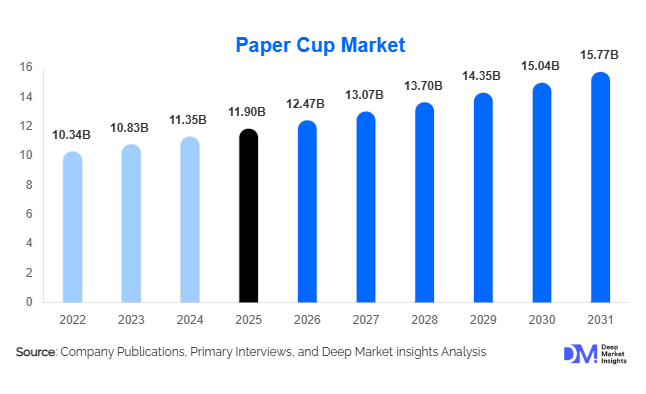

According to Deep Market Insights, the global paper cup market size was valued at USD 11.9 billion in 2025 and is projected to grow from USD 12.47 billion in 2026 to reach USD 15.77 billion by 2031, expanding at a CAGR of 4.8% during the forecast period (2026–2031). The paper cup market growth is primarily driven by the increasing global shift away from single-use plastics, rising takeaway beverage consumption, rapid expansion of quick-service restaurant chains, and growing adoption of sustainable foodservice packaging solutions.

Paper cups have become an essential component of modern foodservice infrastructure across cafés, coffee chains, convenience stores, institutional catering, and online food delivery platforms. Governments across North America, Europe, and the Asia-Pacific are implementing stricter environmental regulations on plastic packaging waste, encouraging businesses to adopt recyclable and compostable paper-based alternatives. Simultaneously, rising coffee culture, urbanization, and changing consumer lifestyles are accelerating demand for disposable beverage packaging globally.

Technological innovations in water-based barrier coatings, biodegradable cup linings, and recyclable paper materials are transforming manufacturing standards within the industry. Premium insulated paper cups with enhanced thermal resistance and customized branding are increasingly being adopted by multinational café chains and foodservice operators. Asia-Pacific is emerging as the fastest-growing regional market due to rising disposable incomes, rapid growth in organized foodservice, and increasing environmental awareness, while North America continues to dominate global consumption owing to strong coffee culture and mature takeaway infrastructure.

Key Market Insights

- Global regulations restricting single-use plastics are accelerating adoption of paper-based beverage packaging, particularly across foodservice and institutional sectors.

- Premium insulated paper cups are gaining strong demand globally, driven by rising coffee consumption and consumer preference for improved beverage handling experiences.

- North America dominates the paper cup market, supported by high per-capita coffee consumption and extensive quick-service restaurant penetration.

- Asia-Pacific remains the fastest-growing regional market, led by rapid urbanization, café culture expansion, and rising takeaway beverage demand in China and India.

- Food delivery and cloud kitchen platforms are significantly increasing paper cup consumption, particularly for hot beverage transportation applications.

- Technological advancements in sustainable coatings and recyclable barrier materials are reshaping product innovation and regulatory compliance strategies.

Paper Cup Market Trends

Sustainable Coating Technologies Transforming Product Innovation

Manufacturers are increasingly investing in sustainable coating technologies to reduce dependence on polyethylene-lined paper cups. Water-based coatings, bio-based barriers, and compostable lining materials are gaining traction as governments tighten packaging waste regulations. Large foodservice brands and café chains are prioritizing recyclable and plastic-free paper cups to improve sustainability credentials and meet environmental targets. This trend is encouraging manufacturers to develop next-generation cup structures that maintain moisture resistance and thermal insulation while improving recyclability. Several companies are also investing in FSC-certified fiber sourcing and low-carbon manufacturing processes to strengthen their environmental positioning.

Customization and Digital Printing Expanding Rapidly

Digital printing technologies are transforming the paper cup market by enabling low-volume, high-quality customized packaging production. Coffee chains, restaurants, event organizers, and beverage brands increasingly use paper cups as promotional and branding tools. Seasonal campaigns, regional branding, festival promotions, and personalized customer experiences are driving strong adoption of digitally printed paper cups. This trend is particularly prominent among premium cafés and entertainment venues seeking enhanced customer engagement. The ability to rapidly customize packaging while maintaining operational efficiency is creating significant value for foodservice operators and packaging manufacturers alike.

Paper Cup Market Drivers

Global Restrictions on Single-Use Plastics

Government regulations targeting single-use plastics are among the strongest drivers supporting paper cup market growth. Countries across Europe, North America, and Asia-Pacific are implementing bans and restrictions on disposable plastic packaging, encouraging foodservice operators to transition toward paper-based alternatives. Environmental sustainability targets and circular economy initiatives are accelerating investments in recyclable and compostable packaging solutions. Large multinational restaurant chains are also committing to sustainable procurement programs, creating long-term demand for eco-friendly paper cups.

Growth of Takeaway Beverage and Coffee Culture

The rapid expansion of global coffee culture and takeaway beverage consumption continues to fuel market demand. Urban consumers increasingly prefer portable beverage solutions due to convenience-focused lifestyles and rising mobility. Coffee chains, convenience stores, and quick-service restaurants are witnessing sustained growth in disposable beverage packaging consumption. Emerging economies such as India, China, Indonesia, and Vietnam are experiencing significant growth in café culture, further expanding paper cup demand. Premium hot beverage applications are particularly supporting growth in insulated and double-wall cup formats.

Paper Cup Market Restraints

Volatility in Raw Material Prices

The paper cup industry remains highly sensitive to fluctuations in pulp, paperboard, and energy prices. Rising wood pulp costs and transportation expenses directly impact manufacturing margins, especially for small and mid-sized producers operating in highly competitive markets. Volatile raw material pricing can reduce profitability and create pricing pressure across institutional supply contracts. Manufacturers are increasingly focusing on supply chain optimization and long-term sourcing agreements to reduce exposure to cost fluctuations.

Limited Recycling Infrastructure

Although paper cups are considered more sustainable than plastic alternatives, conventional PE-lined cups remain difficult to recycle in many regions. Developing economies often lack specialized recycling facilities capable of separating paper fibers from plastic linings. This infrastructure gap creates environmental criticism and regulatory pressure on manufacturers to adopt more expensive sustainable coating technologies. Additionally, increasing competition from reusable beverage systems and alternative compostable materials may restrict growth in certain developed markets.

Paper Cup Market Opportunities

Expansion of Sustainable and Compostable Paper Cups

The growing global emphasis on sustainable packaging presents major opportunities for manufacturers investing in compostable and recyclable paper cup technologies. Governments, multinational café chains, and institutional buyers are increasingly prioritizing environmentally compliant foodservice packaging solutions. Manufacturers capable of commercializing water-based coatings, plastic-free cup structures, and bio-based barrier technologies are expected to secure premium contracts and strengthen long-term market positioning. The transition toward circular packaging systems is also creating opportunities for recycling partnerships and closed-loop material recovery initiatives.

Emerging Market Growth and Foodservice Expansion

Rapid expansion of organized foodservice and café chains across emerging economies is creating significant opportunities for paper cup manufacturers. Countries such as India, Vietnam, Indonesia, Brazil, and Saudi Arabia are witnessing rising disposable incomes, urbanization, and growth in takeaway dining culture. International coffee chains and regional quick-service restaurant brands are aggressively expanding outlet networks, generating sustained demand for customized beverage packaging. Localized manufacturing, export-oriented production, and private-label supply agreements are expected to remain key growth strategies for both established companies and new market entrants.

Cup Type Insights

Hot paper cups dominate the global market, accounting for nearly 62% of total revenue in 2025, supported by rising coffee and tea consumption worldwide. Coffee chains, office vending systems, and convenience retailers remain major consumers of insulated hot beverage cups. Cold paper cups continue to witness strong growth across soft drink, juice, and frozen dessert applications, particularly in quick-service restaurants and entertainment venues. Demand for specialty beverage cups with enhanced insulation and premium finishes is also increasing as cafés focus on customer experience differentiation.

Wall Type Insights

Single-wall paper cups account for approximately 48% of global demand due to their cost efficiency and broad adoption across quick-service beverage applications. However, double-wall and ripple-wall paper cups are growing at faster rates due to rising demand for premium hot beverage packaging with improved heat insulation. Triple-wall insulated cups are increasingly used in premium café chains and institutional catering environments where superior thermal protection and customer comfort are prioritized.

Coating Type Insights

Polyethylene-coated paper cups continue to dominate the market with nearly 58% share due to established manufacturing infrastructure and lower production costs. However, water-based coated and PLA-coated paper cups are witnessing rapid adoption across Europe and North America as sustainability regulations become more stringent. Bio-based barrier coatings are emerging as a critical innovation segment, enabling manufacturers to improve recyclability while maintaining liquid resistance and structural integrity.

End-Use Industry Insights

Quick-service restaurants remain the largest end-use segment for paper cups, accounting for nearly 34% of global consumption in 2025. Large international chains require high-volume standardized beverage packaging supported by reliable supply contracts and branding consistency. Café chains and food delivery platforms are among the fastest-growing segments globally, driven by urban convenience lifestyles and rising online ordering penetration. Institutional applications including hospitals, airports, railways, and educational campuses are also expanding rapidly due to sustainability-focused procurement policies.

Distribution Channel Insights

Direct institutional contracts dominate paper cup distribution globally, accounting for nearly 44% of market share in 2025. Large foodservice operators increasingly prefer long-term agreements with packaging manufacturers to ensure supply consistency and customized branding support. Packaging distributors and wholesale suppliers remain important for regional cafés and independent restaurants. Meanwhile, e-commerce procurement platforms are witnessing rapid growth among small and medium-sized foodservice businesses due to improved accessibility, bulk ordering flexibility, and digital product customization capabilities.

| By Cup Type | By Wall Type | By Coating Type | By End User | By Distribution Channel |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America accounted for approximately 36% of the global paper cup market in 2025, making it the largest regional market by revenue. The United States alone represented nearly 29% of global demand due to strong coffee culture, widespread takeaway beverage consumption, and the extensive presence of multinational café and quick-service restaurant chains. Sustainability initiatives and plastic reduction policies are further accelerating demand for recyclable paper-based packaging solutions across the region.

Europe

Europe held nearly 27% of global market share in 2025, supported by stringent environmental regulations and strong consumer preference for sustainable packaging. Germany, the United Kingdom, and France are among the leading contributors within the region. European foodservice operators are rapidly adopting compostable and recyclable cup technologies to comply with circular economy policies and single-use plastic restrictions. Premium café culture and sustainability-conscious consumers continue to drive innovation in eco-friendly beverage packaging.

Asia-Pacific

Asia-Pacific is projected to be the fastest-growing regional market through 2031, with a CAGR expected to exceed 6%. China remains the largest regional consumer due to the rapid expansion of café chains, convenience stores, and food delivery platforms. India is emerging as one of the fastest-growing national markets globally owing to rising disposable incomes, urbanization, and strong growth in organized foodservice infrastructure. Japan and South Korea continue to support premium demand for insulated and customized beverage packaging.

Latin America

Latin America accounted for approximately 6% of global demand in 2025, with Brazil representing the region’s largest market. Growing coffee retail infrastructure, increasing urban takeaway beverage consumption, and expansion of quick-service restaurants are supporting regional growth. Mexico is also witnessing increasing demand due to rising convenience retail penetration and foodservice investments.

Middle East & Africa

The Middle East & Africa region held nearly 6% market share in 2025. GCC countries including the UAE and Saudi Arabia are experiencing rising demand due to café culture expansion, tourism growth, and premium hospitality development. South Africa remains the leading African market supported by organized retail and hospitality sector growth. Increasing environmental awareness and tourism-driven foodservice expansion are expected to further strengthen regional demand.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Paper Cup Market

- Huhtamaki Oyj

- Dart Container Corporation

- Pactiv Evergreen Inc.

- Graphic Packaging International

- WestRock Company

- Detmold Group

- International Paper Company

- Genpak LLC

- Duni Group

- Benders Paper Cups

- Go-Pak Group

- Seda International Packaging Group

- SCG Packaging

- Konie Cups International

- Lollicup USA Inc.